U.S. Highlights

- Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S.. It is still early days, but it is likely the important efforts to contain the disease will crimp economic growth in China.

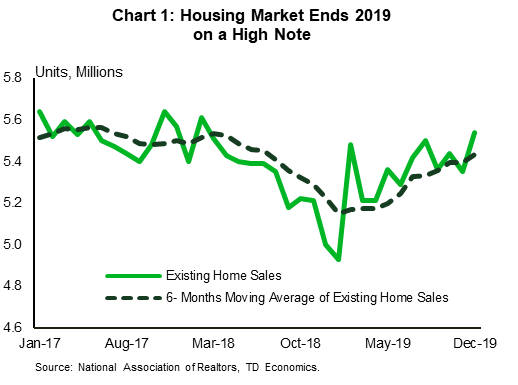

- Existing home sales more than recouped November’s decline in December. Unseasonably warm weather likely was a factor, but it sets up strong momentum in residential investment heading into 2020.

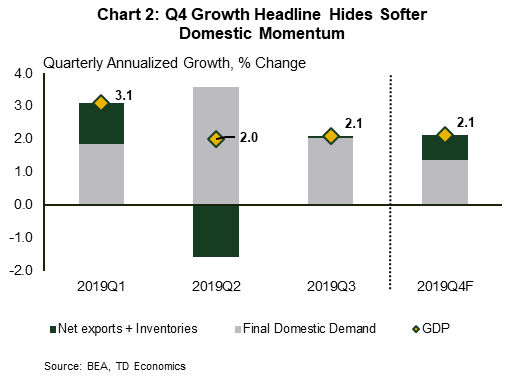

- Next week features the Fed meeting and our first peek at fourth quarter economic growth. The Fed is likely to leave rates on hold as it assesses the potential upside from the trade deal with China. A solid headline of around 2% growth is likely to mask softer domestic details.

Canadian Highlights

- The Bank of Canada’s interest rate decision was the main event of the week. As expected, the Bank held the rate at 1.75%. However, the accompanying statement was dovish compared to expectations.

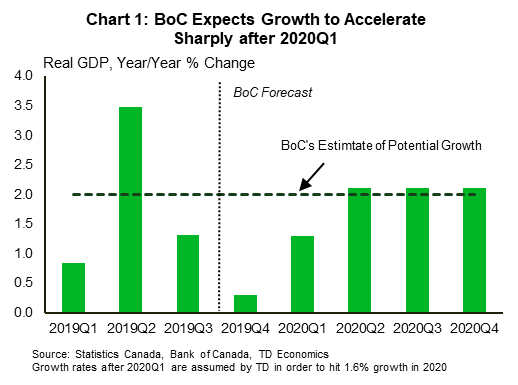

- Despite the dovish tone in the statement, the Bank’s growth expectations after the near-term look downright peppy. Growth is projected to accelerate through 2020 to an above-potential pace next year.

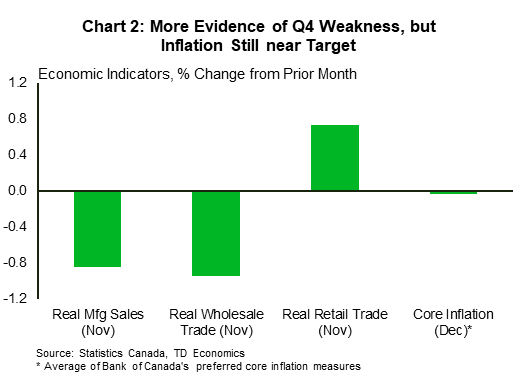

- Data this week generally reinforced our view that the economy stalled at the end of 2019. Even the decent retail sales data was driven by often volatile auto sales and was unable to reverse the prior months’ decline.

U.S. – All Quiet Ahead of the Fed

Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S. It is still very early days, with analysts looking back at the SARS outbreak in 2003 for guidance. However, the global health system is now much better prepared to contain an outbreak like this. The containment restrictions in China will hopefully help, but the disruption is likely to hold back economic growth there in the short-term.

The European Central Bank left its low policy rates unchanged this week. Activity in the Euro Area appears to be stabilizing, albeit at a lower level. Christine Lagarde, the new ECB President, also set out the framework for the ECB’s first strategic review in 16 years. It will reconsider the inflation target and the tools used to achieve it. Notably it will also examine how other considerations, like climate change and environmental sustainability can be relevant to the ECB’s mandate.

Existing home sales jumped up 4% in December, more than recovering from the 1.7% decline in November. Activity was likely boosted by unseasonable warm weather in December, so we will likely see some softness in the months ahead. Overall, however, the story of 2019 was a resurgence in housing in the second half of the year (Chart 1). The main reason was rising affordability due to lower mortgage rates and accelerating income.

In fact, home sales could have been even higher if not for constrained housing supply, which is driving up prices. All in, as we outlined in our recent report, we expect existing home sales to continue to improve, but at a more subdued pace this year.

