Highlights

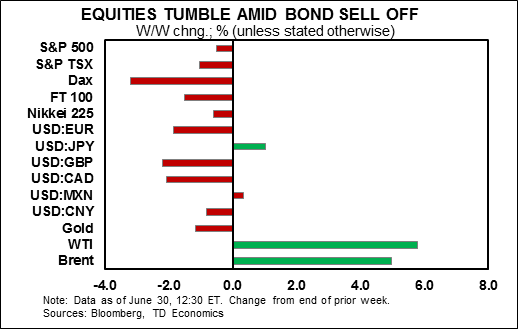

- Bond markets sold off sharply this week on remarks from monetary policymakers. Bond yields rose by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed.

- Momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward.

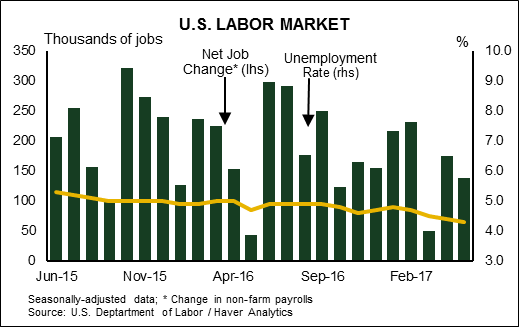

- We look forward to next week’s employment report as a potential market mover. We expect a relatively robust print of 170 thousand jobs and unemployment to hold steady at 4.3%.

U.S. – Hawkish Central Bank Rhetoric Rattles Markets

Global markets were volatile in recent days. Bond markets sold off sharply since mid-week on remarks from monetary policymakers. Central bankers in the Eurozone and the UK have indicated that meaningful economic improvements should begin to warrant the removal of accommodative monetary policy measures. This hawkish sentiment saw bond yields rise by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed. The relatively softer U.S. data also led the dollar lower vis-à-vis the euro and the pound.

The lower U.S. dollar also helped to shore up oil prices that have been led higher recently by curtailed production related to maintenance of Alaskan sites and a storm in the Gulf of Mexico. Still, US stockpiles have remained high this summer, with oil prices likely to remain relatively anchored during the rest of the year.

Expectations of less-stimulative policy going forward have also led stock markets to retrench as investors across the Atlantic readied themselves for what may be end an era of cheap money. At the same time, comments by Fed Chair Janet Yellen on Tuesday indicated that the Fed is keeping a close eye on stock markets valuations, injecting further caution into U.S. equity markets.

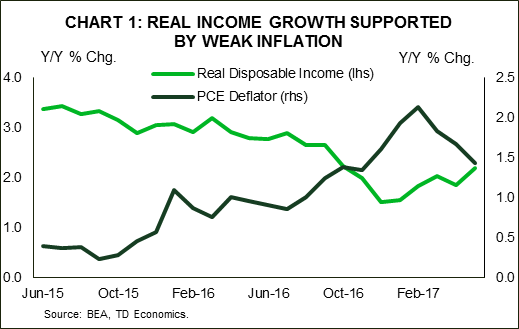

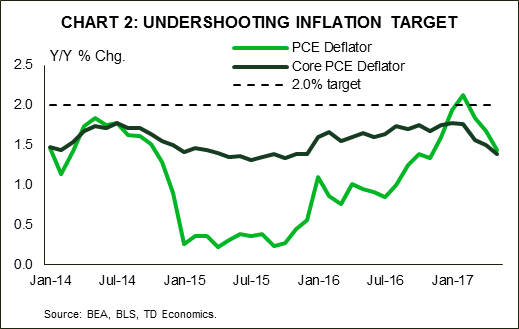

Still, the U.S. data came in relatively weak this week. While still supportive of growth in the second quarter, momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward (Chart 1). But, this was partly related to the weakness in prices, which underperformed in May, corroborating anemic CPI growth on the month (Chart 2). There was also weakness in durable goods orders, which fell in May according to the advance estimate, suggesting weaker capital investment in the second quarter.

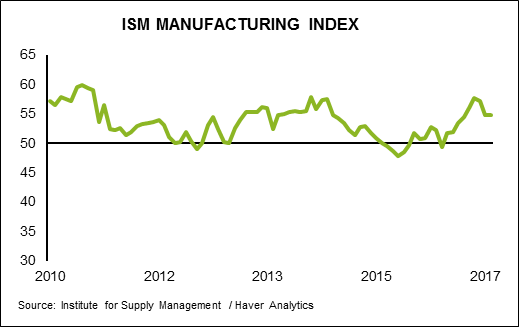

But, not all data were soft. Consumer confidence metrics rose according to both the Conference Board and University of Michigan surveys. Moreover, the goods trade balance narrowed slightly in May as automotive exports rebounded following two consecutive months of underperformance. With domestic US auto sales peaking last year, global demand will play an increasingly important role for growth in the sector. Exports should also get some support from a weaker greenback. We look forward to next week’s ISM manufacturing survey results to echo these positive developments, with readings poised to expand, mirroring upbeat regional surveys for June.

