As heightened trade tensions force central banks around the world to take a dovish turn, the fate of the US-China trade talks will be determined at the G20 summit in Japan. The planned meeting between US President Trump and Chinese President Xi will be the highlight of the week as investors will be hoping for a thaw in the strained relations between the two leaders. Central banks will not totally disappear from the limelight as the RBNZ will hold its latest policy meeting and inflation data from the Eurozone and the United States could provide clues to the ECB’s and the Fed’s next moves.

Eurozone flash inflation eyed after dovish Draghi

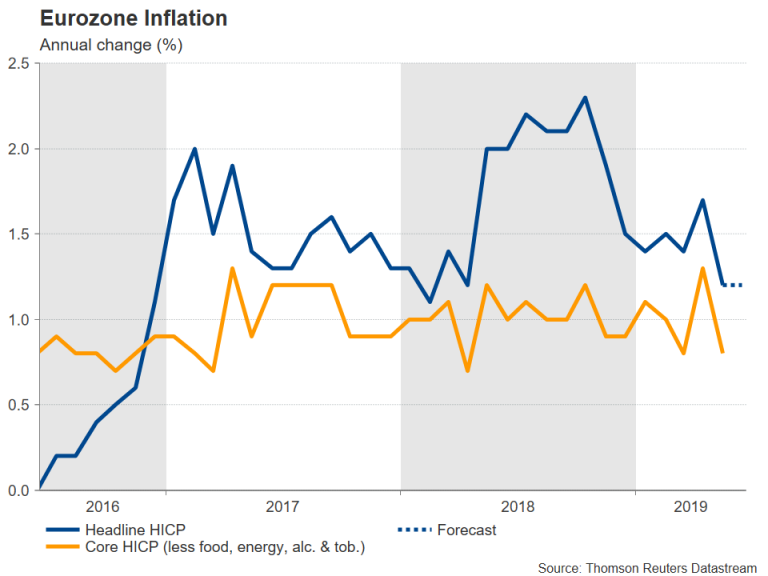

The President of the European Central Bank, Mario Draghi, made it pretty clear this week that if inflation fails to converge sustainably towards the ECB’s target, then “additional stimulus will be required”. This puts the focus on what happens to euro area inflation in the coming months as price pressures have eased substantially this year. Annual inflation fell to 1.2% in May, having stood above 2% late last year. Core inflation has also moderated, with the measure that strips out food, energy, alcohol and tobacco prices declining to just 0.8%.

Headline inflation is forecast to stay unchanged at 1.2% year-on-year when the data is released on Friday. Other data that will be watched from the bloc next week is Germany’s Ifo Business Climate index on Monday and the Eurozone economic sentiment index on Thursday.

The euro’s rebound against the US dollar could be capped if the inflation and business sentiment gauges disappoint as this would take the ECB closer to loosening policy.

UK and Canadian GDP coming up

The Bank of England this week maintained its tightening bias even as more of its peers moved towards a rate cut. However, the bank lowered its forecast for Q2 growth to 0%, stressing the increased downside risks and raising doubts about its own forward guidance. The pound fell slightly on the BoE’s statement and could fall again if Friday’s second reading of Q1 GDP growth is negatively revised.

The Bank of Canada, which dropped its hawkish inclination back in April, could be on the verge of flagging a rate increase again after inflation rose by more than anticipated in May. The next important piece of data for the BoC will be Friday’s monthly GDP estimate for April. A strong showing would further pare back market expectations of a rate cut by the BoC this year and boost the Canadian dollar, which hit 3½-month highs versus the US dollar this week. Another clue could come from the Bank of Canada’s quarterly business outlook survey due on Friday.

