U.S. Review

Fundamentals Continue to Support Festive Holiday Spending

- Despite easing for the fourth consecutive month, confidence still remains near its cycle high in November as consumers continue to focus on their own economic prospects, while discounting political drama out of Washington D.C. and concerns from abroad.

- The health of the labor market, low gasoline prices and a stock market near record highs continue to underpin our expectations for solid consumer spending growth in the fourth quarter, albeit at a substantially slower pace than the robust rates seen in the prior two quarters.

Fundamentals Continue to Support Festive Holiday Spending

As the Thanksgiving holiday compressed the economic indicator schedule into the first half of the week, market attention remained squarely focused on the data performance in order to gauge the overall health of the U.S. economy during the final months of 2019. In particular, this week’s consumer-related indicators were of keen interest as the unofficial kickoff of the holiday shopping season, including Black Friday and Cyber Monday, is now upon us.

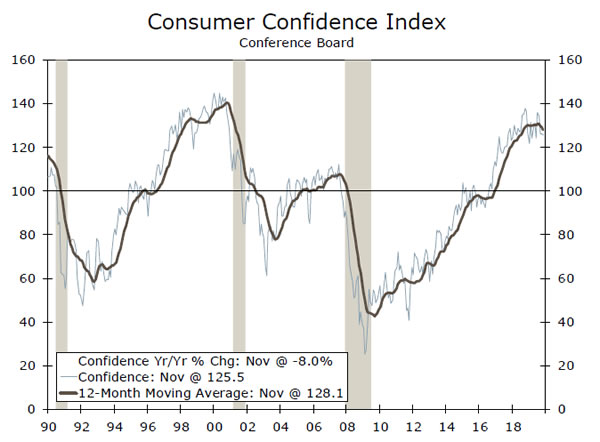

With regards to the consumer, the landscape remains largely positive, though we have witnessed some evidence that supports our expectation for an easing in the pace of consumer spending growth in coming quarters. Consumer confidence, as measured by the Conference Board, unexpectedly eased in November to a level of 125.5. While this marks the fourth consecutive month of declines, consumer confidence remains in elevated territory (top chart). In addition to a still-healthy labor market, low gasoline prices and a stock market running near record-high levels continue to suggest that the major drivers of confidence remain supportive of solid consumer spending growth.

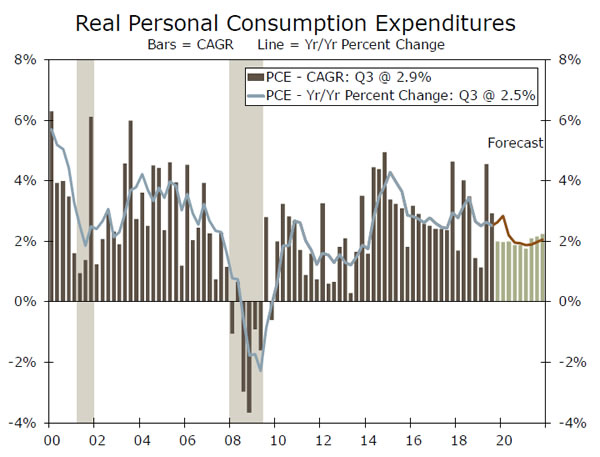

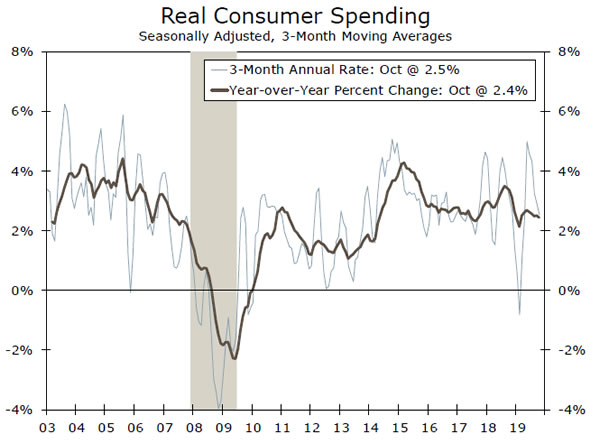

Despite the lackluster confidence performance, retail sales and other measures of consumer spending remain on track for moderate growth in the current quarter. On an inflation-adjusted basis, consumer spending is running at a 2.5% annualized rate over the past three months (middle chart). While marking a deceleration from stronger rates of growth recorded in prior months, the trend pace still suggests consumer spending growth should hold up reasonably well in the fourth quarter.

