- US markets retreat as healthcare stocks ‘feel the Bern’

- Moves in FX generally subdued, but euro takes a hit after German PMIs

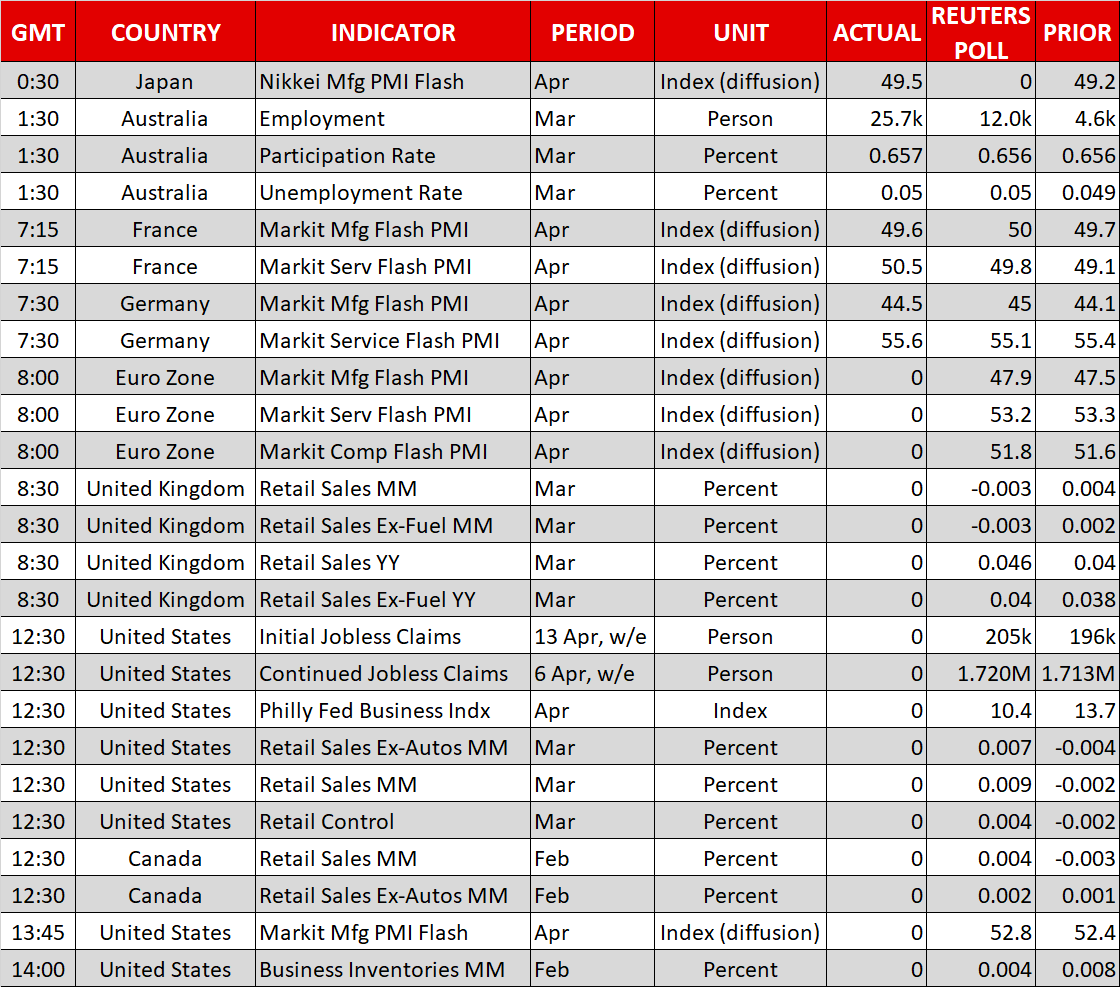

- Retail sales data coming up in UK, US, and Canada today

Wall Street inches down as healthcare stocks weigh ‘Sanders risk’

US equity markets retreated modestly on Wednesday, with losses in the healthcare sector eclipsing encouraging earnings elsewhere. The benchmark S&P 500 fell by 0.23%, weighed down by pharmaceutical giants UnitedHealth (-1.87%), Pfizer (-2.49%), and Merck (-4.72%), among others. The catalyst were some remarks by UnitedHealth’s CEO, who highlighted the potential damage to the sector from policies like ‘Medicare for all’, the flagship proposal of Democratic presidential nominee Bernie Sanders.

