Global trade tensions intensified overnight after China’s Commerce Ministry noted China will not make concessions on key major issues. The recent theme over the past several trading days has been mostly negative for trade talk progress. With fading signs that talks will resume, US Stocks remain vulnerable and we could see the S&P 500 poised to break below the May 14th low. Safe-haven currencies, the yen and franc are rising heavily against their major trading partners. World bond markets are seeing Bunds and Treasuries rise as yields slide. The US 10-year Treasury yield is down 2.5 basis points to 2.359%.

This morning, the Parliamentary elections started. Britain and the Netherlands will vote on 99 Members of the European Parliament (MEPs), the UK will get 73 seats and the Dutch 26 spots. When the UK leaves the EU, the Netherlands will then get an additional 3 seats. Between tomorrow and Sunday voting for the rest of the EU will continue, with results coming shortly after the last polling station closes on Sunday.

The weekly jobless claims release shows the US labor market remains strong as claims fell 1,000 to 211,000, roughly in-line with estimates. For Canada, wholesale sales continued the strong batch of data, with the March reading rising 1.4%.

- EUR – EZ PMIs and German IFO disappoint

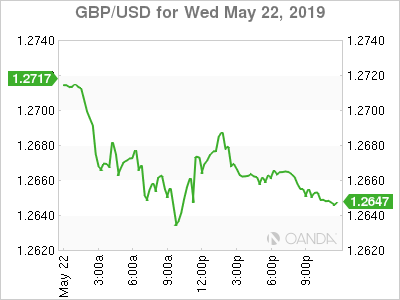

- GBP – 14 consecutive days of weakness to euro

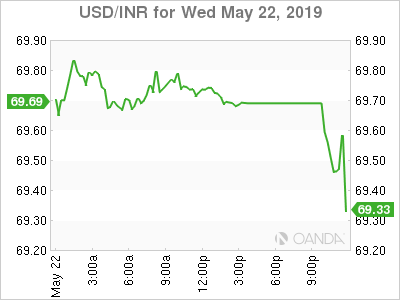

- Modi – Retail sales deliver biggest gain in 10 months

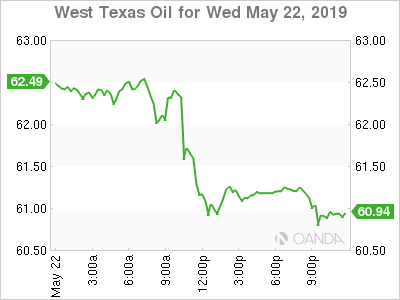

- Oil – WTI dips below $60 a barrel for first time since March

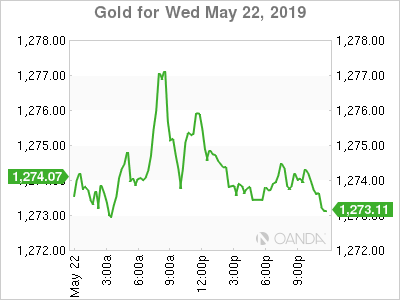

- Gold – Continues to sink as ETF holdings rise

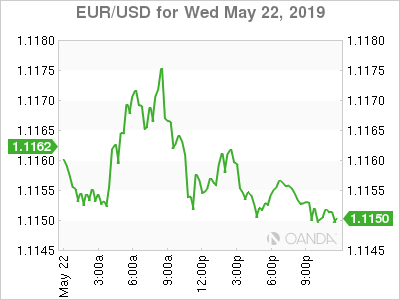

EUR

A wrath of European data dampened prospects that growth concerns were starting to stabilize. The eurozone manufacturing PMI delivered a third straight contraction, which would imply growth of only 0.2% for the second quarter.

The German IFO business confidence declined sharply to 97.9 and missed analysts’ expectations of 99.1. Concerns are growing for German manufacturing as it continues to shrink for possibly a third quarter in a row and fears are growing this will move into the service sector. The base case remains for a strong German rebound in the second half of the year, but we may not be at the bottom yet. Both trade spats between US/China and the US/EU and falling domestic demand for industrial goods will continue to weigh on the German data.

The euro is down 0.1% to the dollar as tentatively finds some support from the 2019 low of 1.1112.

GBP

The British pound’s record losing streak combined with the growing risks that Brexit will see a hard exit, is making fund managers abandon long-term bullish bets. Just a few months ago, the base case was that Brexit would be delivered by PM May and that it would be a soft exit. Now expectations are running high that PM May will give up pushing her Brexit deal and possibly quit on Friday.

If we do see Boris Johnson, the current oddsmaker favorite, become May’s successor, we could see the hardest Brexit occur. Cable, which is currently at four-month lows, could see further pressure target the psychological 1.2000 level and eventually the 2016 lows. No-deal Brexit and a general election risks are likely to keep the pound under pressure.

The European elections could provide a bid for the British pound if we see better results from pro-EU parties.

Modi

India’s polls got the general election right. Prime Minister Narendra Modi’s party celebrated a decisive victory, gaining over 290 seats, well above 272 seats needed to form a government. He now has a clear path to push his second-term policies. The benchmark Sensex rose to a record high but has given back today’s gains and turned negative. The Indian rupee has steadily given back most of the election bump gains.

Oil

Crude prices continue to weaken following yesterday’s EIA inventory data and global demand concerns as the US-China trade war shows no signs of easing. West Texas Intermediate crude’s decline is testing some key technical levels, currently below $60 a barrel, a level that has not been tested since March. Yesterday’s close was below the 50-day SMA, and current weakness is testing below the 200-day SMA. A strong break of psychological $60 level could see further support from the $58.25 level.

Geopolitical risks are taking a backseat with today’s price action, but should eventually incentivize buyers if we see another move lower.

Gold

Gold prices are posting modest gains as trade worries deepen. Talks between the US and China have moved further off course and Wall Street is now expecting a deal to occur beyond summer. Global growth will take a hit from the next round of tariffs. If we see the tariffs remain for over six months, we will likely see the Fed deliver a rate cut. If by the end of the month, we do not see any positive sign that talks are resuming, gold may have a clear path above the $1,300 an ounce.

{kind=link}