- Economic indicators confirm a picture of moderate recovery.

- People’s Bank of China (PBoC) eases again and continues to focus on credit to the private sector.

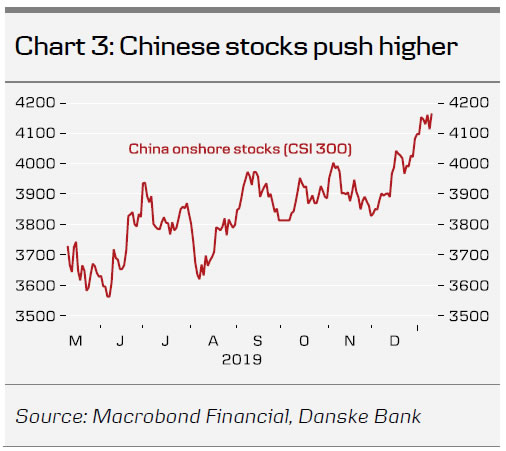

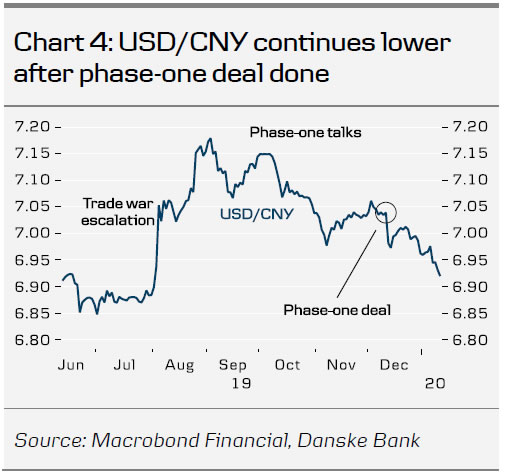

- CNY strengthens further and stock markets push higher.

- Increasing signs of a reform push in 2020 within areas of SOEs, private sector and Hukou system.

- Phase-one trade deal set to be signed on 15 January.

Following a seasonal break, China Weekly Letter is back. Today’s edition is a wrap-up of what happened over Christmas and New Year. Fortunately, news has been mainly positive. We have had confirmation that the phase-one trade deal will be signed next week, witnessed decent growth indicators and seen signs that the Chinese leadership may push for a faster reform pace in 2020 and continue the work on reducing financial risks and improving financing for the private sector. Both the CNY and stock markets have rallied in response to the newsflow.

Moderate recovery on track

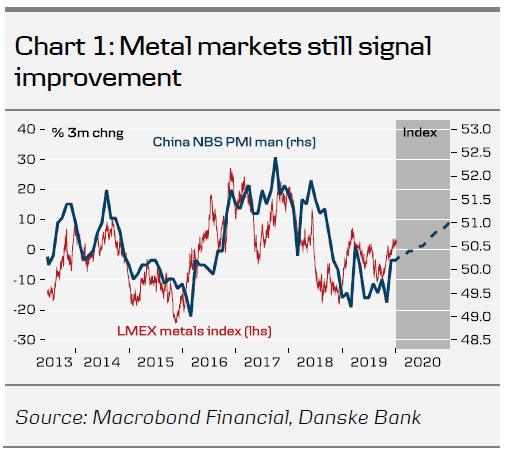

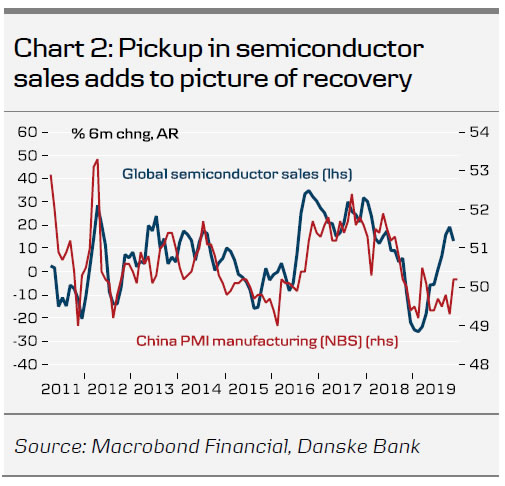

PMI data for December were slightly better than expected , suggesting that the worse is behind us. Other indicators paint a similar picture, such as China’s electricity production and industrial metal prices. Global semiconductor sales have also turned after a big dive in early 2019, suggesting that the electronics sector, which is important for China and many other Asian countries, has picked up again.

Comment: Some of the big headwinds in 2019 have started to ease . The all-out trade war has been avoided with a phase-one deal and economic stimulus has underpinned demand. There are signs that an inventory cycle played out following the fears of a global recession in 2019, which led companies to slash production to get rid of inventories. The pickup in semiconductor sales suggests inventory reduction has run its course. The outlook for electronics in 2020 is also favoured by more 5G mobile phones coming to market ( Apple launches its’ first 5G phone in September ) and the need for investments in 5G mobile infrastructure should gain traction. See China Outlook – Clouds are lifting , 19 December 2019, for more on our expectations for the Chinese economy.

