U.S. Highlights

- Chinese economic growth slowed 6.2% y/y in the second quarter of this year, as rising trade tensions weighed on activity. Signs of wear are also showing in the U.S., where industrial output continued to grow at a slow pace in June.

- U.S. housing data remains soft. Starts eased in June, while permits dropped precipitously (-6.1% m/m), pointing to more weakness in the pipeline. That said, the services side of the economy continues to hold up well, with consumption providing a major helping hand. Retail sales rose by 0.4% in June, extending the winning streak to four straight months.

- The resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. But, Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness.

Canadian Highlights

- Data this week, while mixed, confirmed that the Q2 growth rebound is on track. Existing home sales held on to recent gains while manufacturing shipments surged. On the softer side, retail sales sank and inflation eased, but remains on target at 2.0%.

- With a rebound in Q2 largely a done deal, attention shifts to third quarter growth prospects. The Bank of Canada projects a cautious 1.5% rate in Q3, implying a notable slowdown would be required to spur policy re-think from the BoC.

U.S. – Resilient Consumer Unlikely To Change Fed’s Mind

The first half of July, which was marked by a G20 meeting and major Fed communications, was a hard act to follow. But this week still offered plenty of kick, with political developments and a few primary data releases dominating headlines. Of note, tensions in the Persian Gulf remained high with the U.S. claiming that it shot down an Iranian drone in the Strait of Hormuz. The U.S.-China trade spat also continued to reverberate, with President Trump stating that trade talks still have “a long way to go” and calling for an inquiry into Google’s work with China.

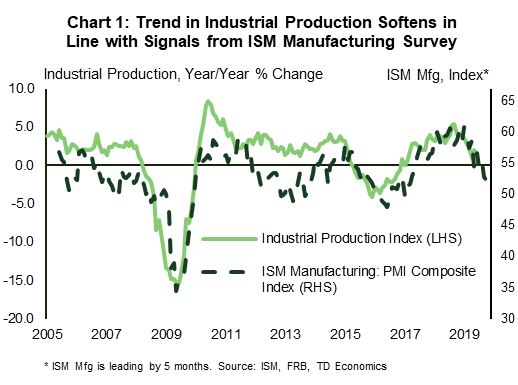

The trade blows are inflicting wounds on both sides. Figures out this week showed that Chinese economic growth slowed to 6.2% year-on-year – the slowest pace in 27 years, with output in secondary industries (construction and manufacturing) decelerating to 5.6% from 6.1% in the first quarter. In the U.S., industrial output continued to grow at a slow pace in June, in line with signals from the ISM manufacturing survey (Chart 1). The impact of the trade conflict is not confined to manufacturing. An annual NAR survey showed that Chinese home purchases in the U.S. fell by 56% in the 12-months ending in March.

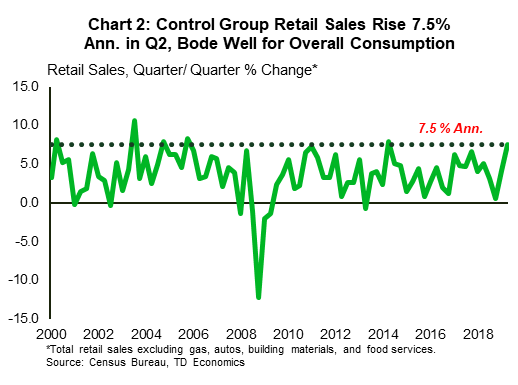

The good news is that despite all the challenges (trade-related or not), the larger services side of the U.S. economy continues to hold up well. The Fed’s Beige Book corroborated this narrative in what appeared to be another steady-as-she-goes report for the mid-May to early-July period. Consumer spending is providing a major helping hand. Retail sales extended their winning streak to four straight months, with the tally up 0.4% in June. Sales in the ‘control group’, which excludes volatile categories and is used in calculating GDP, rose by an even more impressive 0.7%. With the month prior also receiving a slight upgrade, control group sales in the second quarter advanced 7.5% annualized – the strongest showing since mid-2014 (Chart 2). This bodes well for real consumer spending in the second quarter, which we expect to come in at around 4% annualized – a strong rebound from the sluggish start to the year.

Housing data, on the other hand, remains soft. Starts edged lower in June (-0.9%) and have generally moved sideways in recent months. Building permits, however, fell precipitously on the month (-6.1% m/m), suggesting some weakness is still in the pipeline. Despite a favorable demand backdrop and relatively low and falling interest rates, new construction is struggling to kick into higher gear. A lack of buildable lots, labor shortages and increased production costs remain key hurdles.

Looking past housing challenges, the resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. However, several Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness. Still, should the data continue to hold up, the case for limited stimulus (i.e. only 1-2 cuts) is likely to prevail.

