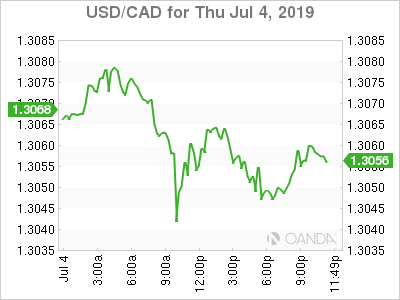

The Canadian dollar was flat on Thursday as the volume in the market was subdued with the Fourth of July holiday in the States. The loonie has risen as the market is pricing in more than one rate cut by the Federal Reserve this year. President Trump continues to pile pressure on the Fed to depreciate the currency via lower rates as he compares the lack of effort from the Fed as what the ECB and other central banks are doing.

The Bank of Canada (BoC) has turned dovish, but not enough to signal a rate cut in the near term. Improving fundamentals have given the central bank some breathing room with steady growth and higher exports.

Next up for the CAD will be the release of the Canadian employment data on Friday. Last month was a pleasant surprise as a small correction was expected after the monster jobs gain published on May 10. The forecast calls for 10,000 positions to be added, but a miss would not be a surprise given the gain in the April jobs report.

US employment has been a steady pillar of the economy, so when the NFP showed a big miss last month it validated the market pricing a Fed rate cut. The lower than expected Jobs report triggered a bout of pessimism about US growth and the need for the Fed to drop its patient stance and go the full 180 degree turn on interest rates.

The US economy could add 165,000 jobs, but given the importance of the indicator a lower number combined with a miss on the wage growth component could be another dagger for the US dollar as it would get the Fed even closer to announcing a rate cut when the FOMC meets at the end of the month.

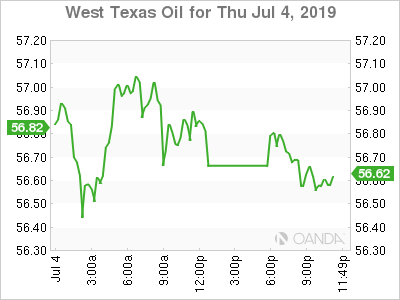

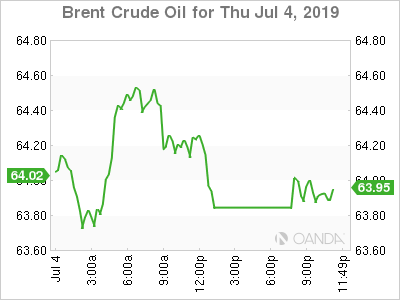

OIL – Oil Lower on Global Growth Concerns

Oil prices fell close to 1 percent on Thursday. The lack of volume due to the US Independence Day was a factor with traders looking for the market to regain full force ahead of the release of the US employment report for June.

US crude inventories registered another drawdown, but given the expectations set by the API a day earlier, it was a miss by shrinking for less than anticipated.

Global growth remains the main factor holding back crude prices. Trade disputes have hurt estimates as more agencies and central banks downgrade growth forecasts as trade headwinds get stronger. Without shutting the door on the US-China dispute, the US has now targeted the EU.

Manufacturing data around the globe is beginning to show signs of deceleration attributed to the trade war. One of the main reasons behind central banks so eager to restart the easing engines is the pressure protectionism is putting on economic growth, so they must step in with more stimulus even though their arsenal is depleted.

The OPEC+ announced a 9-month extension to their production cut agreement, after a successful meeting between Saudi Arabia and Russia in Japan in the sideline of the G20. Russia played hard to get until the end but given the low forecasts they have for internal budget current prices are acceptable. It is the volatility that could put pressure on Russian producers to break away from the group, but that is something for next year to ponder.

The OPEC+ deal will keep prices from falling too hard, but there must be an end to trade protectionism to assure the demand for energy products recovers.

Oil is also under pressure from higher US production. The US is now positioned to become a net exporter and is not bound by the production limit agreement. This could further drive prices lower.

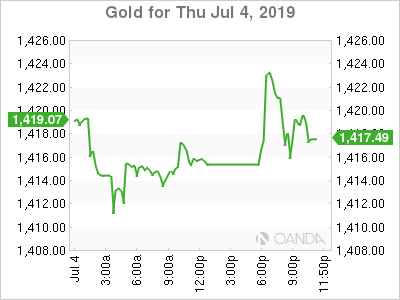

GOLD – Gold Drops Slightly But Awaiting Signs of US Economic Slowdown

Gold fell 0.2 percent during the Thursday trading session. The Fourth of July holiday came at the right time for the US dollar, as it gave the currency time to get its footing after Fed fund rate cut anticipation had depreciated the greenback.

The NFP report on Friday could add another soft data point to the narrative of a slowdown of American growth. The Fed was forced to a 180 degree turn after lifting its benchmark rate in December and being on the verge of cutting the interest rate to avoid a recession.

Gold has risen as the Fed preached patience and is now ready to remove some of the tightening it added last year. The yellow metal is also having a moment as it retakes the safe haven crown away from the US dollar. Trade uncertainty, in particular more than one trade front open at the same time, has given the edge to gold in the eyes of investors.

Despite a cordial meeting between Trump and Xi at the G20, the biggest takeaway was a restart of negotiations. Negotiations that are still far apart in key topics, with neither side willing to concede.

Geopolitical concerns are keeping gold bid, as the Middle East situation could once again flare up with the US taking a less diplomatic approach to Iran and although awaiting a new leader the UK is gearing to get Brexit done once and for all.

STOCKS – Indices Mixed Ahead of US Jobs Report

The Fourth of July holiday made for a low volume day of trading, with most major indices stuck in a tight range awaiting the U.S. non-farm payrolls (NFP) due on Friday. Equities have rallied on the back of a most likely rate cut by the Federal Reserve and the lower than expected US private payrolls report earlier in the week.

The Fed is independent from the White House, even though President Trump has been very aggressive that the US central bank needs to lower rates and depreciate the dollar to make US exports more competitive.

The Fed is likely to cut the benchmark rate later this month by 25 basis points. This fact alone has boosted stock markets around the globe and put pressure on the dollar and bonds.

Emerging markets offer higher yields to investors so they will be more attractive as major economies are looking to cut rates or keep them low.

Risk appetite has improved, but the biggest obstacle for an EM rally is a full-blown trade war. US-China remains unresolved and the US is looking to pick a tariff fight with the EU.

The rally in equities has been driven by dovish central bank rhetoric. The stock market has not been too concerned with the trade war, as the tariffs have avoided hitting consumer goods so far. There is still upside if a true trade agreement materializes between the US and China and the Fed keeps cutting rates as expected.

Geopolitical issues like Brexit, Middle East tensions and the trade war have been an inconvenience, but not enough to derail the record setting pace. A resolution on such fronts could expand the bullish run into next year, but as more headwinds add up it could signal the end of the party.