The string of data that has missed expectations recently has been leading markets to push out the timeline for further rate hikes, with another hike this year now priced in below 50%. This is particularly the case for inflation, which has been stubbornly weak, while wage growth has recently lost some momentum too. We look forward to next week’s employment report as a potential market mover. We expect a relatively robust print of 170 thousand jobs and unemployment to hold steady at 4.3%. Moreover, with unemployment near its natural rate, we expect that wage growth should once again accelerate. This should help underpin the inflation outlook and could bolster the case for another rate hike by year end.

Canada – Rate Hikes Coming, Just A Matter Of When

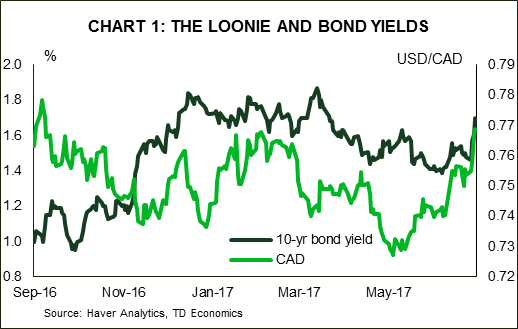

It was a good week for Canada’s loonie, as it pushed above 77 US cents to a 9-month high. Oil prices provided some support, moving back above US$45 per barrel.

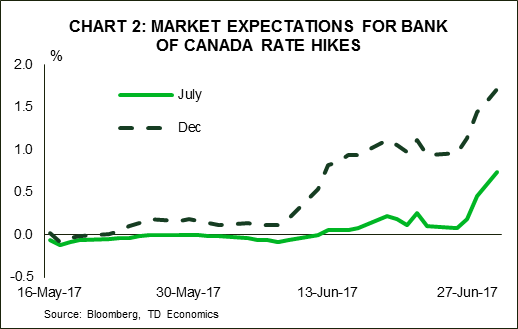

However, the more important driver of currency strength of late has been the Bank of Canada, where hawkish remarks by senior officials over the past few weeks have prompted markets to bring forward expectations of when the tightening cycle will begin. Comments from Governor Poloz this week – that rate cuts have done their job and excess capacity is being used up – echoed this sentiment, signaling that it is no longer a question of if the Bank of Canada will hike rates, but when. As of this morning, markets had priced in a nearly 80% chance that the Bank will hike the overnight rate at the next meeting in July. As a result, 5- and 10-yr bond yields rose by about 25 basis points on the week to a 3-month high.

The Bank of Canada is clearly responding to the stellar growth that the Canadian economy has recorded in the second half of last year and first quarter of 2017. And, this momentum has carried over into the second quarter. This morning’s April GDP report showed that the economy expanded by 0.2% during the month, putting it on track to meet our expectations of 2.9% (annualized) for the quarter as a whole. This should help to close the output gap – or eliminate the excess capacity – in the current quarter.

Moreover, this morning’s release of the Business Outlook Survey – which the Bank of Canada tends to put a lot of weight on – showed that business activity is continuing to gain momentum. Firms expect sales growth to improve further and hiring intentions shot up to record levels. Still, inflation expectations edged down, with the bulk of respondents forecasting price growth in the 1-2% range.

Price pressures are perhaps the only thing missing that would solidify a July hike. All of the Bank’s core measures of inflation have been flat or trending down this year and remain on the low end of the 1-3% target range. And expectations among businesses suggest that inflationary pressures will be limited. However, monetary policy acts with a lag. And given that the Bank of Canada’s research suggests that core inflation should be bottoming, it could very well feel that a July hike is justified.

All told, the heat of the continued rhetoric by Governor Poloz this week, strong growth data and associated market reaction are all working in the direction of a rate hike at the central bank’s July 12th fixed announcement date. At the same time, however, inflation is still the Bank of Canada’s single mandate and has yet to show any signs of moving toward target. As such, although markets have priced in a hike for July, we believe there is little risk of waiting a bit longer (i.e., October). This will give the Bank a little more time to ensure that inflationary pressures are beginning to materialize as expected, and to obtain more clarity surrounding the impact of recently announced housing measures in some regions, as well as the direction of oil prices. Should the Bank of Canada hike rates in July, markets should be cautious about pricing in too much additional tightening given the soft inflation backdrop.