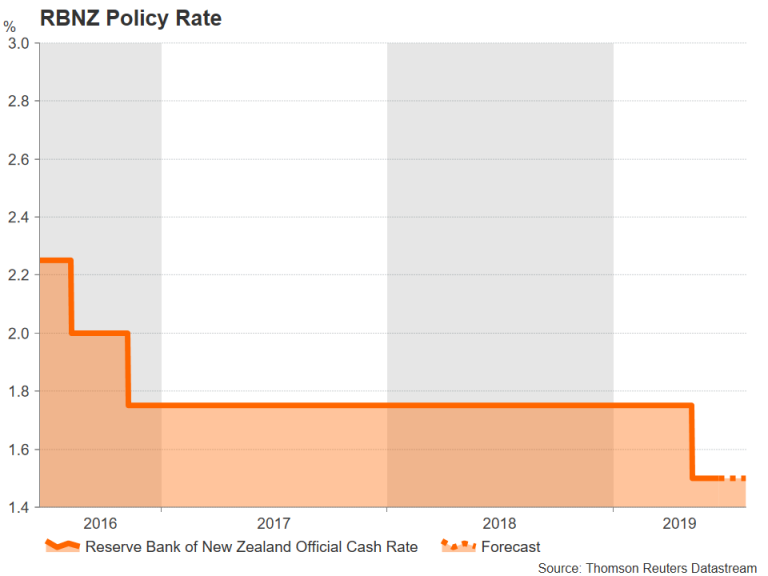

RBNZ to hold rates but more cuts expected

The Reserve Bank of New Zealand became the first major central bank to cut rates in the latest global shift towards looser policy. Following the move at the May meeting, the RBNZ meets again in June but is forecast to hold rates this time round. Recent data out of New Zealand has been more or less in line with the forecasts, with the economy growing by a reasonable 0.6% quarter-on-quarter rate in Q1. However, weaknesses remain such as subdued household consumption and low business confidence. The closely watched Business Outlook Survey by ANZ Bank for June, which is released on Thursday – a day after the RBNZ decision, will be a good indication of where the economy is headed in the coming months.

The New Zealand dollar, which has rebounded modestly from the near the 7-month lows it reached in late May, could resume its downtrend if the RBNZ signals another cut soon.

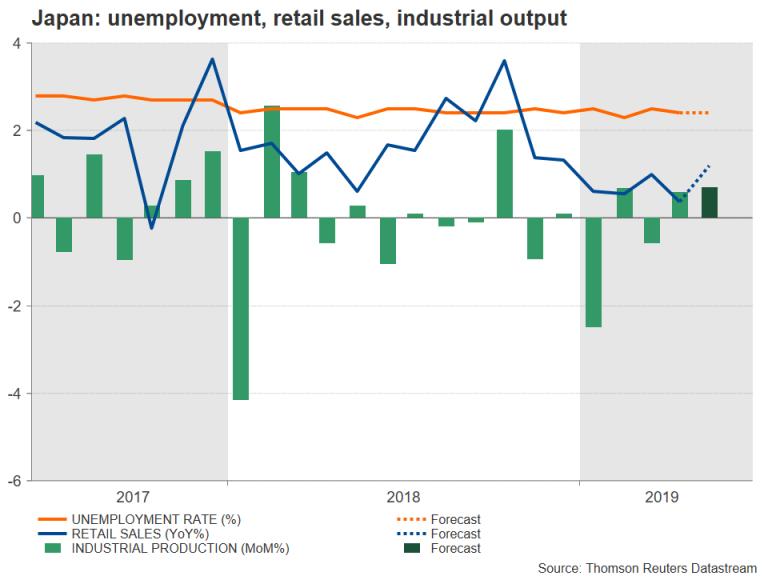

BoJ meeting summary could shed more light on policy direction

The Bank of Japan didn’t join the Fed and the ECB in opening the door for policy easing at its meeting this week. But the Summary of Opinions of that meeting, to be published on Friday, could reveal whether board members discussed at all about expanding the BoJ’s already large stimulus program.

While the bank is more likely to wait until October to see what the impact of the planned sales tax hike will be before taking any action, a stronger yen could prompt policymakers to act sooner. The yen has risen sharply against both the euro and the dollar over the past few days and a sustained appreciation would risk becoming a big drag on growth and inflation.

In terms of data, the May reports for retail sales on Thursday, and industrial output and jobs figures on Friday will be watched out of Japan.