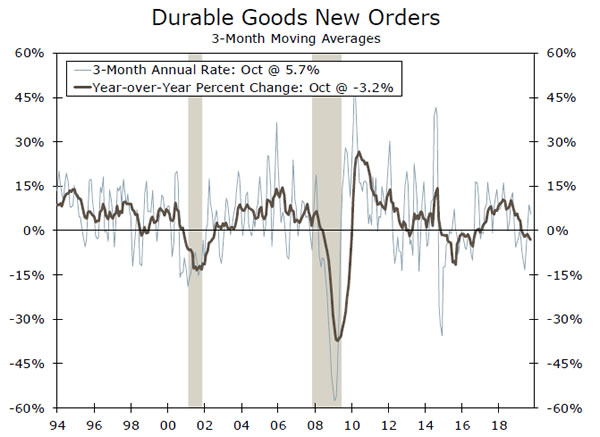

Turning to the factory sector, the advance reading of October durable goods orders beat expectations, rising 0.6% over the month. Encouragingly, core capital goods shipments–a proxy for business equipment spending–also unexpectedly increased, posting the largest monthly gain since January. While the October performance offers a glimmer of hope that manufacturing activity could be stabilizing, the trend in orders growth remains lackluster and thus likely to limit any potential capex gains.

Collectively, this week’s indicator performance does little to change our perspective on the near term outlook. The dichotomy between the consumer and factory sectors continues, with the former still expected to provide the lion’s share of support to overall GDP growth for the foreseeable future. No doubt, the consumer has been the linchpin of growth in extending economic expansion this year, especially in light of heighted trade tensions, political drama out of Washington D.C. and slowing global growth. While we expect consumers’ resilience to continue, we are mindful that the robust rates of spending growth in Q2 and Q3 will not likely be repeated any time soon. While consumer spending growth should remain steady at about a 2% pace in coming quarters, we currently project U.S. real GDP to increase at a more modest 1.2% annualized rate in Q4, and maintain a sub-2.0% pace of growth in the first half of next year.

U.S. Outlook

ISM Manufacturing Index • Monday

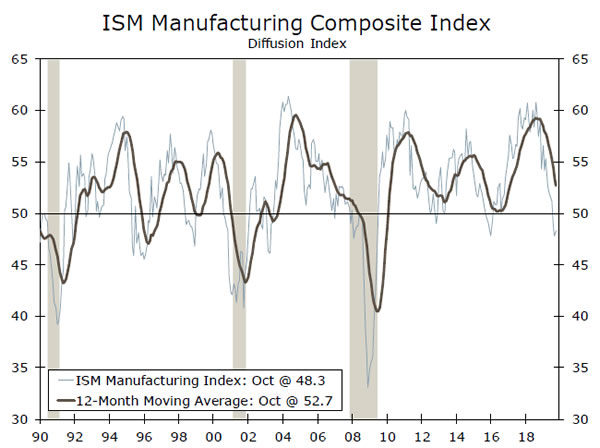

The ISM manufacturing index has been in contraction territory for three straight months. However, as the chart to the right shows, you can have dips below 50 for a few months and still avoid recession.

The most recent period that looks similar to this one was late 2015. Then as now, you have some calling what is going on in the factory sector a “manufacturing recession.” Given the fact that many businesses are still operating at capacity and having trouble finding skilled labor, that may be an overstatement, but there are clearly a number of headwinds confronting manufacturing today.

