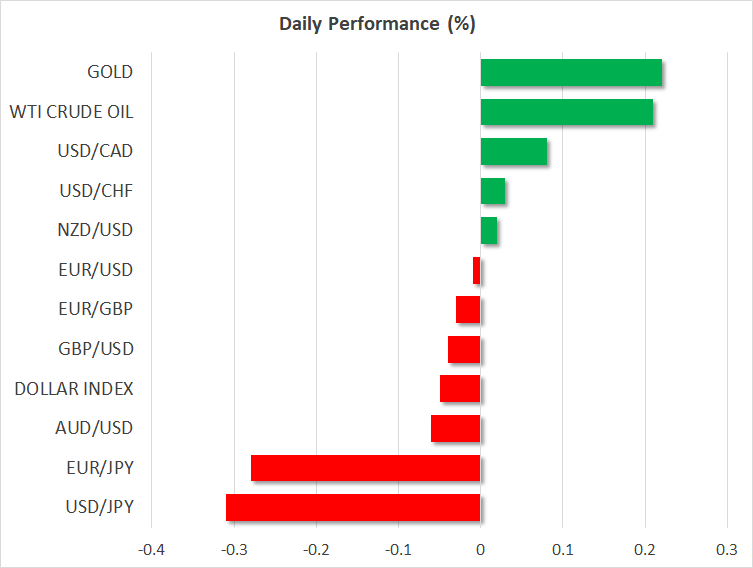

- Dollar index soars to 2-year high as euro, commodity currencies suffer

- BoC remains on hold but abandons rate-hike bias; loonie drops

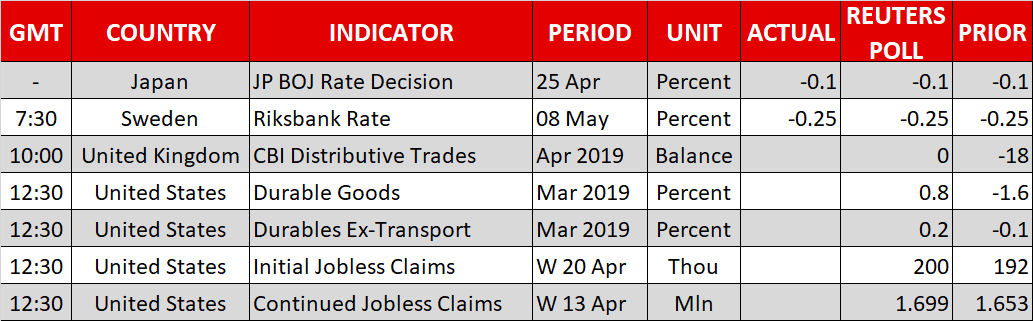

- BoJ commits to low rates until 2020 but yen snoozes

‘King dollar’ returns as euro and antipodeans lose their shine

The world’s reserve currency advanced across the board on Wednesday, with the dollar index soaring to 2-year highs, even without any US-specific catalyst. Instead, the greenback capitalized on weakness in other major currencies, most notably in the euro, aussie, kiwi, and loonie.

Starting with the euro – which holds the biggest weight in the dollar index by far – it fell sharply following a disappointing German Ifo survey, which highlighted that Europe’s powerhouse continues to struggle. If growth in the euro area’s biggest economy is still anemic and its third largest – Italy – is in recession, then a material rebound seems unlikely anytime soon, which implies a ‘lower for longer’ stance by the ECB. Overall, there’s a clear disparity between the European and American economies.

Likewise, central banks in Australia and New Zealand may cut interest rates before long, the Bank of Canada was more dovish yesterday, sterling continues to be tormented by political woes, and Japan offers interest rates so low the yen isn’t attractive. Therefore, the dollar remains ‘the only game in town’ for now, at least until one of these narratives changes, especially the European growth story.

Loonie crumbles as BoC abandons hiking plans, turns neutral

The Bank of Canada (BoC) remained on hold yesterday but slashed its growth forecasts and eliminated any surviving mention to future rate hikes, assuming a clearly neutral bias. Even though there were some hints of optimism, the overarching message was that the Bank sees even lower odds of any future hike, which was enough to push the loonie sharply lower – with a rising dollar exacerbating the move.

Is all hope lost for the Canadian dollar then? Even though a lot will depend on the US dollar and oil prices, the domestic economy doesn’t seem to be in real trouble yet and the bar for any rate cuts may be quite high, despite markets are pricing in a ~55% chance for one by December. In other words, much pessimism is already priced into the battered loonie, so it wouldn’t be a surprise to see a rebound going forward, particularly if oil prices continue to gain.

BoJ commits to ultra-low rates until 2020, but no reaction in yen

The Bank of Japan (BoJ) kept its policy unchanged overnight. To the surprise of no one, policymakers said inflation will take longer than intended to reach its 2% goal, while they also committed to keeping interest rates at current low levels until the spring of 2020. Overall, the BoJ made it clear that policy will stay ultra-accommodative for a prolonged period of time, and yet the Japanese yen did not react. Most likely because no investors were expecting otherwise, given the lackluster inflation and growth outlook.

Going forward, relative interest rates will likely continue to work against the yen. This implies a slow grind lower for the currency, until an episode of risk aversion hits, in which case the yen could gain quickly and immensely.

{kind=link}