U.S. Review

Something in the Air

- Fears of an escalating coronavirus outbreak reached the United States this week, as a Washington state man became the first confirmed domestic case and the international total reached more than 800.

- We expect any short-term economic impact to be limited and concentrated in East Asia, but the U.S. economy is certainly more vulnerable to shocks at this stage in the cycle. Sentiment matters.

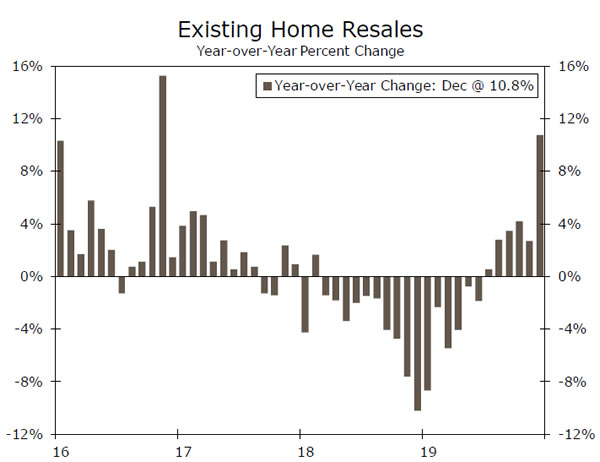

- On the home front, December existing home sales rose a solid 3.6% to a 5.54 million-unit pace as the housing market renaissance continues.

Something in the Air

Fears of an escalating coronavirus outbreak reached the United States this week, as a Washington state man became the first confirmed domestic case and the international total reached over 800. We expect any short-term economic impact to be limited and concentrated in East Asia—see our initial report and page 4 of this report for more detail. The 2003 SARS outbreak is perhaps the most relevant comparison, but the coronavirus is reportedly not as deadly and containment methods today are ostensibly more effective. On the other hand, a simple historical comparison misses the fact that retail spending, travel and personal consumption are a much more important driver of the Chinese economy today, 16 years later, a potential downside risk to estimates of a virusinduced economic deceleration.

The focus this week on epidemiology rather than economics is not unwarranted. The heightened financial market attention to medical reports out of central China did indeed have a lot to do with the scarcity of new economic data, but it is also true that the U.S. economy is more vulnerable to shocks in the 11th year of the expansion. Seemingly far-off events—an Asian virus outbreak or the killing of an Iranian general—can spark a rapid deterioration in sentiment, which can quickly affect spending habits and the real economy. Thus, while a cold look at the numbers suggests no reason to panic—the single U.S. case of coronavirus is dwarfed by the 6,600 deaths from the flu already this season, according to the CDC—it is fear that can have an outsized impact on the economy, particularly at this stage of the cycle.

The World Economic Forum in Davos also got its usual dose of media attention, but passed without major fanfare as the assembled politicians and business executives expressed confidence in the global economy. The IMF was slightly less optimistic, reducing its global growth forecasts for 2019 and 2020 by 0.1 percentage point to 2.9% and 3.3%, respectively. It similarly downgraded its U.S. forecasts to 2.3% and 2.0%, still the highest among the G7. On the sidelines, President Trump turned his attention from China to the EU, again threatening tariffs if a deal isn’t reached before the election. EU officials promised to retaliate.