Until the uncertainty surrounding the trade war goes away, we do not expect a return to pre-trade war highs in the ISM index. But if there is no further escalation in the trade war in 2020, as we expect, then a modest improvement seems likely, though we do not expect to see much of a mover here in the November reading next week.

Previous: 48.3 Wells Fargo: 48.9 Consensus: 49.5

International Trade • Thursday

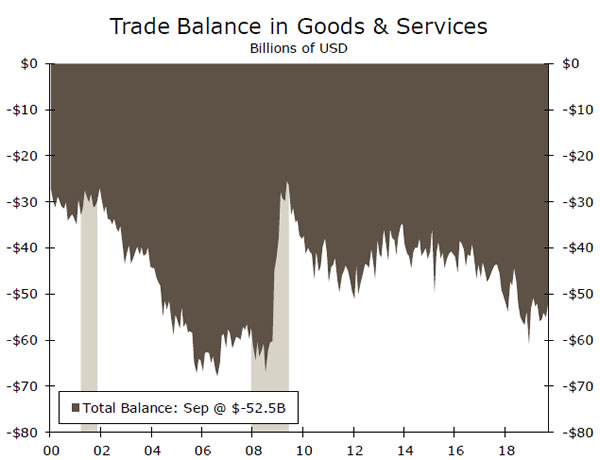

Speaking of trade, next Thursday we will get an indication of how trade is shaping up in the fourth quarter.

The advance goods trade balance reported earlier this week indicated a significant slowing in U.S. goods imports in October, which is the month the latest round of new trade tariffs against China took effect. The decline in goods imports combined with a smaller decline in goods exports points to a narrowing in the October trade deficit, all else equal. An unexpected surge in services exports or a cratering in service imports could soften the blow, but our baseline expectation is that the trade deficit will narrow.

That is a plus for fourth quarter GDP, at least in terms of the arithmetic, as a smaller deficit means a slight boost even if the big driver behind that narrowing is a steep decline in goods imports.

Previous: -$52.5B Wells Fargo: -$48.2B Consensus: -$51.5B

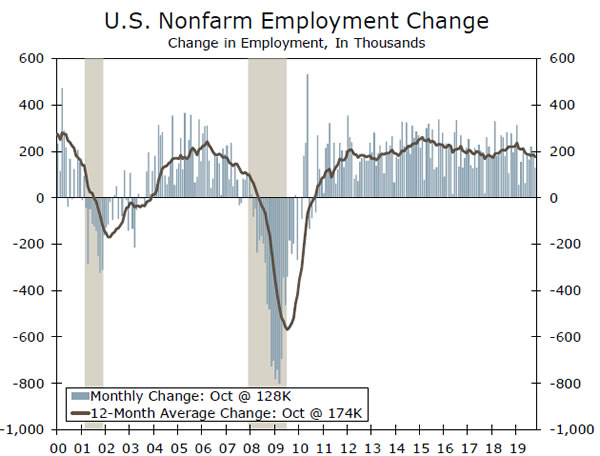

Employment • Friday

The job market in the United States remains quite strong, though more than 10 years into this expansion, it is starting to show its age. The U.S. added over 200K jobs each month in 2017 and 2018, on average. In 2019, that average monthly growth rate slowed to 167K.

Layoffs have remained low, but an uptick in jobless claims in recent weeks raise a suspicious eyebrow. There have also been layoffs the past two months in the manufacturing sector. An optimist might point out difficulty finding skilled labor and how that may be holding back the pace of hiring. That is certainly true, but the 36K manufacturing jobs lost in October throw some cold water on that.

Still, after adding just 128K jobs in October, some improvement is expected in November. A faster pace of job growth would offer some assurance to the Fed and the markets that the economy really is in “a good place” after all.

