U.S. Highlights

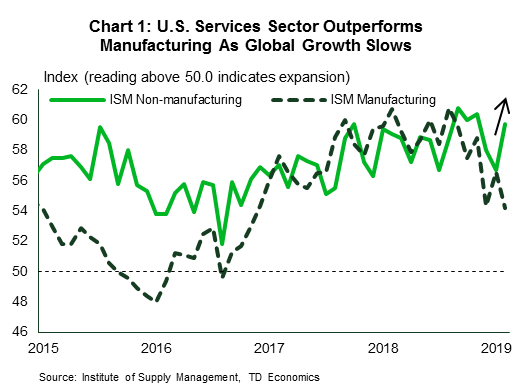

- This week started off on an upbeat note. An uptick in the ISM non-manufacturing index got the ball rolling, with the headline rising by 3.0 points to 59.7 in February.

- In a nice twist to the recent doom and gloom, housing data was also encouraging. Sales of new homes rose 3.6% in December, and housing starts surged by 18.6% in January.

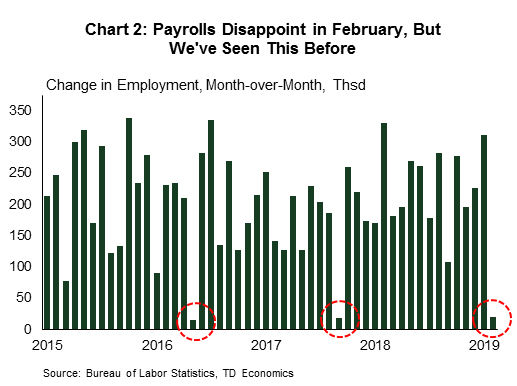

- The positive economic news faced a setback on Friday as the payroll report showed job growth slowing to just 20k in February. The soft payroll print is unlikely to stay, but works to reinforce the Federal Reserve’s current “patient” approach.

Canadian Highlights

- The Bank of Canada left the overnight rate at 1.75% this week. Its statement made clear that it is not looking to increase rates anytime soon, noting in its follow up communication that it “need[s] time to better understand what’s happening”.

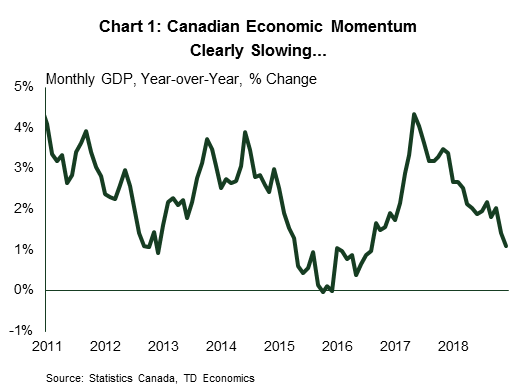

- Housing data confirm the Canadian economic malaise continued into the first quarter with home sales down in Toronto and Vancouver and housing starts plunging across the country in February.

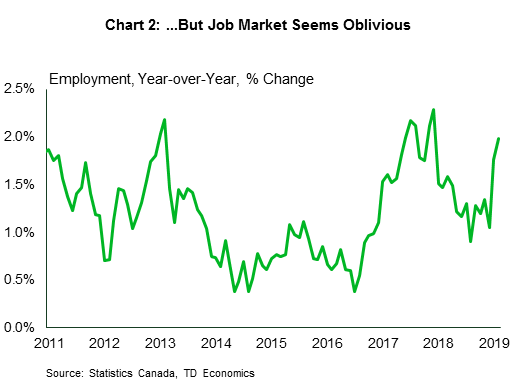

- Despite the near-universal bad economic news, the Canadian job market continued to add jobs at an astonishing rate in February. Some 55.9k jobs were added, while the unemployment rate remained near a cyclical low of 5.8% as more people entered the labour market.

U.S. – Positive Economic Data Muted By Weak Payroll Print

In a welcome change from the recent doom and gloom, this week started off on an upbeat note. An uptick in the ISM non-manufacturing index got the ball rolling. Diverging from its manufacturing counterpart, the headline rose 3.0 points to 59.7 in February, reversing two consecutive declines in the prior months. An improved performance in the services sector is echoed in consumer confidence that rebounded with the conclusion of the partial government shutdown and a turnaround in equity markets. It also reaffirms that domestic demand remains solid, corroborated by gains in all 18 industries in February.