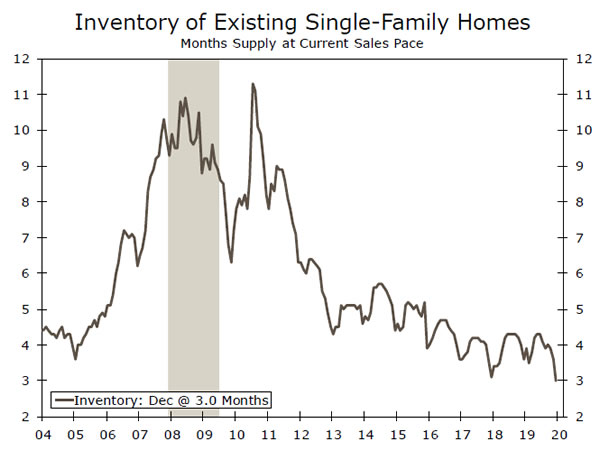

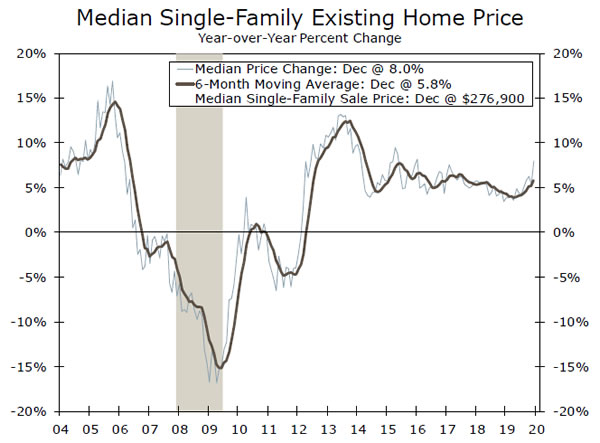

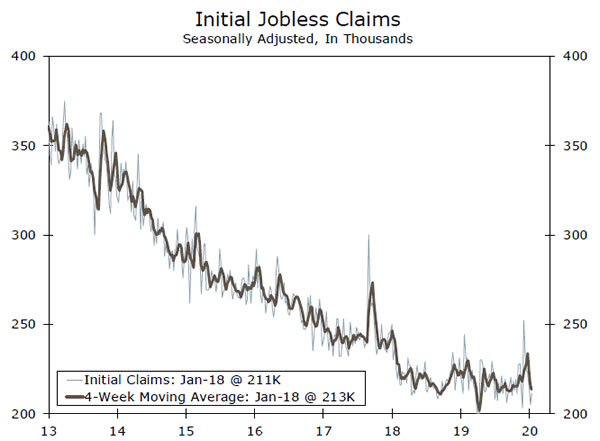

On the home front, December existing home sales rose a solid 3.6% to a 5.54 million-unit pace as the housing market renaissance continues. Lower mortgage rates have brought buyers back into the market, particularly in the South and West, where population and employment growth remain the strongest. The rebound in existing home sales follows a string of positive housing reports and will have sizable pass-through effects, including realtors’ commissions and remodeling spending. Inventories are extremely low, however, which is driving price appreciation higher again— the median single-family home price rose 8.0% year-over-year in December—which is spurring more construction. Housing starts reached a 13-year high in December and builder optimism is holding near 20-year highs. With this backdrop and no discernible uptick in jobless claims, the housing market is clear for further gains.

U.S. Outlook

Durable Goods • Tuesday

Month-to-month changes in durable goods orders are notoriously volatile, and the past few months have been no exception. Ongoing struggles at Boeing with its 737 MAX aircraft—more on that in Topic of the Week on page 7—as well as the recent GM strike have resulted in some large swings in underlying order components.

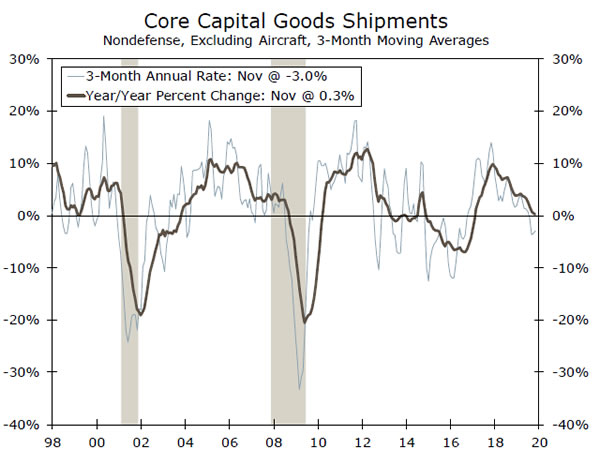

That said, Tuesday’s December durable goods report should be rather boring. Attention will be on nondefense capital goods shipments since they feed into the Bureau of Economic Analysis’ (BEA) calculation of equipment spending in the GDP report. This will be a good indication of what to expect from this component for Q4 output, which will be released two days later. After declining at a 3.4% annualized pace in Q3—the weakest since 2015—we expect equipment spending remained flat to end the year. Elsewhere, our focus will be on any sign of stabilization in the sector after manufacturing took a hit last year amid trade uncertainty.

