US stocks slipped from record highs following a wrath of mixed earnings results and despite a strong signal from Federal Reserve officials that they are ready to cut interest rates at the end of the month. With over 15% of the companies in the S&P 500 already reporting second quarter results, investors are hardly celebrating earnings beats from roughly four-fifths of them. The S&P 500 finished the week 1% lower, despite rising easing expectation signals from both the Fed and ECB and positive trade banter from President Trump. The dollar has not tanked as Fed officials do not seem ready just yet to deliver bolder action. With a strong string of economic surprises with labor, inflation and retail sales, it seems the market will need another wave of US data deterioration before seeing policymakers signal a more dovish outlook.

Next week the focus will fall heavily on the global manufacturing PMI data, the ECB rate decision and the US advance reading of second quarter GDP. Tuesday, we should find out if Boris Johnson becomes the next UK PM. On Wednesday, Eurozone and Germany manufacturing data is expected to improve but remain in contraction territory, while both service readings are expected to soften but remain in expansion territory. On Thursday, the German IFO survey is expected to see small improvements with business climate and expectations. Thursday will also see a couple big rate decision from the ECB and Turkish central bank. The ECB should switch to easing mode and queuing up fresh moves in September, while the CBRT will cut rates. On Friday, the first reading of US Q2 GDP is expected to fall to 1.8%, the range of estimates is currently 1.4% to 2.5%. A stronger the expected drop in GDP will likely cement expectations for four rate cuts to occur over the next year. A 2.0% or better reading could see rate cut bets fall to two for the remainder of the year.

- ECB to queue up rate cuts and restart of bond buying program

- FOMC rate cut bets could surge if the US advance Q2 GDP declines sharper than expected

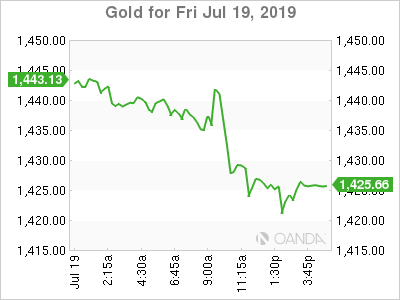

- Gold continued support from lack of trade progress and tensions in Persian Gulf

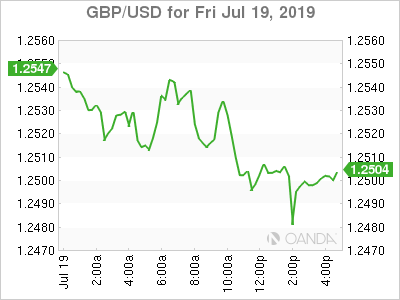

GBP

The UK will finally have a new prime minister on Tuesday after 180,000 members of Britain’s conservative party ballots are tallied. Boris Johnson, a huge front-runner is expected to take over on Wednesday and will face an uphill battle as Tory rebels will try to block Johnson’s no-deal Brexit threat.

This week, BOE Gov Carney noted that divergent outlooks are not unsurprising and that officials will explore how to best illustrate market sensitivities. The Treasury Committee also asked the BOE and Treasury to Brexit economic analysis that presented last November. Monetary policy decisions will likely remain on hold until we have further Brexit clarity.

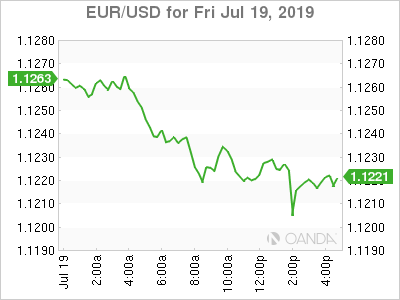

ECB

The ECB observed a quiet period ahead of next week’s rate decision. Press reports circulated that that they could revamp their inflation target, a move that would embolden policymakers to easy policy for much longer. Changes to the inflation target are expected along plans to restart the government bond buying program by November.

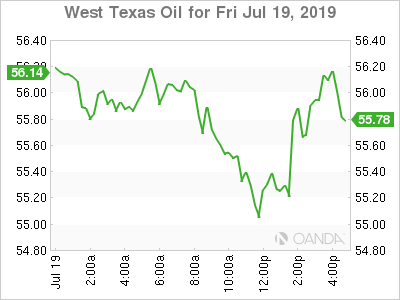

Oil

Crude prices will look to see if they can muster up a rebound as geopolitical risks remain high and as the Fed and other major central banks prepare to open the floodgates of easy money.

Tanker seizures and drones getting shot down will remain common themes that should keep the situation tense in the Persian Gulf and possibly lead to some crude shipping disruptions. Friday’s news that Iran’s Revolutionary Guard seized a British tanker helped squash some optimism that we could see Iran return to the negotiating table.

Oil prices will also pay see limited downward pressure on global manufacturing PMI misses as expectations grow for most of the major central banks poised to deliver stimulus. In 1995, when the Fed finally delivered a rate cut in hope of securing a soft landing, oil prices nearly doubled.

Gold

Gold prices came off six-year highs as investors await the next major development with the trade war or Persian Gulf tensions. Gold’s strong run over the past couple weeks stemmed from dovish banter from the Fed, ECB and PBOC. Institutional investor interest is also growing as low interest rate policy (negative for some) appears to be locked in for the foreseeable future and geopolitical risks remain high,

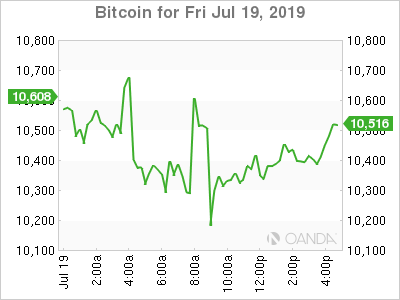

Bitcoin

Bitcoin’s initial rally that stemmed from the interest of Facebook’s Libra currency galvanized regulatory interest that will create major hurdles for all cryptocurrencies. We will likely continue to see the focus remain on regulatory side as CFTC will continue to ramp up crackdown efforts for digital coins.

Bitcoin’s wild ride continues as investors seem unfazed by random 10% swings. If Bitcoin can continue to stabilize next week, we could see bullish momentum return as sellers will continue to unwind short positions.

{kind=link}