Housing data was also encouraging this week. Sales of new homes rose 3.6% in December, edging higher for the second month in a row. Ditto for housing starts. After ending 2018 on a sour note, homebuilding started the year on better footing with starts surging by 18.6% in January. The gain in single-family construction was even more impressive, with starts up by 25% – the highest monthly gain since 1979. As we discuss in our recent report, the housing market has room to grow and demand should rebound alongside rising affordability. With low vacancy rates, housing construction should continue to make gains over the next year.

The positive economic news faced a setback on Friday as the payroll report showed job growth slowing to just 20k new jobs in February. The headline was a big miss on expectations, but notably came after two months of strong consensus-beating gains. There was also plenty of encouraging news in other parts of the report. The unemployment rate edged lower, the labor force participation rate maintained January’s gain and hourly earnings accelerated, rising to 3.4% year-on-year – the fastest pace in almost ten years.

There is good reason to look past the dour headline, which was probably influenced by temporary factors and poor weather. We expect job growth to slow in the months ahead, but it will be on the back of a labor market that for all intents and purposes has achieved full employment rather than any pronounced deterioration in domestic demand.

Still, the soft payroll print will reinforce the Federal Reserve’s current “patient” approach. On that front, the Federal Reserve has been joined by other global central banks. This week, the ECB unveiled a package of cheap funding for the Eurozone’s banks and said it would keep rates on hold until 2020 on the back of softening economic momentum and rising uncertainty related to Brexit and trade. The Bank of Canada’s statement this week was similarly dovish – noting the increased difficulty in reading the economic tea leaves given the increase in global crosscurrents. The dovish turn in other global central banks means the U.S. dollar is likely to remain relatively strong, giving the Fed even more reason to remain on the sidelines until at least the second half of this year.

Canada – It’s a Hard Knock Life for Central Bankers

Much like its counterparts around the world, the Bank of Canada this week recognized the deterioration in the economic outlook and the haze of uncertainty around the future course of policy. On Wednesday, it left the overnight rate unchanged at 1.75%. Its statement made clear that it is not looking to increase its policy rate any time soon.

Outside the Labour Force Survey (LFS), the economic data has been unambiguously bad. Even more concerning for the central bank is that the weakest data is in segments of the economy most sensitive to interest rates – namely business investment, housing, and consumer durable goods spending. Investment in both non-residential and residential sectors fell off a cliff in the second half of 2018, and durable goods spending has fallen for three straight quarters.

The data for early 2019 suggest that the pain continued in the first quarter, especially in the housing market. Home sales fell in Toronto and Vancouver in February according to local real estate board data. Meanwhile, housing starts plummeted across the country in the same month.

Given the available data, the Canadian economy appears more likely to have shrunk in the first quarter of the year than shown any meaningful growth. This is not the narrative the Bank of Canada was hoping for. A slowdown in housing and related consumer spending has long been anticipated, but it has come faster and more furiously than expected. Also worrying is that the pullback in business investment is broad-based, and not just an energy story.

In a speech explaining the Bank of Canada’s thinking, Deputy Governor Lynn Patterson attributed at least some of the pullback in investment to uncertainty around the free trade deal that has yet to be ratified, but is not overly confident in this view. As its accompanying communication noted, the Bank “need[s] time to better understand what’s happening”.

The apparent resilience in the labour market muddies the outlook further. The Canadian job market churned out 55.9k jobs in February. The outsized gain is more than your regular volatility. The six month trend is an equally impressive 48.3k. On a year-on-year basis, employment is up 2.0%, the strongest growth in over a year. Fascinatingly, despite the gain in jobs, the total number of labour hours worked in the country continues to fall, implying that the jobs created are with fewer hours than those existing or replaced (data on job flows by hours worked is unfortunately not available).

While notable, the labour market strength doesn’t provide enough assurance because it is typically a lagging indicator. The evidence suggested by a broad range of indicators is that the current stance of policy is more than adequate to stem inflationary pressures. The Bank of Canada’s statement still noted the potential interest rate increases, but this will require the data to tell a better story than the one we’ve been reading over the past several months.