Previous: -2.1% Wells Fargo: 0.9% Consensus: 1.0% (Month-over-Month)

Q4 U.S. GDP • Thursday

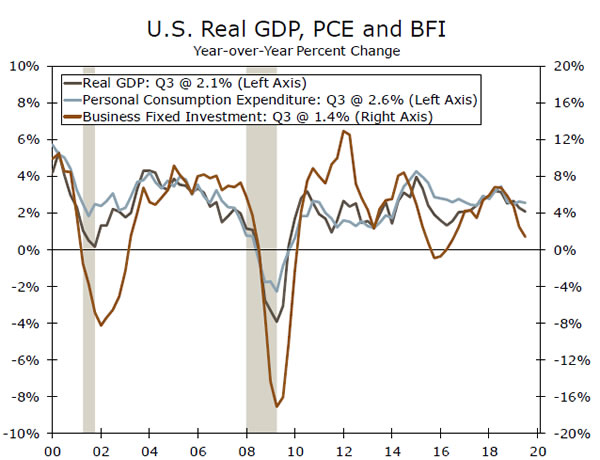

To many, Q4 may already seem like a distant memory, but on Thursday market attention will turn to the BEA’s Q4 GDP release. We expect the economy expanded at a 2.3% annualized pace in the final quarter of the year. This gain is largely predicated on a sizeable boost from net exports, as the November international trade report showed a larger narrowing in the trade deficit for the month than previously anticipated.

Outside of trade, keep an eye on the residential construction line. Residential investment seems to be a bright spot in the outlook; demand is on the rise as lower mortgage rates entice prospective buyers to enter the market. Consumer spending shouldn’t be much of a surprise. We’re expecting a 2.2% gain, which is still strong but a step down from the prior two quarters. Business investment spending is expected to remain weak in Q4—as addressed in the durable goods section—but should climb out of its slump in 2020.

Previous: 2.1% Wells Fargo: 2.3% Consensus: 2.2% (Annualized, Quarter-over-Quarter)

Personal Income & Spending • Friday

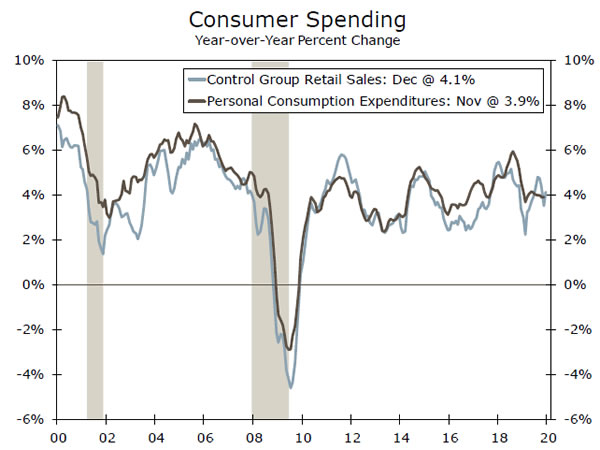

By the time the BEA releases its December personal income and spending report on Friday, we will already have Q4 personal consumption expenditure (PCE) data. Nonetheless, the report is still likely to garner much attention. The last month of the quarter can be particularly important in gauging consumer spending momentum for the next quarter, meaning a solid gain in December would set Q1 consumption off to a good start. Our expectation of a 0.4% gain in spending should do just that. We already know December was a strong month for retail sales, which rose a solid 0.3%, as “control group” sales—which exclude volatile purchases like gasoline, autos, food services and building materials—were up 0.5%. The “control group” is a good proxy for personal spending on goods in the GDP accounts, and suggests our expectation for a 2.2% annualized gain in Q4 PCE remains reasonable. Further out, we expect a trend-like 2% quarterly pace of PCE growth.