Previous: 128K Wells Fargo: 190K Consensus: 190K

Global Review

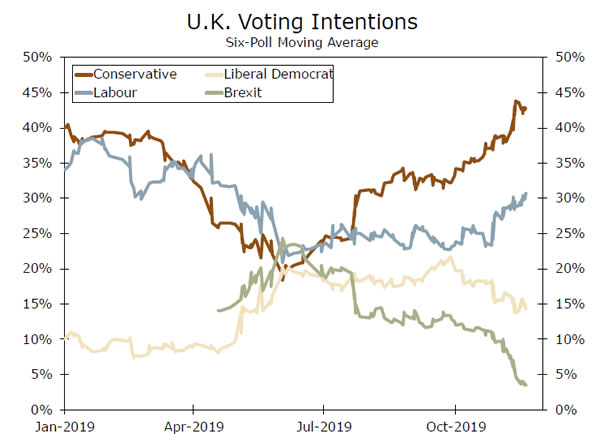

Boris Johnson Commands Lead in U.K. Polls

- A series of U.K. general election polls released this week continue to show Boris Johnson’s Conservative Party with a significant lead over the opposition Labour Party. The current margin of support points to a parliamentary majority for the Conservatives, although much can still change over the next two weeks leading into the election.

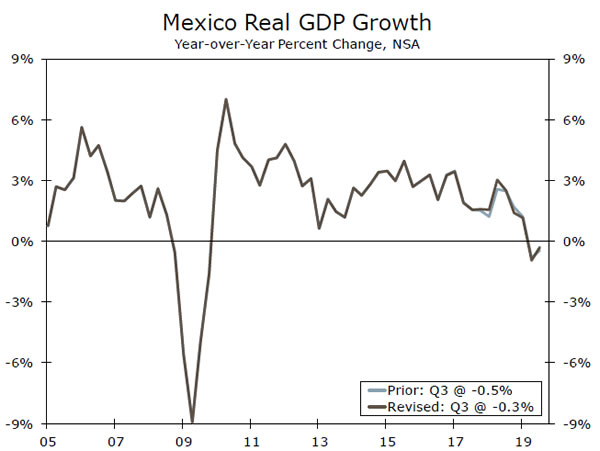

- It was a quiet start to the week for international data releases. Sentiment figures from Germany rebounded very slightly but still point to especially sluggish economic growth, while revisions to Mexican GDP figures showed the economy contracted for three straight quarters starting in Q4-2018.

Polls Still Favor Boris Johnson

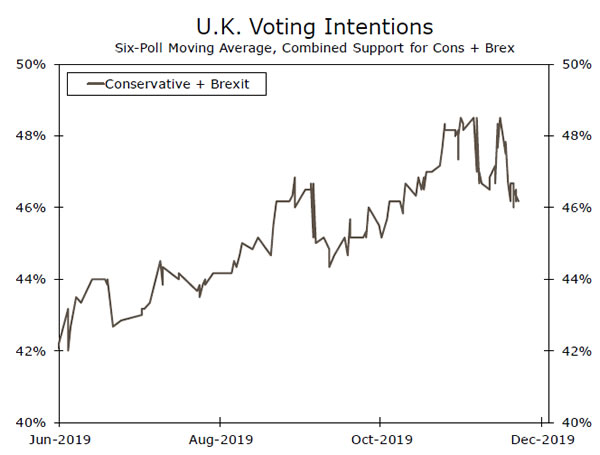

In the United Kingdom, polls continue to suggest Boris Johnson’s Conservative Party has a commanding lead ahead of the December 12 general election. If the election were held today, we would be surprised if the Conservatives did not win a majority in U.K. Parliament. That said, there are still about two weeks until the election, and polls can still shift meaningfully before then. Support for the Conservatives has already leveled off and ticked lower after a multi-month surge. This likely reflects the fact that much of the run-up that began in October was merely a sign of waning support for the Brexit Party, whose candidates have dropped out of a number of key races. In fact, combined support for the Conservatives and the Brexit Party has fallen almost back to where it was at the start of October (top chart). Still, the Conservatives have a comfortable margin over the opposition Labour Party at this point, and our base case is that the Conservative Party will win a parliamentary majority in the upcoming election, allowing it to shepherd through a Brexit withdrawal deal and move on to longer-term trade talks with the European Union.