U.S.: Upcoming Key Economic Releases

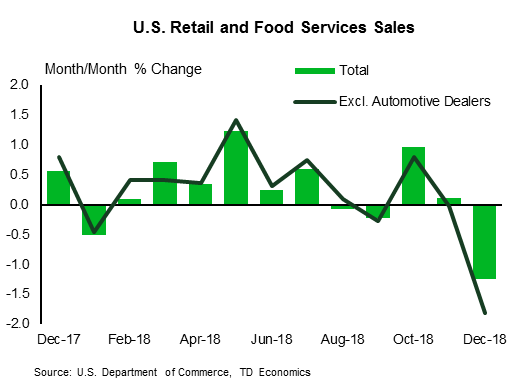

U.S. Retail Sales – January

Release Date: March 11, 2019

Previous: -1.2%, ex auto: -1.8%, control group: -1.7%

TD Forecast: -0.5%, ex auto: 0.0%, control group: 0.4%

Consensus: -0.1%, ex auto: 0.3%, control group: 0.6%

We expect notably weak auto and gasoline sales to drive headline retail sales 0.5% lower in January, following the sharp 1.2% m/m decline in the prior month. Indeed, headline ex-auto sales should come in flat for the month. Lower gasoline station sales should continue to reflect an unfavorable month-on-month comparison in gasoline prices despite their stabilization in January (this should no longer be a major drag in February). On a positive note, we anticipate core retail sales to bounce back 0.4% m/m after December’s unexpected 1.7% tumble.

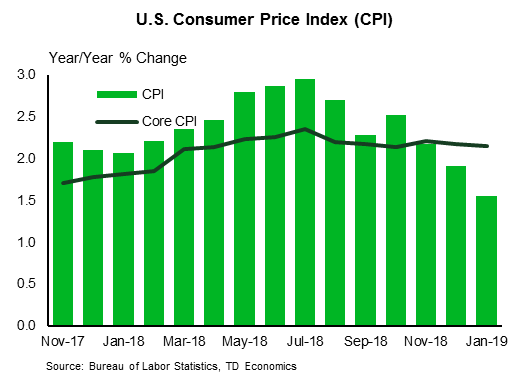

U.S. CPI – February

Release Date: March 12, 2019

Previous: 0.0% m/m; core 0.2% m/m

TD Forecast: 0.2% m/m; core 0.2% m/m

Consensus: 0.2% m/m; core 0.2% m/m

We expect headline CPI to stabilize at 1.6%, reflecting a 0.2% increase with risk for a 0.3% print. Price pressures will benefit higher food and gasoline prices, offset by lower energy services prices. We expect core CPI to print another solid 0.2% increase, leaving the inflation rate unchanged at 2.2%. We expect to see gains in both core goods and services. There is risk for a slight deceleration in shelter, but we expect strength elsewhere across goods and services, including tariff-related categories, medical care and airfares. Looking ahead, we look for headline CPI is likely to remain below 2% until December assuming a modest drift higher in oil prices and core inflation holding slightly above 2%.

Canada: Upcoming Key Economic Releases

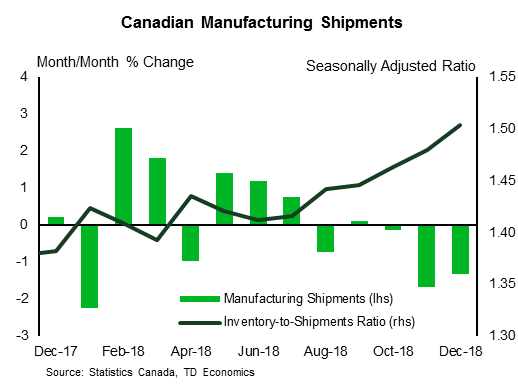

Canadian Manufacturing Sales – January*

Release Date: March 15, 2019

Previous: -1.3%

TD Forecast: -0.3% m/m

Consensus: N/A

TD looks for manufacturing sales to decline by 0.3% in January on weaker motor vehicle shipments, partially offset by a rebound in petroleum sales. US auto production registered the largest decline since the financial crisis in January, which presents downside risks to Canadian output given the highly integrated supply chains. Other transportation equipment categories are also strong candidates for a pullback, with shipments of aerospace products sitting at their highest level since 2016. A rebound in petroleum output will provide a key offset to weakness in transportation equipment; nominal petroleum sales have fallen by 25% over the last two months on a combination of lower prices and refinery maintenance. Gasoline prices stabilized in January, but lower prices for the industrial sector as a whole should allow real manufacturing sales to outperform the nominal print.

{kind=link}