Previous: 0.5%; 0.4% Wells Fargo: 0.3%; 0.4% Consensus: 0.3%; 0.3% (Month-over-Month)

Global Review

China’s Coronavirus Spreading to Financial Markets

- For the last three weeks, a new coronavirus has originated in China and spread across Asia. Most recently, the virus was confirmed to have entered the United States, sparking reminders of the SARS epidemic that plagued China and Asia in the early 2000s.

- These fears have reached financial markets, with Asian and Chinese asset prices coming under pressure over the last few weeks. With travel restrictions put in place and the Chinese New Year approaching, Chinese economic activity data could be affected; however, we would expect any disruptions to be short-lived.

China Coronavirus Scaring Markets, but for How Long?

Over the past few weeks, a new coronavirus—originating from the city of Wuhan, China—has spread across Asia and into the United States. To date, there have been more than 800 confirmed cases around the world, while the virus has claimed at least 25 lives. The virus is still in its early stages, but has already drawn comparisons to the outbreak of SARS (severe accurate respiratory syndrome) that plagued China and other parts of Asia in the early 2000s. As of now, doctors and scientists have indicated the Wuhan coronavirus is not as severe as SARS; however, this has not prevented Chinese authorities from taking preemptive action in an effort to stem the virus’ effect and prevent it from spreading globally. In just the last week, the Chinese government has implemented travel restrictions in and out of the city of Wuhan, while other municipalities have placed constraints around the use of public transportation. In addition, the World Health Organization (WHO) has determined the virus is not yet a global public health emergency—a designation used for complex epidemics that can easily spread internationally—but noted “it may yet become one.”

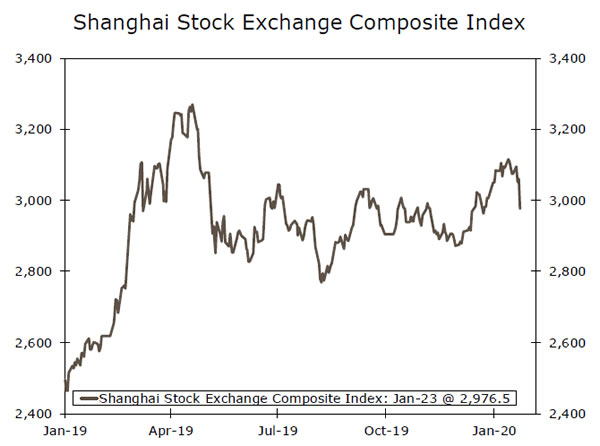

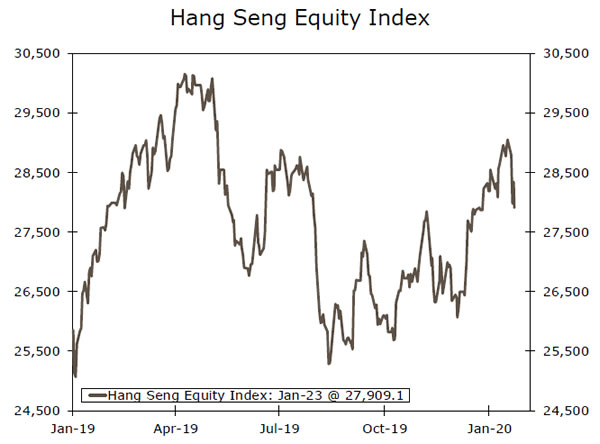

In addition to its effect on the global population, the coronavirus has also rattled investors and financial markets, particularly in China and financial hubs across Asia. Since the beginning of this week, the Shanghai Composite equity index has sold off about 4.0%, while the Hong Kong Hang Seng equity index is down close to 3.5%. The Chinese renminbi has also moved lower as a result, selling off roughly 1.0% over the same time period, while other emerging Asian currencies have also weakened as investor sentiment toward the region has soured. We would expect asset prices within emerging Asia to remain under some pressure in the short term as the severity and the ability to contain the virus are still unclear at this time. There may also be some effect on China’s economy as this week marks the beginning of the Chinese New Year, typically a time for increased travel and retail spending within the country. Given the travel restrictions and general fear of contagion, we would expect economic activity to decelerate in the short term, but not necessarily to a degree that we would be overly concerned with.