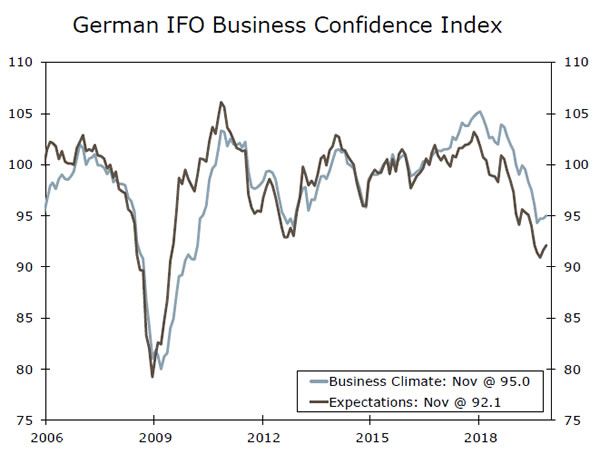

It was a quiet start to the week in terms of data releases from major international economies. One release that stood out was Germany’s IFO business confidence index for November, which showed a modest recovery in sentiment but not quite as strong as some had expected. The overall index ticked higher to 95.0, although that was mainly driven by a rise in expectations as the current assessment was more or less stagnant. These sentiment readings are indicative of the broader state of Germany’s economy at present—stagnating, but not in a full-scale recession. There have been some other signs of initial stabilization in Germany’s economy, and the Eurozone economy more broadly, of late. German factory orders appear to have bottomed out, while the Eurozone manufacturing PMI ticked higher in both October and November, albeit modestly. These figures are again reflective of the overall story of the Eurozone economy, which appears to be stabilizing but is unlikely to recover particularly quickly. For more detail on this topic, please see our recent special report.

Looking beyond the developed world, Mexico released comprehensive GDP revisions, which showed output declined for three straight quarters starting in Q4-2018. Overall, however, the revisions did not meaningfully alter the trend in annual real GDP growth in Mexico (bottom chart), and we doubt they will have any real impact on monetary policy. Meanwhile, economic activity data were also released for September, which showed a stronger than expected 0.3% sequential rise in output during the month. The strength in growth at the end of Q3 bodes well for the Q4 GDP reading, although we would be surprised to see a very strong growth number. For one, the ongoing softness in the U.S. economy is likely to keep a lid on Mexican economic growth, while real interest rates of roughly 5% are also holding back the more interest-rate sensitive sectors of Mexico’s economy, including investment spending.

Global Outlook

Brazil GDP • Tuesday

Brazil’s economy has languished in recent years, as real GDP growth has averaged just 1.5% on an annualized basis since the country emerged from recession in 2017. After nearly three years of recovery, real GDP is still nearly 5% below its previous peak in 2014. The sluggish pace of recovery is likely owing to a few factors, including depressed commodity prices, still-restrictive monetary policy and domestic political uncertainty. That said, on the latter issue, we note Brazil’s success in passing landmark pension reform earlier this year. The reform may not be a panacea for the country’s economy, but the government is making efforts to build on its momentum by working toward other comprehensive reforms. Meanwhile, the central bank has already cut rates 150 bps this year and more easing could be on the way. None of this changes the reality of low commodity prices and anemic global growth, but improving domestic conditions could help lift Brazil’s GDP growth rate moderately in the coming quarters.

Previous: 0.4% Consensus: 0.5% (Quarter-over-Quarter)