Next week will feature bigger headlines, with a Fed meeting and fourth quarter GDP data. We don’t foresee fireworks from the FOMC, which is widely expected to leave rates unchanged. This decision does not feature a forecast update, but we will be watching for the Fed’s take on the Phase 1 China trade deal. The narrative of a strong consumer and resurgent housing sector, alongside weak business investment, remains very much intact since December’s statement.

Fourth quarter economic growth is forecast to post a respectable 2.1% annualized gain on the surface. However, the details are likely to show the U.S. economy ended 2019 on a soft note. Consumer spending is tracking below 2%, and business investment is looking flat to slightly negative. Residential investment is one area expected to be quite bright, but it is relatively small. A large drop in imports is the main factor keeping growth above 2%, but that is not a positive sign for demand (Chart 2). Trade is often a trickier component to predict, so there is a bit more uncertainty than usual on the quarter’s forecast. Domestic demand should look a bit better in Q1, but overall our latest forecast calls for relatively modest growth in 2020 of around 2 percent.

Canada – This Is What It Feels Like…When Doves Guide

In the past five days, economy watchers have been gobsmacked by a cornucopia of top-tier data and events, headlined by the Bank of Canada’s latest interest rate decision. As expected, the Bank held their policy rate steady at 1.75%, although the accompanying statement hewed to the dovish side of expectations. Policymakers rightly put some of the blame for the recent run of poor data on “special factors” (e.g. labour and other disruptions) but acknowledged that weak global conditions could be weighing on activity more than previously thought. They also downgraded their 2020 growth forecast a touch to 1.6% – on lesser contributions from consumption and inventories – while caveating recent positive trade developments with references to still-heightened uncertainty and rising geopolitical risks.

Still, the title of this article may be exaggerating things, as the Bank’s outlook is not completely bleak (Chart 1). In fact, after a lull to end 2019 (where “special factors” helped keep growth near zero) and a weak rebound expected in the first quarter of this year, prospects for the Canadian economy look downright peppy to Poloz and company. This is clear given that growth would have to average 2.1% (annualized) in the remaining quarters of 2020 to hit the Bank’s full-year target of 1.6%. What’s more, their estimate of potential output (i.e. how much we’re capable of producing) has been boosted compared to what was expected in October. Next year, policymakers expect the economy to “grow just above the rate of potential”, yielding an upgraded forecast of 2.0% for the year overall. What’s behind these relatively rosy projections? Much of it can be put down to household spending, although forecasts for residential investment and export growth also received lesser upgrades.

Back in the here and now, the run of primary and secondary data releases this weak reinforced our forecast that growth stalled out in the final quarter of 2019 (Chart 2). Manufacturing volumes tumbled 0.8% m/m in November, partly reflecting since-ended strikes at CN Rail and GM. However, moving past these impacts revealed weakening trends in several sectors and regions. Wholesale sales volumes also fell during the month, with declines across most major categories. Even consumer price inflation got in on the act, with the average of the Bank of Canada’s core measures dipping slightly, though generally remaining on-target, in December. On the plus side, growth in November retail sales volumes was solid, although this followed back-to-back drops in the months prior and gains were largely in the volatile auto sales sector. All told, it’s clear that fourth quarter growth was exceedingly weak despite the likelihood that the end of labour disruptions in November will make the December data look a bit better

Our 2019Q4 growth tracking is close to (though a bit below) the Bank’s updated forecast. However, the rest of our forecast is not quite as bullish. As such, we view their projections as leaving room for disappointment, particularly given historically high household debt service charges, a challenged global economy, and the chance that bond yields could rise further. Ultimately, these factors tilt the balance of risks in favour of a rate cut this year.

U.S: Upcoming Key Economic Releases

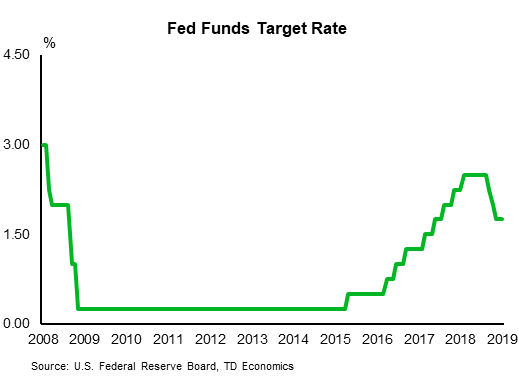

U.S. FOMC Rate Decision – January

Release Date: January 29

Previous: 1.50-1.75%

TD Forecast: 1.50-1.75%

Consensus: 1.50-1.75%

Fed officials will almost certainly keep the target range for the funds rate at 1.50-1.75%, a second consecutive meeting with no change following three straight 25bp easings. We expect changes to the FOMC statement to be fairly minor, resulting in a similar message to the one sent in December. Officials are undoubtedly relieved that trade tensions have eased and their base case is likely still for an extended pause, but they probably still see more downside than upside risks. Note that there are no new economic or dot plot projections this time. In contrast to the funds rate, we expect officials to announce a 5bp increase in the IOER rate to 1.60% in order to better align the effective funds rate with the mid-point of the target range. Fed officials will (rightly in our view) insist that the change is “technical,” as the effective rate has been running below the 1.625% target range midpoint. Moreover, as usual, the IOER rate will be relegated to the separately released monetary policy “implementation note,” and not the FOMC statement itself.