Looking further ahead, and despite details of the virus being scarce, we do not expect a major long-term effect on financial markets or the global economy. We think the risk-off tone toward Asian asset prices the last few weeks is likely to dissipate, while the likelihood of the recent negative sentiment affecting U.S. and other developed financial markets is quite low. As far as longer-term economic effects, we believe the coronavirus outbreak will not have any meaningful or long-lasting effect on China’s economy or any major influence over the economic health of other Asian countries. In fact, a report from the Brookings Institute estimating the economic effect of SARS determined annual GDP in China was reduced roughly 1% in 2003, but the economy recovered quite quickly. At this time, we do not expect a similar effect from the new coronavirus, and as mentioned, believe economic effects will be short-term in nature.

Global Outlook

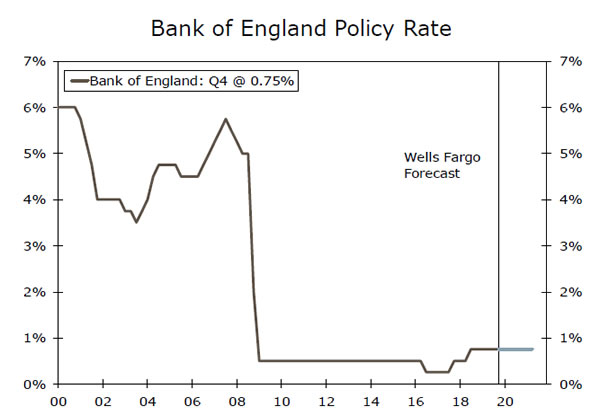

Bank of England • Thursday

Following a string of weak economic and sentiment data over the last few months, market participants have started to consider the possibility the Bank of England (BoE) could ease monetary policy. Last week, December retail sales significantly underperformed expectations, while monthly GDP data released in mid-January indicated the economy contracted in November. Tack on uncertainties regarding the future trade relationship between the U.K. and E.U., and the case for interest rate cuts becomes a bit more compelling. However, recent jobs and wage growth data indicate a relatively healthy labor market, and in our view, should result in the Bank of England holding policy rates steady next week. Formal approval of Boris Johnson’s withdrawal agreement should also keep the BoE on hold. As of now, markets are implying about a 45% chance of a BoE rate cut next week, which—should the BoE hold rates firm—could result in some upside for the British currency.