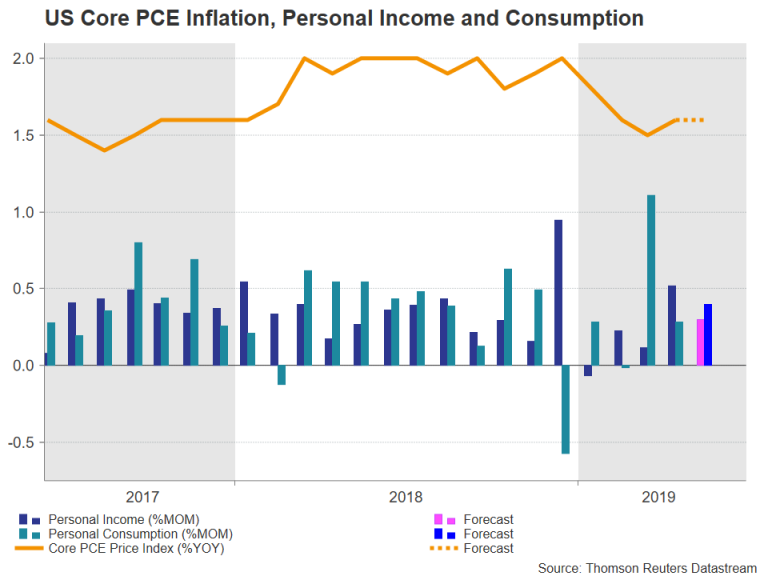

US PCE inflation to be eyed by the Fed

The US will have the busiest calendar next week with plenty of data for investors to digest as they push the Federal Reserve to lower rates at its July meeting. With markets fully convinced that a rate cut in July is a done deal, a broadly strong set of indicators next week would cast doubt on the current doom and gloom about the US economy and probably result in some profit-taking in the dollar crosses, giving the greenback a lift after what looks set to be a very bruising week. The dollar index is on track to finish the week down by 1% following the Fed’s dramatic dovish tilt.

Starting the week on Tuesday are new home sales and the Conference Board’s consumer confidence index. The consumer confidence index rose to 134.1 in May, taking it close to last October’s 18-year high. It’s forecast to slip to 132.0 in June. Durable goods orders will be the main release on Wednesday. They are expected to have increased by 0.2% month-on-month in May, rebounding only marginally from the 2.1% drop in April. On Thursday, pending home sales are due along with the final estimate of GDP growth for the first quarter. No revisions are being anticipated to the annualized rate of 3.1% recorded in the second reading.

The biggest focus for the week though will be on the Personal Consumption Expenditures (PCE) report for May, due on Friday, which of course includes the Fed’s preferred inflation barometer, the core PCE price index. Personal income is forecast to have risen by 0.3% m/m in May, slightly easing from the prior month, but personal consumption is projected to have accelerated a little to 0.4% m/m. The core PCE price index is expected to underline the muted prices pressures in the US as it’s forecast to hold steady at 1.6% y/y, below the Fed’s 2% target. Other data on Friday will include the Chicago PMI.

Few hopes of Trump-Xi breakthrough at G20 summit

There was huge relief when President Trump confirmed that the meeting between himself and President Xi on the sidelines of the G20 summit on June 28 and 29 was back on. However, expectations are not very high that the two leaders will be able to agree to anything substantial given the sudden breakdown in relations after the US accused China of ‘breaking the deal’ and imposed sanctions on Chinese telecom giant, Huawei. But with economic conditions in both China and the US having deteriorated sharply since then, it’s likely Trump and Xi will at least get the ball rolling on restarting scheduled trade talks, which have stalled for the past six weeks.

If Trump and Xi surprise with a major breakthrough, then risk appetite is bound to receive a significant boost, with equity markets likely to be the biggest beneficiaries. However, if the two leaders leave the G20 event without any progress, fears of a global recession would only intensify, keeping central banks firmly on the easing path and pulling US stocks away from their current record highs.

{kind=link}