Sanders has been gaining ground in opinion polls lately and is currently the front runner out of the Democrats that have entered the race, only behind former Vice President Joe Biden, who has not announced yet. To be frank, this theme will probably grow in importance moving forth. Sanders is an outspoken critic of large pharmaceuticals, banks, and huge multinationals in general – so the more he gains in the polls, the more pain may be in store for such stocks. By extent, this represents a risk for the broader market as well, even though traders haven’t started to focus on the 2020 election yet.

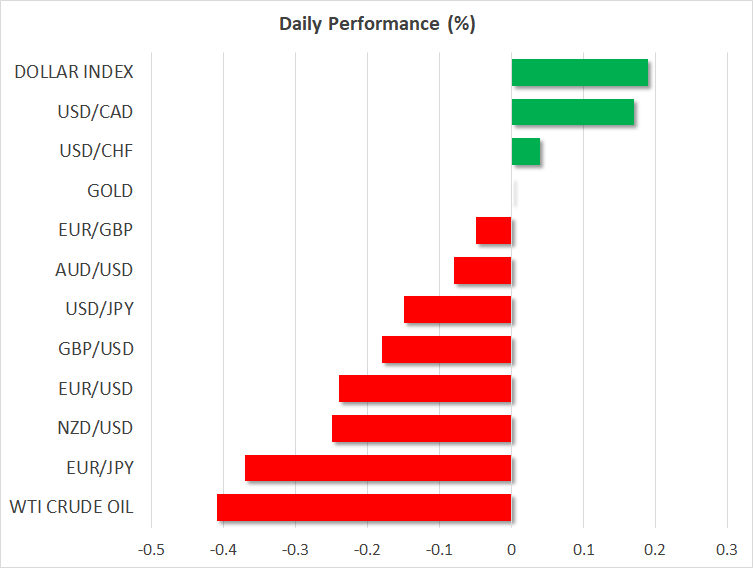

Currencies go nowhere amid light news flow

It was a subdued session in the FX market, with the major pairs trading in relatively wide intra-day ranges, but closing little changed overall. A case in point was the Canadian dollar, which soared after the nation’s core inflation data beat expectations, only to give back those gains in the following minutes to trade nearly unchanged.

Euro takes a hit after German PMIs

Meanwhile, the best performer on Wednesday was the euro, which advanced across the board with a little help from upbeat Chinese GDP data. The slowdown in China seems to have been much less severe than feared, partly due to the vast stimulus rolled out by the nation’s authorities, something that paints a brighter picture for the EU’s massive export industry.

However, the single currency is giving back its gains on Thursday, following the preliminary German PMIs for April. The manufacturing index disappointed, and even though the services print beat projections, that wasn’t enough to calm concerns around growth. Perhaps investors think that the continued weakness in manufacturing will eventually ‘infect’ the otherwise healthy – and far bigger – services sector. Overall, these prints confirm that Europe’s growth engine entered Q2 on a soft footing, and other things equal, they raise the likelihood that the ECB may roll out some more stimulus, or at least that any rate hike may be pushed further back. Consequently, this amplifies the near-term downside risks for the euro.

Coming up: UK, US, and Canadian retail sales data

As for today, the highlights left on the economic calendar today will be retail sales figures out of the UK, US, and Canada.

UK data tend to have a muted effect on the pound lately, so the next ‘big’ move in the currency will probably be driven by Brexit updates, not economics.

The US prints will provide some of the final evidence on how the economy fared in Q1, while similarly, the Canadian figures will be the last piece of the ‘puzzle’ before the Bank of Canada meets next week.

{kind=link}