Canada – Mixed Data Largely Confirms Q2 Growth Rebound

This week offered investors a deluge of top-tier data releases largely confirming that Canada’s second quarter growth rebound is on track. Financial markets were mixed, with the TSX trading sideways and the Canadian dollar slipping late in the week on a soft retail trade print. Movements in oil prices made headlines, with WTI plunging by around $5, likely owing to a confluence of factors, including consternation about global growth prospects. Meanwhile, Canadian bond yields followed the lead of their global counterparts, heading lower also on concerns about the health of the world economy.

On the data front, existing home sales kicked off the week. Despite taking a breather in June, sales were up 5% in the second quarter, boding well for overall growth. Rising activity is certainly welcome, but we float the possibility that sales growth should have been even stronger than the 2% (year-to-date) increase seen so far. After all, mortgage rates have fallen by 75-80 bps by some measures and labour markets remain healthy. Moving forward, these same factors should keep activity on an upward trajectory.

Other data released during the week was more mixed, with a healthy rise in manufacturing sales coming alongside a sharp drop in retail volumes and decelerating consumer price inflation. In May, manufacturing volumes were up a sturdy 1.7% (m/m), partly on a reversal of transitory factors in the auto sector, but also on gains in other industries. However, a rise in inventories to their highest on record took some shine off the headline, as the unwind of these bloated levels will restrain growth in coming quarters.

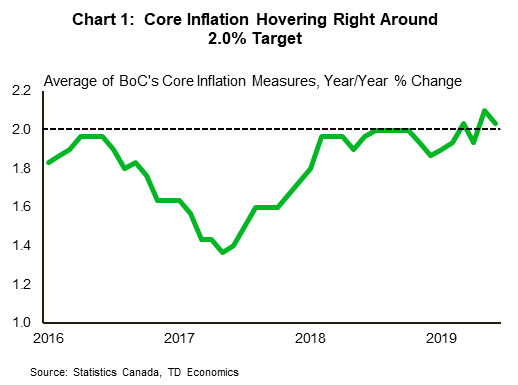

On the softer side, retail spending volumes sank 0.5% (m/m) in May, the sharpest decline in several months, and consistent with our call for more modest household spending in Q2. Headline consumer price inflation also eased up a notch, falling to 2% (y/y) from 2.4% in May. The average of the Bank of Canada’s core inflation measures also came in at 2%, down a tenth of a point from May. Despite falling in June, inflation remains well behaved and provides little cause for concern for policymakers (Chart 1).

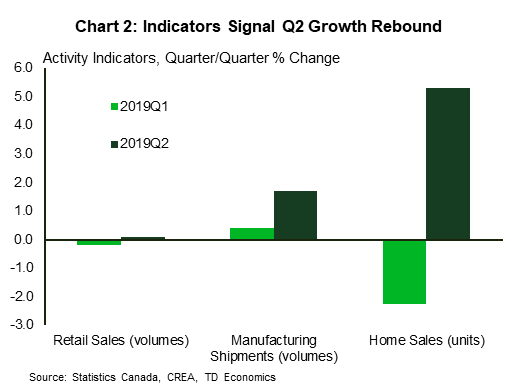

Bringing it all together, data this week mostly reinforced the (well-worn) notion that economic growth strengthened in Q2 (Chart 2). With this outcome all but guaranteed, attention shifts to third quarter growth prospects. The Bank of Canada expects third quarter growth to slow to a sub-trend 1.5% rate. This suggests that a material slowdown would have to manifest to surprise policymakers and cause some re-think on their current neutral stance. Our own forecast sees the economy chugging along at a trend-like pace in the third quarter and beyond, thus allowing policymakers the leeway to remain on hold for the foreseeable future. Of course, the global growth backdrop has softened, representing the most clear and present danger to this view.

U.S.: Upcoming Key Economic Releases

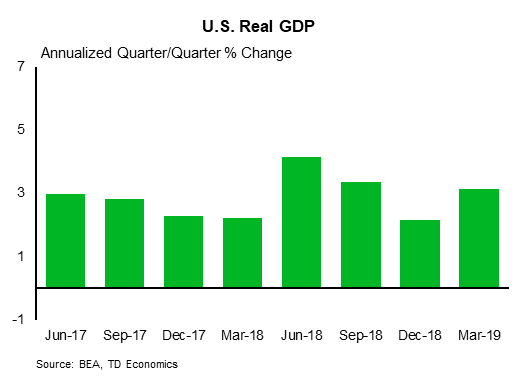

U.S. Real GDP – Q2

Release Date: July 26, 2019

Previous: 3.1%

TD Forecast: 2.0%

Consensus: 1.8%

We expect GDP to advance a near-trend 2.0% q/q saar in Q2, down from a strong 3.1% print in Q1. Unlike the prior quarter, we expect consumer spending to be a key engine of growth, rebounding to about 4% after a wobbly start to the year. Business investment, however, continued to slow in the face of global growth concerns and heightened trade uncertainties. Inventories and net exports, key contributors to growth in Q1, were likely a drag on activity in Q2.

{kind=link}