The Aftermath

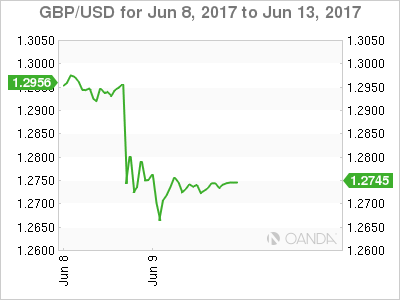

The markets will continue to rethink the Tories diminished Brexit directive, and possible party backlash after May’s snap election wager ultimately backfired and sent parliament into complete disarray.So we should expect much more discussion about and rethinking of the UK’s Brexit position. With May’s leadership teetering on the brink, the UK steps ever so closer to the calamitous Brexit cliff edge scenario.

As for the pound, it remains deadlocked in the 1.2700-50 zone as traders muddle through the election aftermath looking for directional clues. Certainly, prolonged uncertainty would argue for a deeper correction on Sterling as May’s diminished Brexit mandate scenario plays out. However, there are cooler heads in play suspecting the only real option left is the more market-friendly outcome where the UK adopts a European Economic Area styled agreement. A settlement widely perceived as the least ruinous opportunity for the UK and the rest of the bloc. So, expect markets to struggle in the vortex of near-term possibilities clashing with longer term probabilities.

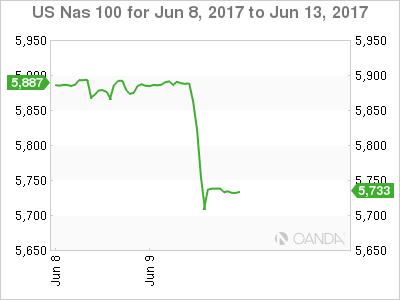

NASDAQ made the Friday afternoon lowlight reel when tech shares pivoted lower driven in part by an apparent flash crash on Amazon shares which dipped nearly 8 % at one point all the while the Dow Jones climbed to record highs. A clear sign of sector rotation in play as opposed to any real shift in fundamentals. While the street was abuzz with talk of a resurgent ‘Trump on trade ‘as both financial and energy stocks gained by week’s end, we remain jaded and pessimistic as that shifting narrative falls a bit too soon and far too optimistic at this stage of the game.

Japanese Yen

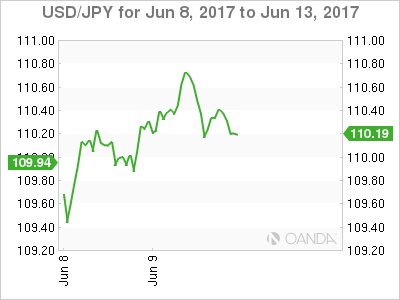

The USDJPY was trading resiliently and showing little signs of post-UK election panic that was until the Friday afternoon swoon on the NASDAQ which .sent the pair toppling over 60 points from intraday highs as risk turned jittery heading into the weekend. I suspect traders opted to play the defensive strategy given weekend headline risk

We‘re left picking up the pieces this morning after Friday’s rollercoaster. While some focus remains on last week’s BoJ QE exit headlines, we view this little more than the BoJ floating an ‘exit” trial balloon.

Risk, on the other hand, has not rebounded in early APAC trade suggesting the markets is sitting tight awaiting more concrete news on the UK political landscape. So far no silver lining in sight as USDJPY trades with an early offered bias and the Nikkei slides

Euro

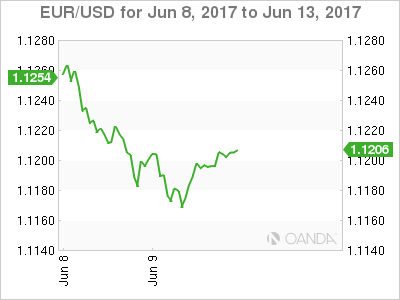

The Euro remains stuck in the mud after the ECB was broadly in line with economists expectations last week. However, with the market anticipating something more on the hawkish side, we could see some more focus on that after the UK election banter fades and EURGBP demand abates.There was a high build up in EURUSD long positioning heading into last week’s ECB, so we could see more near-term EURUSD weakness as ECB hawkish narrative continues to unwind

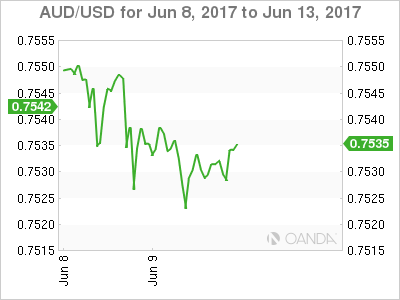

Australian Dollar

Very tight ranges to close the week as the market’s major focus remained on the UK election.But traders are eyeing support holding at .7500-.7525 which bodes will after a solid performance of late. Iron Ore, however, continues to look for a floor which suggests seller will appear on rallies above .7550.

Overall inflation expectations and the employment data have proven supportive of late and another positive print on the Jobs report this week will corroborate the RBA view to look past Q1 weakness and should be supportive for the Aussie.