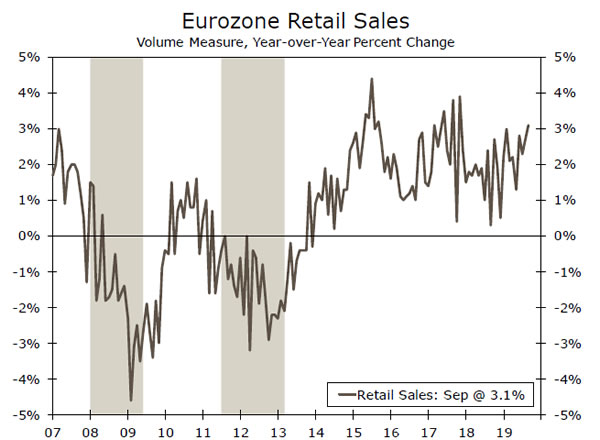

Eurozone Retail Sales • Thursday

2019 has been a year that has pushed manufacturing sectors across the globe to the brink, but services sectors have generally been resilient, driven by solid consumers. Nowhere has that been truer than in the Eurozone, where the gap between manufacturing and services sentiment reached the widest since 2008 last month.

That is not to say that consumers have been unaffected. Indeed, employment growth has weakened and growth in hours worked has slowed. However, overall real income gains have been sturdy enough to keep the consumer chugging along for now, and the ongoing strength in the retail sales data support that narrative. With services sentiment remaining subdued thus far in Q4, we would not be surprised if retail sales slowed a bit during October. Still, the available data are not concerning enough to call for a more significant or prolonged slowdown in consumer activity.

Previous: 3.1% (Year-over-Year)

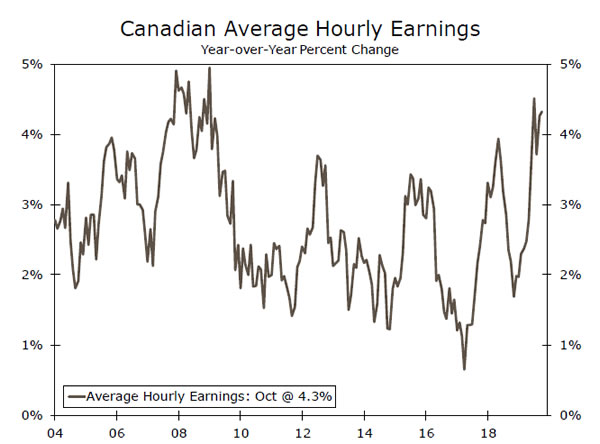

Canada Employment Report • Friday

Canada’s labor market has been red hot this year. Employment growth has averaged around 36,000 jobs per month in 2019, the strongest year for job growth since 2002. A substantial portion of that growth has come from full-time jobs as well, an encouraging sign, while growth in average hourly earnings is up more than 4% on an annual basis.

We would not be surprised to see some moderation in employment growth in Canada in the months ahead. It is simply hard for Canada to sustain above-trend employment gains in an environment of lackluster global growth and low commodity prices, while we also note that underlying domestic demand in Canada remains fairly soft. Also of note next week will be the Bank of Canada monetary policy announcement, which we cover in more detail in the Interest Rate Watch section on page 6.

Previous: -1.8K (Net Change in Employment)

Point of View

Interest Rate Watch

BoC—We’re Going Steady

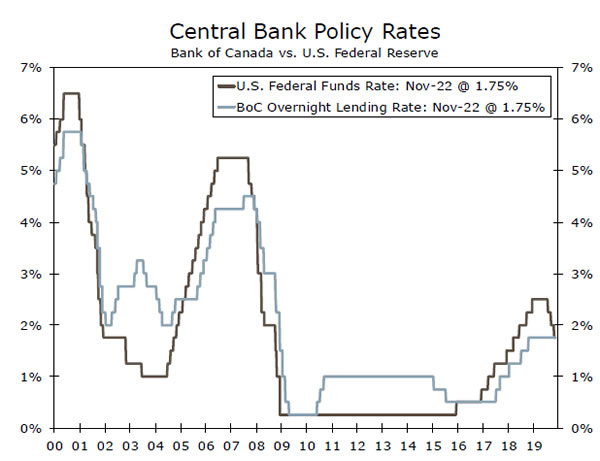

Given the close integration of the American and Canadian economies, it is not surprising that there is a fair degree of correlation between monetary policy rates in the United States and Canada (top chart). Indeed, the Bank of Canada (BoC) was following the Fed higher throughout most of the FOMC’s tightening cycle in 2015-2018. So when the FOMC started to cut rates earlier this year, many observers, ourselves included, thought that the BoC would follow suit, at least to some extent.