Previous: 0.75% Wells Fargo: 0.75% Consensus: 0.75%

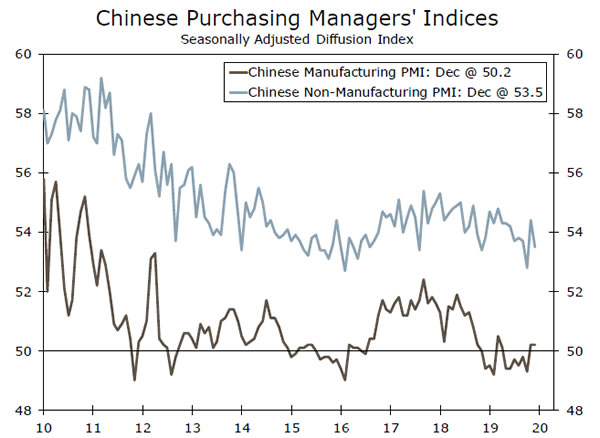

China Manufacturing PMI • Thursday

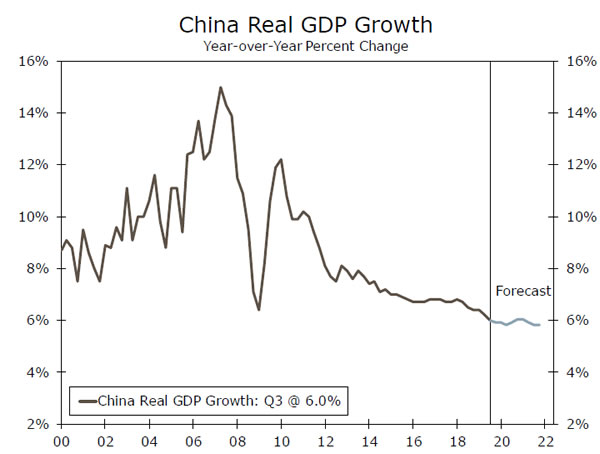

The phase I trade deal with the U.S.—secured in mid-December and officially signed earlier this month—likely takes some pressure off the Chinese economy going forward. A slight rollback of existing tariffs should also help the manufacturing sector pick up in the coming months. As of now, consensus forecasts suggest the manufacturing PMI may dip slightly in January to 50.1, but remain in expansionary territory. In our view, we would not be overly surprised if this data point beat consensus forecasts given some of the renewed optimism around China’s economy following the phase I trade deal. In addition, recent GDP data matched consensus expectations, with the economy growing 6.0% year-over-year in Q4-2019, a welcome sign given how trade tensions have affected the economy over the last year or so. We do not expect a major effect on China’s economic data as a result of the new coronavirus, with any effect on soft data likely to be short-lived.

Previous: 50.2 Consensus: 50.0

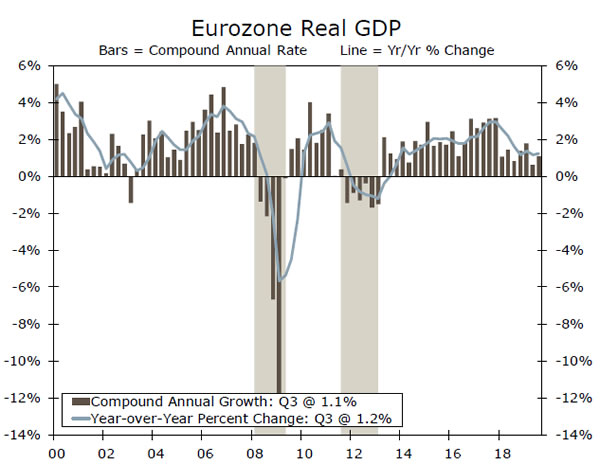

Eurozone GDP • Friday

In recent months, Eurozone economic data have shown notable improvements. In particular, the service sector has been quite resilient with retail sales growth firming. While the manufacturing sector remains relatively subdued, an improving service sector could underpin a more optimistic growth profile for the Eurozone. In addition to a stronger service sector, inflation has picked up recently, with core CPI inflation quickening to 1.3% year-over-year, while market-based expectations for inflation have also moved higher. Consensus forecasts expect growth to remain constant in Q4 at 0.2% quarter-over-quarter. In addition, we currently forecast the Eurozone economy to expand a little more than 1.0% this year, with risks around that forecast tilted toward the upside. Given an improved economic outlook and a relatively steady euro, we expect the European Central Bank will keep policy rates on hold for the time being; however, it will continue its bond-buying program to provide additional stimulus to the Eurozone economy.

Previous: 0.2% Consensus: 0.2% (Quarter-over-Quarter)

Point of View

Interest Rate Watch

Foreign Central Banks on Hold

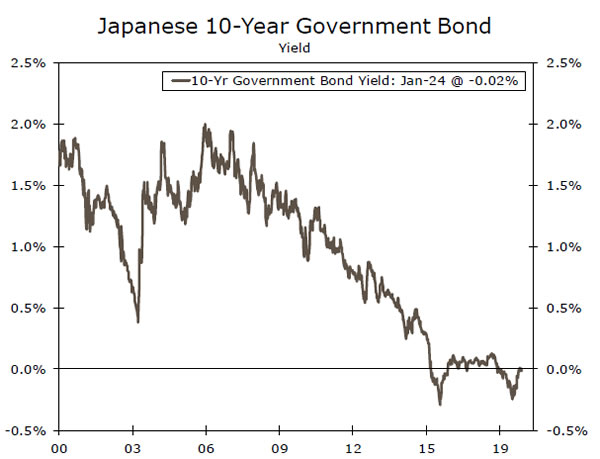

A number of major central banks held policy meetings this week and, as largely expected, each decided to keep its policy stance unchanged. On Tuesday, the Bank of Japan (BoJ) left its main policy rate unchanged at -0.10%, where it has been maintained since January 2016. In addition, the BoJ kept in place its “yield curve control,” whereby it aims to keep the yield on the 10-year Japanese government bond “around zero percent” (top chart). We do not envision the BoJ making any material changes to its policy stance in the foreseeable future.