PBoC easing to help small companies and private sector

PBoC eased further just before New Year by cutting the reserve requirement ratio by 50bp. According to the statement , it directs the policy easing at lowering financing costs for micro and small enterprises (MSEs) and private enterprises .

Following meetings before New Year, on 3 January, the China Banking and Insurance Regulatory Commission (CBIRC) released ‘Guidance Opinions Concerning Driving High-Quality Growth of the Banking and Insurance Sectors ‘. The document set the goals of a ‘more optimised financial structure’ and ‘the formation of a multi-tier, broad-coverage differentiated banking and insurance institutional system’ by 2025.

Comment: The policy easing by PBoC is another move to improve credit to the private sector and, not least, start-ups and small- and medium-sized companies, which generally struggle to get credit, not least following the crackdown on shadow finance over the past few years. The work by CBIRC to create a multi-pronged financing system is set to prioritise more financing channels for the private sector. At the same time, we expect focus to be on building a system with a proper balance between risks and financing availability. Allowing for more defaults is part of the transition to a system that more properly assesses risks and where companies in the state sector face tougher budget constraints.

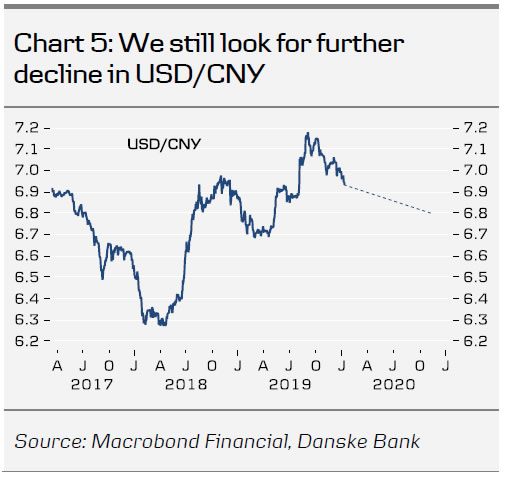

CNY and Chinese stocks see strong gains

The positive newsflow added a tailwind to the CNY and Chinese stock markets. USD/CNY has fallen to 6.92, the lowest level since early August and stocks have reached a new cycle high. On Friday, Blackstone’s Byron Wien said to Bloomberg that he believed in further gains in the Chinese market even without a phase-two deal.

Comment: We believe the positive trend can continue as the tide has turned for China and 2020 looks set to be a year of more positive momentum. We look for more inflows from foreign investors into the Chinese stock market, which would support both the stock market and the currency. We believe indications that China will step up the reform pace in 2020, which we turn to next, will support the positive sentiment.

Signs of reform push in 2020

Chinese leaders have signalled a further reform push in a range of areas lately. On 25 December, the State Council (China’s cabinet) signalled new initiatives to reform the so-called Hukou (registered residency status) system and rolled out guidelines to ‘adopt more steps to remove institutional barriers that block the social mobility of labour and talent’. The Hukou household registration system ties people to their original birthplace, where they have their ‘Hukou’. On reform of state-owned enterprises (SOEs), the state-assets watchdog SASAC vowed in late December to push ahead with an overhaul of state firms. We expect China to release a three-year plan on SOE reform in the first quarter. It may announce this at the annual National People’s Congress (NPC) starting on 5 March, where policy signals and goals for the year are set to be revealed.

Comment: In our view, the increasing signs of reform are important, as are steps to improve access to credit for the private sector. The rise in defaults among SOEs over the past year supports the notion that Beijing is stepping up reform, as it indicates that Beijing is forcing tougher budget constraints on inefficient SOEs. We intend to watch the NPC closely for indications of a possible step-up in reforms.

Other China news this week

Taiwan goes to the polls on Saturday, with incumbent Tsai Ing-wen favourite to stay on as President.

A US-China phase-one deal is set to be signed on 15 January, although Donald Trump has said it could be shortly after. A Chinese delegation is due to be in Washington from 13-15 January.

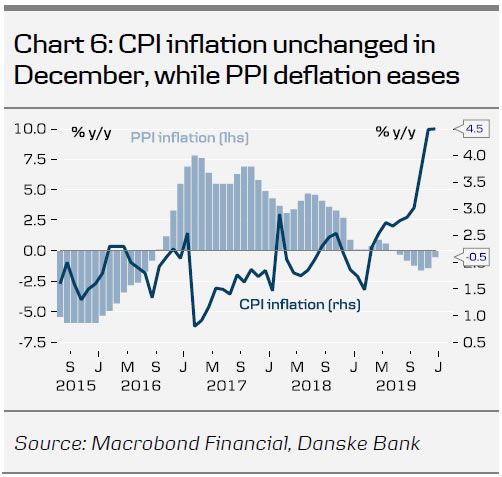

CPI inflation was unchanged at 4.5% in December (Chart 6). PPI deflation eased from -1.4% y/y to -0.5% y/y. We expect it to become positive again in coming months.

{kind=link}