U.S.: Upcoming Key Releases

U.S. ISM Manufacturing Index – June

Release Date: July 3, 2017

May Result: 54.9

TD Forecast: 55.5

Consensus: 55.0

TD looks for ISM Manufacturing to strengthen to 55.5 in June on a broadening improvement in regional soft data. ISM-adjusted empire manufacturing reached a six-year high in June and while the Philly Fed Index drifted lower on an ISM-adjusted basis, it still remains near cycle-highs and firmly entrenched in expansionary territory. Chicago PMI also surprised to the upside in June, coming in just shy of the previous cycle high set in 2011. This should bode well for market sentiment, though we note that inflation and hard data are far more important for the Fed in the current environment.

U.S. Employment – June

Release Date: July 7, 2017

Previous Result: 138k, unemployment rate 4.3%

TD Forecast: 179k, unemployment rate 4.3%

Consensus: 180k, unemployment rate 4.3%

We expect June nonfarm payroll employment to pick up to a respectable 170k pace in June after registering a disappointing 138k gain in May. At this stage of the cycle we expect gains above 200k to be fewer and far between, though upside surprises cannot be excluded. We do expect, however, job gains to remain above its breakeven pace needed for further declines in slack (estimated at roughly 80-100k). Jobless claims have stabilized near record lows, household sentiment (e.g., Conference Board) has stayed robust and business survey indicators (regional Fed indexes) have also maintained recent strength. On balance, both hard data and surveys point to a June pickup, though we await additional labor market measures (ISM in particular) before finalizing our forecast.

The unemployment rate is expected to be unchanged at 4.3%. The number of unemployed workers fell for four consecutive months through May, which at this stage of the cycle looks unsustainable. With some stabilization in June paired with ongoing employment growth, we see risks as balanced for a stable reading for the unemployment rate. On wages, calendar effects point to a stronger 0.3% m/m increase in average hourly earnings, leaving the year-on-year pace higher at 2.7%. With realized inflation becoming a more deciding factor on the path of future rate hikes, wage growth will be key to watch in the coming months amid heightened concerns over the Phillips curve.

Canada: Upcoming Key Releases

Canadian International Trade – June

Release Date: July 6, 2017

April Result: -$0.37bn

TD Forecast: -$0.80bn

Consensus: N/A

The international trade deficit is forecast to widen to $0.80bn in May on a sizeable pullback in energy exports and an increase in import activity. Non-energy exports should post a moderate decline and add to the drag from energy, where a sharp decline in prices will overshadow a flat or modest increase in volumes. We see downside risks to motor vehicle exports after a sharp decline in manufacturing shipments and a deteriorating outlook for US auto sales new countervailing duties on softwood lumber, announced in late April, should weigh on exports of forestry products. Factory prices will also weigh on nominal exports, having fallen 0.2% on the month. On the other hand, we see import activity edging higher on robust domestic demand.

So the goods-export revival is not quite happening and Canada’s competitive positive position remains under challenge, mainly due to high unit labour costs relative to the US and Mexico. In addition to the potential drag we may get from housing activity in May, the second quarter could mark the top to Canada’s economic rebound. This is probably as good as it gets and the summer could be bumpier than what we have been accustomed to lately.

Canadian Employment – June

Release Date: July 7, 2017

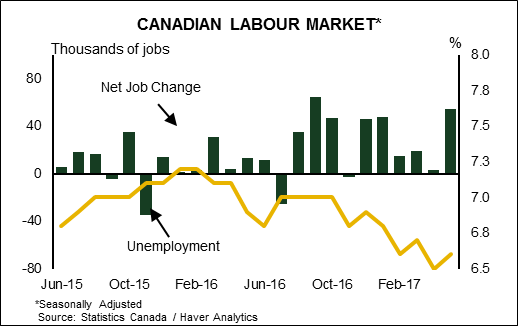

May Result: 55k, unemployment rate 6.6%

TD Forecast: 5k, unemployment rate 6.6%

Consensus: N/A

Canadian job growth is forecast to slow to a 5k pace in June after the robust 55k in May. Details should add a downbeat tone to the report, as we expect to see a partial reversal of last month’s rotation into full time and private sector hiring. Manufacturing employment should cool after surging 25k jobs in May, its strongest month since 2002. We expect finance, insurance and real estate (FIRE) employment to remain soft amid a slowdown in the Toronto housing market. The unemployment rate should remain stable at 6.6%, but the risks are skewed for it to drift lower to 6.5% on a moderation in labour force growth.

While we look for a number of sharp improvements in April’s report to unwind partially, we expect policy makers to look through the weakness in any single month and focus on the encouraging trend that has solidified over the last six months, although the market reaction could be higher than normal, especially if we get a miss, given the current speculations surrounding an upcoming rate hike.