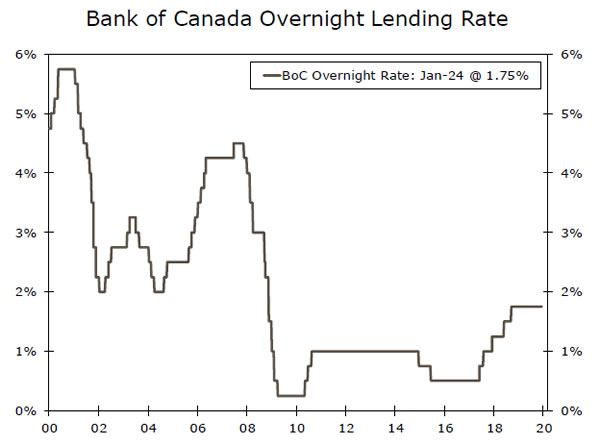

A day later the Bank of Canada (BoC) left its main policy rate unchanged at 1.75%, where it has been maintained since October 2018 (middle chart). However, the statement that was released at the conclusion of the meeting had a dovish tone. Notably, the BoC said that it will be “watching closely to see if the recent slowdown in growth is more persistent than forecast.” In that regard, the BoC forecasts that real GDP in Canada will grow 1.6% in 2020 and 2.0% next year. We look for the BoC to keep its main policy rate unchanged at 1.75% through at least the end of this year. However, we acknowledge that the probability of a BoC rate cut is higher than the probability of a rate hike over that timeframe.

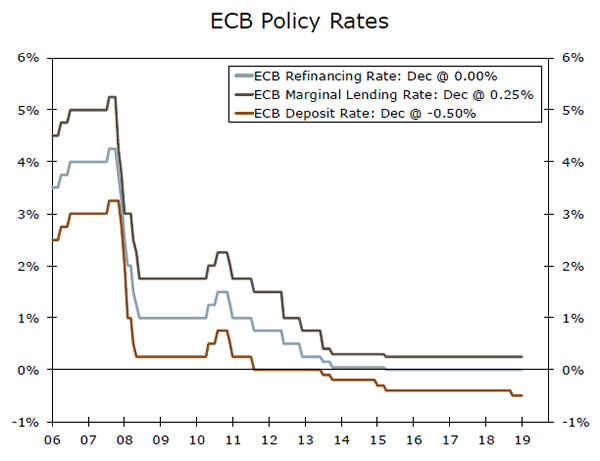

On Thursday, the European Central Bank left its three main policy rates unchanged (bottom chart). We had been forecasting that the Governing Council would reduce its deposit rate from -0.50% to -0.60% at its policy meeting on March 12. However, as we describe in a recent report, we no longer look for an ECB rate cut. Specifically, it appears that growth in the Eurozone is stabilizing, albeit at a low level, following the deceleration that over the past two years. In addition, core CPI inflation rate has ticked up in recent months, but at only 1.3% it remains well below the ECB’s target of “below, but close to two percent.” Therefore, we would characterize the balance of risks to our new ECB forecast of no further rate cuts as skewed toward further easing. That is, if growth stumbles and/or inflation moves lower again, the possibility of an ECB rate cut later this year remains.

Credit Market Insights

C&I Loans Slowing to a Crawl

After registering a double-digit pace at the start of the 2019, commercial and industrial (C&I) loan growth fell to 2.2% on a year-ago basis in December, the slowest pace since February 2018. C&I lending, which funds firms’ operations and investments, has tracked a slowdown in business spending, as firms have showed little appetite for investment. The Senior Loan Officer Opinion Survey has shown more banks reporting weaker C&I loan demand for the last five quarters. Some of this has been led by a pullback in the energy sector, where a lack of new oil wells has contributed to outright declines in structures investment over the last two quarters. The rig count has stabilized to start the year, and our forecast calls for a modest improvement in structures investment going forward. There is still not a great deal of optimism surrounding investment in the energy sector, however, suggesting a big bounce back is unlikely. In the Dallas Fed’s latest energy survey, two-thirds of executives surveyed expected their capital spending to decrease or remain about the same in 2020.

