The US dollar is lower against major pairs on Friday after the U.S. non farm payrolls (NFP) came in lower than expected by 30,000 jobs. The final data point was 130,000, while not raising alarms as it still points to a solid employment sector it does put more pressure on the Fed to cut rates when the FOMC meets in September 17/18. Incoming data next week would be crucial as inflation and retail sales are due on September 12 and 13.

Risk appetite made a comeback this week as risk events eased with HK pulling its extradition bill, no-deal Brexit knocked back as Boris Johnson was dealt heavy political defeats and the US and China got on the phone. The European Central Bank (ECB) will be the main event when it announces its monetary policy decision on Thursday, September 12 at 7:45 am EDT followed by President Draghi’s press conference at 8:30 am EDT.

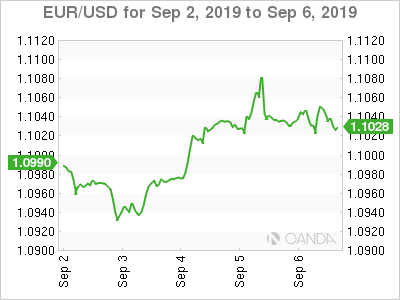

EUR/USD All Eyes on ECB Decision and US Inflation and Retail Data

The EUR/USD is trading at 1.1043 on Friday after the U.S. non farm payrolls (NFP) came in lower than expected. The single currency trades higher by a small margin of 0.08% due to the upcoming ECB rate decision. Markets have fully priced in a 10 basis point rate cut this week, taking the deposit rate to -0.5%.The ECB may not stop there though and previously claimed to be exploring various other options including more QE which currently looks the most likely, possibly accompanied by other measures aimed at limiting the negative effects of negative deposit rates on banks in the region.

The ECB could disappoint as it did at the last meeting and could do again, potentially on the other extraordinary measures that markets expected. EUR has been trending lower in anticipation of more stimulus and with Lagarde due to take over in November, there is scope for the central bank to hold off for now.

US-China to hold high level trade talks on October

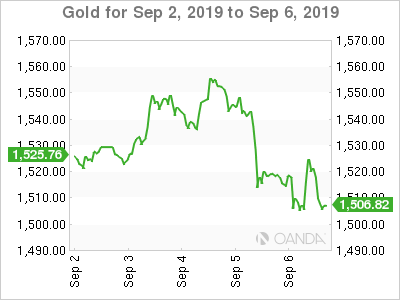

The big news this week was that an actual phone call between China and the US took place and has resulted in trade talks between Beijing and Washington to take place in October. Vice Premier Liu He and U.S. Trade Representative Robert Lighthizer got on the blower to try to de-escalate their tariff conflict. The US-China trade war has been a major negative factor in global growth factor and has kept safe havens bid as investors have flocked to gold, JPY and CHF. Global stocks have risen as the result as trade optimism is once again in vogue. Gold is down 2% on Thursday, but almost flat on weekly trading on the idea of a possible trade deal.

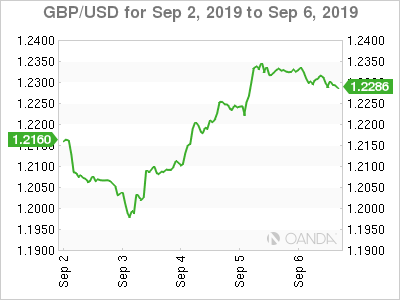

Brexit is the story that keeps on giving with a snap election the next possible step. Boris Johnson has suffered a series of parliamentary defeats that have reduced the probability of a no-deal Brexit. Weekend developments could influence the pound as we enter the final stretch of the EU-UK divorce.

Hong Kong protests still ongoing but protestors scored a major victory with the withdrawal of the extradition bill, but they are pushing for their other four demands, and have met with silence from China. There could be a military response from China over the weekend, stoking the fire and risk delaying the trade talks if the international community condemns the use of force.

Brexit

After events in Parliament this week, the country looks to be headed for an election, possibly as early as 15 October, two days before the European Council summit.

A number of defeats this week has left Boris Johnson wounded and, it seems, without any other options ahead of the 31 October Brexit deadline, which is now likely to be extended.

The situation may still change though and there could be plenty of drama ahead of Parliament being suspended next week.

The pound is extremely sensitive to Brexit developments and the weekend is typically littered with appearances from various politicians. This weekend is likely to be no different which could impact the pound on the open next week.

Commodities

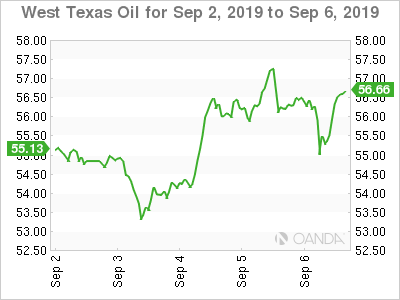

The US-China trade talks have eased some of the pressured on commodities. Oil prices have improved with some solid data out of the US, and a large drawdown this week as reported by the EIA. Developments on the Iran-US front and the efforts of France and the EU to bypass US sanctions could unlock Iran’s oil reserves and put pressure on the black stuff.

Low demand and higher production from OPEC are keeping crude prices from rising too fast. Commodities are sensitive to trade war rhetoric. Escalations from either side will result in lower commodity prices.

Market events to watch this week:

Monday, September 9

- 4:30am GBP GDP m/m

- 4:30am GBP Manufacturing Production m/m

Wednesday, September 11

- 10:30am USD Crude Oil Inventories

Thursday, September 12

- 7:45am EUR Main Refinancing Rate

- 7:45am EUR Monetary Policy Statement

- 8:30am EUR ECB Press Conference

- 8:30am USD CPI

Friday, September 13

- 8:30am USD Retail Sales m/m

*All times EDT