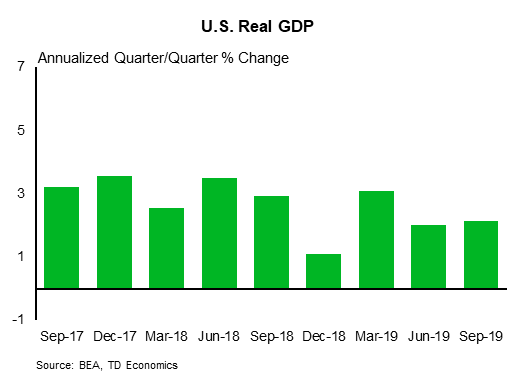

U.S. Real GDP Growth – Q4 Advance

Release Date: January 30

Previous: 2.1%

TD Forecast: 2.1%

Consensus: 2.2%

Real GDP likely rose at a seemingly solid 2.1% pace in Q4. However, beneath the headline, domestic demand was looking a little soft to end the year. We expect to see a solid gain in residential investment, but a decline in business fixed investment and some slowing in consumption, which has shown resilience thus far. We expect headline GDP will be boosted by a tariff-related plunge in imports. This looks to be only be partially offset by a drawdown in inventories. Core inflation likely remained tame. For 2019 as a whole, we estimate real GDP rose by 2.3% (calendar-average basis), down from 2.9% pace in all of 2018.

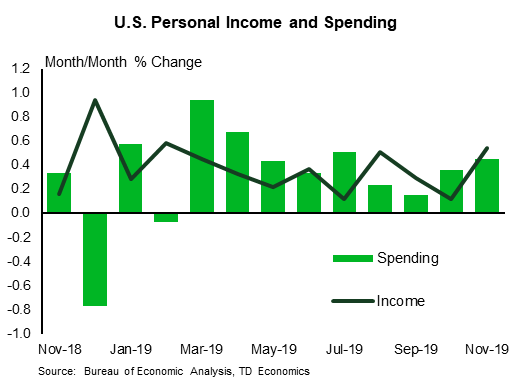

U.S. Personal Income and Spending – December

Release Date: January 31, 2020

Previous: Spending: 0.4% m/m; Income: 0.5%

TD Forecast: Spending: 0.3% m/m; Income: 0.3%

Consensus: Spending: 0.3% m/m; Income: 0.3%

Income and spending likely rose moderately in nominal terms in December. Our 0.3% m/m forecasts imply zero growth in real terms, as we estimate the PCE price index rose 0.3%, led by higher gasoline prices. We estimate real consumer spending rose at a 1.6% quarter-over-quarter annual rate in Q4 as a whole, down from a 3.1% pace in Q3; the quarterly total will be in the GDP report. We estimate the core PCE price index rose 0.2% m/m in December, keeping the 12-month change low at 1.6%. The 12-month change in the overall PCE price index probably rose to a still-low 1.7% from 1.5%.

Canada: Upcoming Key Economic Releases

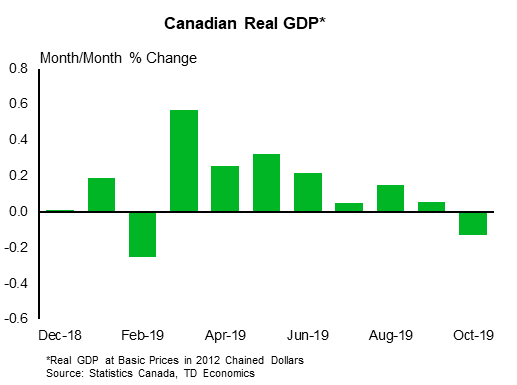

Canadian Real GDP – November

Release Date: January 31

Previous: -0.1%

TD Forecast: 0.0%

Consensus: N/A

TD looks for a flat print on industry-level GDP for November with a muted performance across goods and services. Real manufacturing shipments contracted by nearly 1pp during the month, despite the tailwind from a return to normal operations at Canadian auto plants after US labour disputes disrupted supply chains in October. Energy is expected to be a headwind to growth, owing to softer preliminary output in the oil sands, while construction spending for November was subdued, potentially in response to unseasonably cool weather during the month. Looking to services, another strong month for existing home sales will help support real estate while retail sales should provide another source of strength. However, this will be offset by a drag from wholesale trade and transportation, with the latter a key source of downside risk due to the impact from the CN strike. A flat print would leave Q4 growth tracking near BoC projections (0.3%), suggesting more excess capacity and disinflationary pressure going forward.

{kind=link}