Markets

A dovish Powell – or the absence of a hawkish one – lifted core bonds for a second day straight. Treasuries outperformed thanks to an acceleration in early US dealings. A mixed bag of (second tier) economic data left neither significant nor permanent marks. US yields eased between 2.1 (30y) and 8.8 bps (2y). The 2y yield faced a minor technical setback by losing the three-weeks old upward trading range. German rates lost about 4.5 bps across the curve. EUR/USD fell in European dealings before the accelerated drop in US yields threw the pair a lifeline. A generally weaker dollar brought EUR/USD to a close of 1.0725 eventually. The back-to-back decline in USD/JPY (153.64) was the first since early March. Japanese officials probably breathe a sigh of relief as the yen appreciates further this morning to just south of USD/JPY 153, easing the immediate need for a third intervention this week. The other two took place on Fed-day (Wednesday), minutes after the US stock market closed (estimated at JPY 3.5 tn) and Monday (JPY 5.5 tn) in thin-liquidity circumstances due to Japan observing a holiday. Japanese financial markets are closed again today and next Monday. Keep an eye out should the yen re-weaken sharply as Japanese authorities apparently like to exploit these kind of trading circumstances. Looking at today’s economic calendar, the April services ISM is scheduled for release in the US. After an unexpected setback in March, the April reading for services is anticipated to recover marginally from 51.4 to 52. The April payrolls report is probably going to grab most of the headlines as Fed chair Powell again cited an unexpected (sharp) weakening of the labour market as one of the paths “in which you could see us cutting rates”. Consensus expects the pace of job gains to ease from a stellar 303k to a still-solid 240k. Wage growth may come in at 0.3% m/m, which is probably still too fast to be consistent with inflation returning to 2% considering that would bring the annualized figure based on the four months of 2024 to more than 4%. After a hawkish repositioning during April and in the wake of the Fed policy meeting, we think short term market risks are skewed towards the dovish side. Figures that fall in line or shy of the consensus are probably enough to extend a correction higher in core bonds, with Treasuries outperforming. This makes the dollar vulnerable for the time being as well, more so against a risk-on background. EUR/USD’s first topside reference is situated at 1.0807.

News & Views

The Czech National Bank unanimously decided to lower its policy rate by 50 bps, from 5.75% to 5.25%. While Czech inflation hit the 2% target in February and March and the CNB lowered its 2024 CPI forecast from 2.6% to 2.3%, risks around the new outlook remain modestly inflationary. Their materialization would bring inflation back to the upper bound of the tolerance band and suggest that the CNB should persist with a tight monetary policy, approaching further rate cuts with great caution. CNB governor Michl at the press conference added that cuts may be halted at restrictive levels if needed. In the meantime, the CNB turned less pessimistic on the economy (2024 GDP forecast 1.4% from 0.6%; 2025: 2.7% from 2.4%). The interest rate path in the new forecasts is significantly higher than three months ago and more in line with levels communicated by CNB members (4.25% end 2024; 3-3.25% end 2025). The CNB board also considers it highly likely that the natural rate of interest has risen slightly compared with the pre-Covid period. Currently, internal models still assume a neutral rate of 3%. The front end of the CZK swap curve underperformed yesterday (2-yr: +5 bps) following the hawkish 50 bps rate cut (which might be the final one of this size). EUR/CZK closed below 25 for only the second time since early February.

Bank of Korea governor Rhee told reporters at an Asia Development Bank conference that it will reconsider the timing of policy rate cut. Growing anticipation that the Fed will keep policy tight for longer, the Korean won’s depreciation and faster-than-expected Q1 growth are the key reasons. “Whether the rate cut timing will be pushed back, how much it will be pushed if it is, or if it will even come will be the question that needs to be reviewed”. The Bank of Korea kept its policy rate stable at the peak level of 3.5% for 10 straight meetings, but flagged the potential of a rate cut later this year given disinflation dynamics. KRW profits with USD/KRW dropping back from 1375 towards 1360, painting a short term technical double top formation on the charts.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut and has broad backing. EMU disinflation will continue in April and bring headline CPI (temporarily) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective. Upcoming CPI readings and a resilient economy/labour market will continue to prevent the Fed to cut rates fast nor deep. September at the earliest, but December is more likely. US yields, especially at the front end, could catch a breather after the recent sharp repricing, but their bottom is well protected.

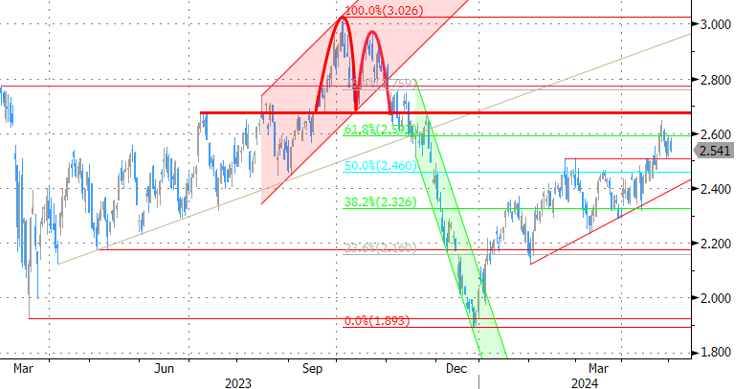

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the previous YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a first break. But after April’s sharp US yield repositioning, we expect some consolidation to weigh on the dollar short term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.

{kind=link}