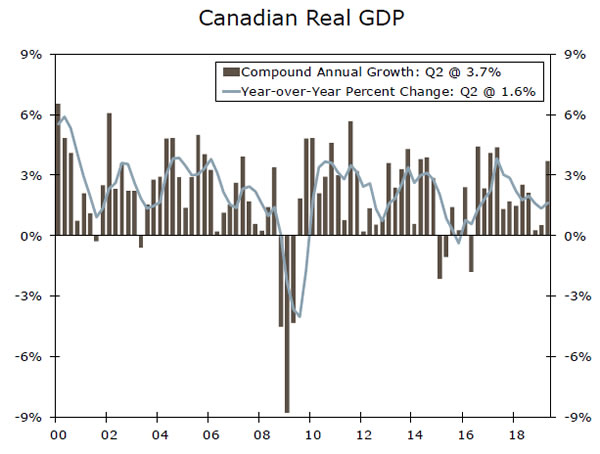

Real GDP growth in Canada has generally slowed this year, in line with the economic deceleration that has occurred in the United States (middle chart). Although Canadian GDP growth rebounded markedly in the second quarter, it seemed that conditions were still ripe enough for policy easing. The statement that was released at the conclusion of the last policy meeting on October 30 was widely interpreted as dovish, which bolstered expectations for a BoC rate cut on December 4.

However, BoC Governor Poloz threw cold water on those expectations last week. Poloz said that the BoC “had monetary conditions about right given the situation.” The Governor went on to say that interest rates at current levels are “still stimulative,” and he also noted that BoC officials had considered a rate cut at the October 30 policy meeting but ultimately decided against it given how well the overall economy is performing. Consequently, we now expect that the Canadian central bank will maintain its main policy rate at 1.75% for the foreseeable future.

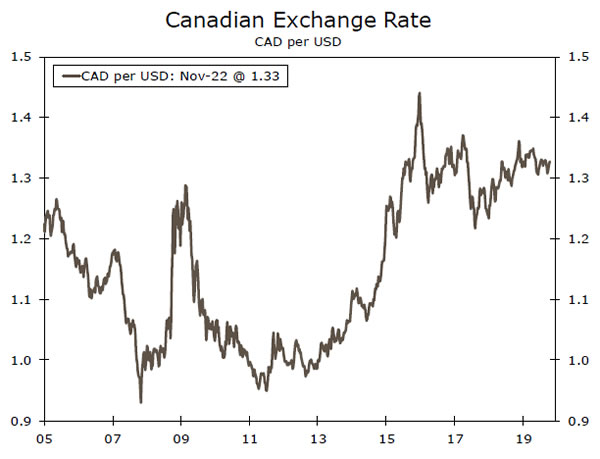

The value of the Canadian dollar has traded in a tight range vis-à-vis its American counterpart for most of the year (bottom chart). We look for the FOMC to cut rates one more time early in 2020, which should weigh somewhat on the U.S. dollar versus the Canadian dollar. In addition, we expect that the U.S. Congress will eventually ratify the USMCA trade agreement, which should remove some uncertainty regarding the Canadian economic outlook. Therefore, we forecast that the loonie will appreciate slightly against the greenback in coming quarters.

Credit Market Insights

Global Debt Hits New Record

Global debt increased by $7.5 trillion in the first half of 2019 to $250.9 trillion, according to the latest report from the Institute of International Finance (IIF)

The increase was driven by governments and the non-financial corporate sector, and a majority of the jump came from the two largest economies, the United States and China, which accounted for more than 60% of the increase. Meanwhile, emerging markets’ debt hit a new record of $71.4 trillion (equal to about 220% of GDP), with government debt growing quickly in countries like Argentina, Brazil and South Africa. As the IIF noted, countries with high government debt may find it harder to implement fiscal stimulus measures in the future. The IIF added that it sees no signs of a slowdown in debt accumulation, and looks for the total amount to exceed $255 trillion this year.

