With rate cut expectations running high following Friday’s disappointing NFP report, the focus for the US dollar this week is firmly on the latest inflation and retail sales figures. The inflation data is released first on Wednesday at 12:30 GMT, followed by the retail sales report on Friday, at the same time. As concerns grow about a sharp slowdown in the US economy, investors will be watching this week’s indicators for more clues about the timing of a rate cut by the Federal Reserve.

Inflation remains elusive

A much-anticipated pick-up in inflation is yet to materialize in a post-financial crisis world, to the bewilderment of economists and policymakers alike, and was a key factor in prompting the Fed to pause its rate hikes at the start of the year. Just a few months later, the Fed has to contend with a deteriorating growth outlook as well and markets are already pricing a 100% probability that rates will be cut twice by 25 basis point each by October.

The first real sign of trouble that the US economy may be fast running out steam came from Friday’s jobs report that showed a big drop in payrolls in May. Hence, any unanticipated weaknesses in the upcoming inflation and retail sales numbers are bound to intensify expectations of a Fed rate cut.

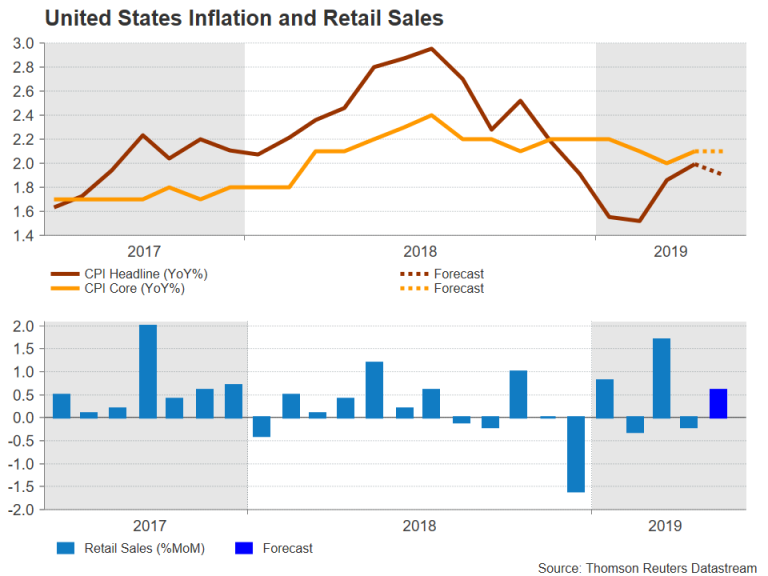

CPI to moderate, retail sales to rebound in May

The US consumer price index is forecast to have increased by 1.9% year-on-year in May, easing marginally from the prior 2.0%. The month-on-month rate is expected at 0.1%, down from 0.3% in April, while core CPI is forecast to remain unchanged at 2.1% y/y. Although the Fed does not monitor CPI inflation as closely as it does the core PCE price index, a fall in the CPI rate would point to cooling inflationary pressures in the economy.

The retail sales figures will be just as, if not more important. Consumption accounts for just under 70% of the US economy so any slowdown in retail spending would point to weaker growth. Retail sales were down by 0.2% m/m in April but are forecast to have rebounded by 0.6% in May. Core retail sales that exclude auto and gasoline sales are predicted to have accelerated from 0.1% to 0.4% m/m. Crucially, the ‘retail control group’ measure, which is used in GDP calculations and excludes autos, gasoline, building materials and food services, is also seen to have bounced back in May by 0.4% m/m.

Dollar may wait for Fed meeting for direction

With the dollar being on the backfoot since the latest eruption in trade tensions, the US currency is looking slightly oversold and could be prone to an upside correction if the data come in at or above estimates. Dollar/yen could overcome resistance at the 50% Fibonacci retracement of the upleg from 104.96 to 112.39, at 108.68, opening the way for the 38.2% Fibonacci at 109.55.

However, the US currency is just as vulnerable to a steep sell-off if this week’s releases add to worries about the economic outlook. Dollar/yen faces an important support at the 61.8% Fibonacci at 107.80. If broken, the bears could pull the pair to as low as 106.55 – the 78.6% Fibonacci level.

A note of caution is likely, though, as the forthcoming data may not provide a clear enough direction for traders, and with the next Fed policy meeting a week away on June 18-19, some investors may choose to sit on the sidelines until then. The Fed will update its economic forecasts as well as its famous dot-plot chart at its June meeting, with the big question being on whether or not policymakers will foresee a rate cut in their projections.

{kind=link}