- Bank of Canada may not be as dovish as markets expect today

- US stocks close at new record highs on blockbuster earnings

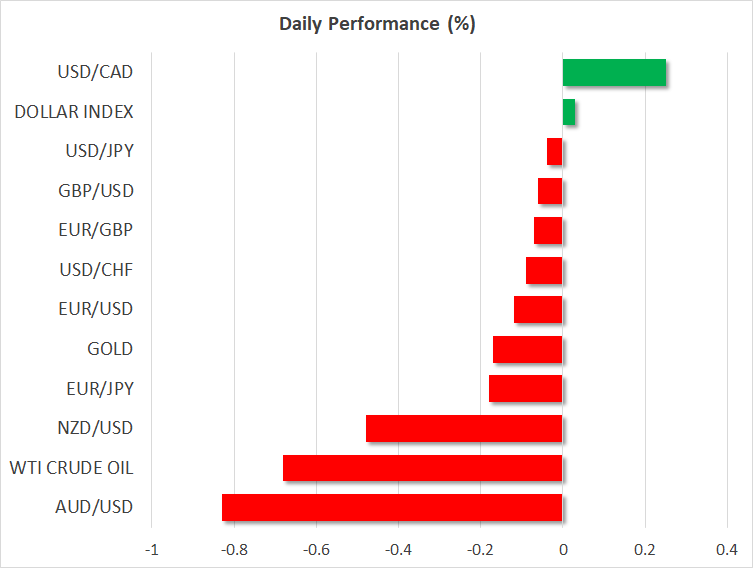

- Dollar rallies amid demand for US equities

- Aussie suffers after disappointing CPIs fuel rate-cut bets

BoC: Cautious, but less than markets expect

The main event today will be the Bank of Canada (BoC) policy decision at 14:00 GMT. No change in policy is expected, so price action will depend on the language of the accompanying statement, the updated forecasts, and Governor Poloz’s tone. The economy hit a soft patch lately, as was highlighted by the BoC’s own business survey for Q1. Wages and house prices have also been struggling – a toxic cocktail for consumers.

In this context, markets seem to expect the central bank to strike an overly cautious tone today, perhaps by abandoning its rate-hike bias completely. In fact, market pricing now indicates a ~50% probability for a rate cut by December. This seems excessively pessimistic. There are still bright spots in the economy, like the rally in oil prices and decent inflation data lately, so officials won’t be in a rush to change their guidance again. Overall, the BoC may be less dovish than markets anticipate, and if so, the Canadian dollar could soar as it finally starts playing catch-up with the oil rally too.

Wall Street hits new records as strong earnings revitalize bulls

US equity markets made headlines on Tuesday. Both the S&P 500 (+0.88%) index and the tech-heavy Nasdaq Composite (+1.32%) rallied to close at new record highs, following some blockbuster earnings from the likes of Twitter (+15.7%). The earnings season in general has been much better than expected so far, with the vast majority of firms beating forecasts, which has reinvigorated demand for stocks.

The earnings season continues in earnest today, with giants like Facebook and Microsoft releasing their results after Wall Street’s closing bell. Industrial bellwethers Boeing and Caterpillar will also announce earnings, and those may be especially important for expectations around broader economic growth, as well as for the Dow Jones.

Dollar finds love amid demand for US equities

In the FX market, the rally in American stocks translated into a rally in the dollar, which outperformed all its major peers outside of the yen. There wasn’t a clear catalyst behind the greenback’s gains. One could argue that the robustness in corporate earnings dampened concerns about a slowdown in the US economy, but the bond market would argue otherwise, as long-term US interest rates fell while the probability for a Fed rate cut by December actually rose.

Hence, the gains in the dollar seem owed simply to demand for US equities attracting foreign funds into America and thus, generating demand for the greenback. Moving forward, the next major market mover for the dollar will probably be the GDP data for Q1 on Friday.

Aussie sinks as inflation miss reinforces RBA rate-cut expectations

Overnight, Australia’s CPI data for Q1 disappointed, with both headline and underlying inflation slowing by much more than expected. The softness likely reinforced market expectations that the RBA could cut rates soon, consequently weighing on the Australian dollar. The kiwi is also on the back foot today, mainly in sympathy to the aussie, as there haven’t been any news from New Zealand.

{kind=link}