The mounting global debt is likely in part a result of central banks around the world, such as the European Central Bank, lowering interest rates to record lows, making borrowing conditions easier.

The IIF’s report suggests markets should be cautious of rising debt levels. The rise in global debt could present trouble ahead and central bankers appear to be taking note. While the conclusion of the Fed’s most recent financial stability report was that vulnerabilities to the U.S. financial system were little changed, it did highlight rising levels of corporate debt as a potential vulnerability.

Topic of the Week

Thankful for Low Food Inflation—or Convenience

Most readers will already have their Thanksgiving grocery-run done and may have noticed slightly higher totals at the register this year. According to the American Farm Bureau, Thanksgiving dinner for 10 this year increased by a penny to $48.91, breaking a three-year string in which the cost of a Thanksgiving meal declined.

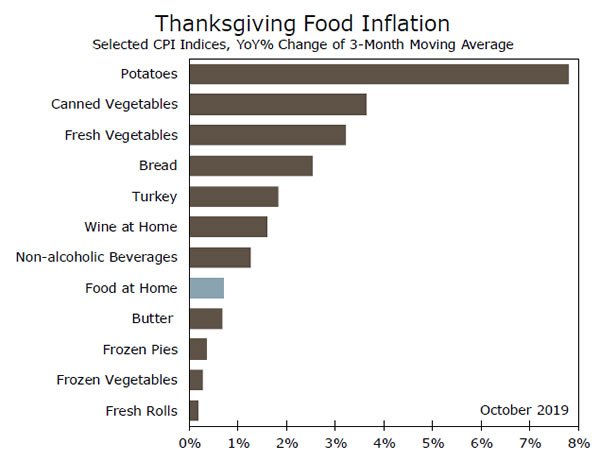

Based on data heading into November, however, we suspect shoppers may have noticed a heftier price jump, unless stores step up their discounting. Prices for common food items served at Thanksgiving were up across the board relative to last year according to the Consumer Price Index (top chart). Moreover, prices for many key Thanksgiving items—including turkey—have risen faster than grocery items have generally.

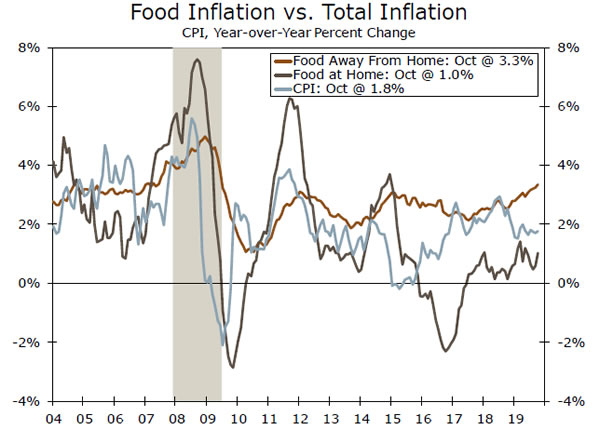

That said, overall price increases for food at home remain relatively tame. Costs at the grocery store continue to advance more slowly than overall inflation (bottom chart). As a result, the share of household spending devoted to food at home has fallen to 7%, which is half the share registered in the late 1970s.

Looking ahead, grocery store inflation looks likely to remain fairly benign for the consumer. The Commodity Research Bureau food index, which leads the CPI food at home index by about six months, is down slightly over the past year. Agriculture prices have been under pressure the past year from Chinese tariffs, but speculation of a “Phase I” deal that includes significant purchases from China have helped to support prices more recently.

Households heading out to celebrate Thanksgiving or ordering pre-prepared food will, however, notice more of a price bump. The cost of eating out has increased ahead of both grocery and overall inflation for most of the past seven years as households place more emphasis on convenience (bottom chart). The tight jobs market, especially for lower-skilled workers who often start their careers in food services, has further fueled costs for eating out, which are now rising at their fastest pace of the expansion.