Outside of the energy sector, lingering uncertainty from the trade war and weaker earnings will likely keep a cap on investment and lending growth. Our forecast for a modest improvement in investment in coming quarters could drive loan demand. However, a rebound would be limited by banks, which have reported tightening lending standards, despite delinquency rates near record lows.

Topic of the Week

Delayed Expectations

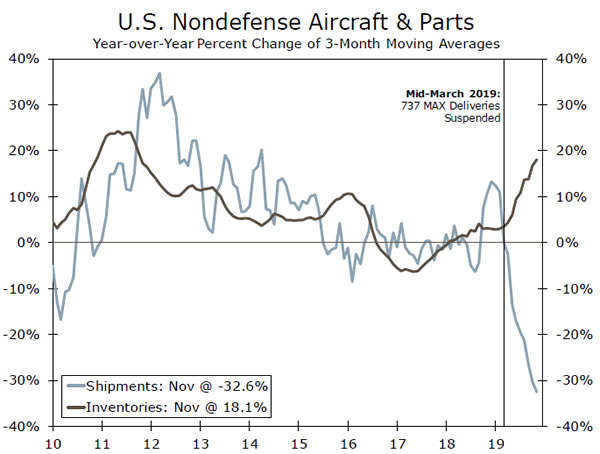

Boeing now does not expect its 737 MAX aircraft to return to service until mid-2020, due to the certification process taking longer than expected. This is months after the manufacturer previously anticipated, a delay which could have knock-on effects across the economy.

To date, there has been little evidence of pass-through effects from the grounding since Boeing continued to produce 42 MAX aircraft a month, down only slightly from its previous rate of 52 a month. The grounding resulted in more of an accounting disturbance in the GDP accounts, with a decline in equipment spending and exports (aircraft are counted once shipped) largely offset by a build in inventories. But the delayed timeline presents a new source of concern. A halt in production directly affects Boeings’ suppliers, and since production of the aircraft was only halted at the start of the year, the effect to suppliers is yet to be realized.

Boeing has released little detail regarding when it expects to resume production, so our baseline expectation has been that it will occur alongside a restart in shipments once the plane is given the all-clear to fly again. The exact timeline, of course, remains largely uncertain—perhaps making it even more difficult for suppliers to weather the storm. Suppliers may be forced to pare back hiring or even lay off workers, depending on how much they rely on Boeing and their position in the 737 MAX supply chain.

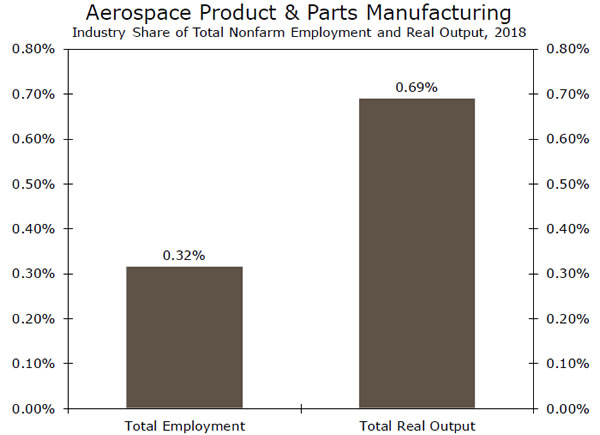

Spirit AeroSystems, supplier of Boeing, has already said it would lay off 2,800 employees, as more than 50% of its annual revenue comes from building components specifically for the 737 MAX. Aerospace production & parts related employment directly represents only 0.3% of U.S. employment. If you expand that to include other types of suppliers that amount surely would be higher; however, layoffs in the sector would still likely not be large enough to have a broad effect on the U.S. labor market. Furthermore, Boeing should eventually resume production and shipments of its MAX aircraft, meaning if layoffs are to occur, the unemployment would be temporary.

{kind=link}