Executive Summary

- For the past three weeks, a new coronavirus has originated in China and spread across Asia. More recently, the virus was confirmed to have entered several other countries around the world, sparking reminders of the SARS epidemic that plagued China and Asia in the early 2000s.

- These fears have reached financial markets, with Asian and Chinese asset prices coming under pressure over the past few weeks. With travel restrictions surrounding the Lunar New Year, China’s economic activity data could also be affected.

- Developments are extremely fluid and uncertainties around the severity of the virus remain prevalent. Accordingly, we think it’s important to lay out our base case scenario, as well as favorable and adverse scenarios, and potential implications for the Chinese economy and currency markets.

- As of now, we place a high probability on our base case scenario and expect China’s economy to grow at 5.8% this year, down from 5.9% before the coronavirus outbreak.

What is the Coronavirus and What is the Impact?

Over the past few weeks, a new coronavirus—originating from the city of Wuhan, China—has spread across Asia and into the United States and other countries. To date, there have been more than 6,000 confirmed cases around the world, while the virus has claimed at least 130 lives. The virus is still in its early stages, but has already drawn comparisons to the outbreak of SARS (severe accurate respiratory syndrome) that plagued China and other parts of Asia in the early 2000s. As of now, doctors and scientists have indicated the Wuhan coronavirus is not as severe as SARS; however, this has not prevented Chinese authorities from taking preemptive action in an effort to stem the virus’ effect and prevent it from spreading globally. In just the last week, the Chinese government has implemented travel restrictions in and out of the city of Wuhan, while other municipalities have placed constraints around the use of public transportation. In addition, the World Health Organization (WHO) has determined the virus is not yet a global public health emergency—a designation used for complex epidemics that can easily spread internationally—but noted “it may yet become one.”

In addition to its health effects, the coronavirus has rattled investors and financial markets, particularly in China and financial hubs across Asia. Since its peak, the Shanghai Composite equity index has sold off about 4.7%, while the Hong Kong Hang Seng equity index is down over 6.0%. The onshore Chinese renminbi has also moved lower as a result, selling off roughly 1.2% over the same time period, while the offshore renminbi has weakened about 1.4%. Other emerging Asian currencies have also weakened as investor sentiment toward the region has soured, with the currencies of countries closely linked to China under the most pressure. The impact has also spread outside of local Asian markets, with most emerging currencies selling off sharply. Oil prices and most commodity prices have come down significantly, dragging commodity-linked currencies such as the Russian ruble, Chilean peso and South African rand lower as well.

As far as effects on the Chinese economy, it is too early to make any specific determinations at this time. However, it is currently the Lunar New Year in China, which is typically a time for increased travel and retail sales. Given the travel restrictions in and out of China and general fear of contagion, there is likely to be a slowdown in economic activity to start the year, which would likely have an effect on the overall growth prospects. While the SARS epidemic may not be a perfect comparison, a Brookings Institution analysis estimated the economic impact of the SARS virus as reducing annual GDP in China by about 1.0% around 2002-2003. With this in mind, we lay out a few scenarios for how the coronavirus situation could evolve and highlight the possible impacts on the Chinese economy as well as potential currency moves.

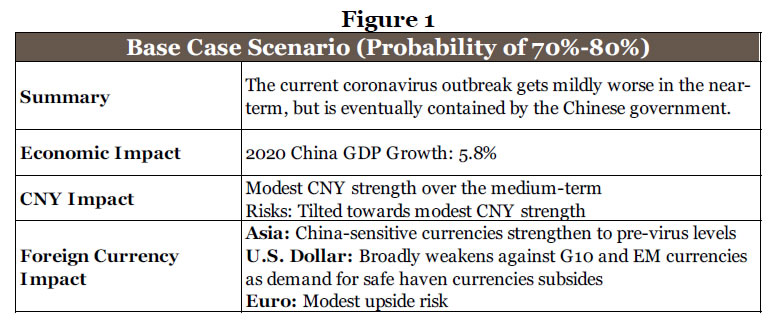

Base Case Scenario – Coronavirus Contained

Our base case scenario, which we assign a 70-80% probability, is that the current coronavirus outbreak gets mildly worse in the near-term, but measures taken by the Chinese government contain the virus. We anticipate that the Chinese government will continue to tighten restrictions on tourists in and out of China and continue to take preemptive measures such as entry screenings at major airports and school closures. With the outbreak occurring during the Chinese Lunar New Year—a peak time for travel and consumer spending—we expect the virus to have a slight impact on China’s growth prospects. Before the virus, we forecasted China’s economy to grow at 5.9% this year; however, given the expected slowdown in economic activity, we now expect China to slow to annual growth of 5.8%. As far as the Chinese currency, we believe the renminbi will eventually strengthen and are comfortable with an outlook for modest CNY strength over the medium-term. We also believe emerging Asian currencies will begin to strengthen as well, while the U.S. dollar will gradually weaken as demand for the safe haven qualities of the greenback dissipate. In addition, we would expect the euro to modestly strengthen from current levels.

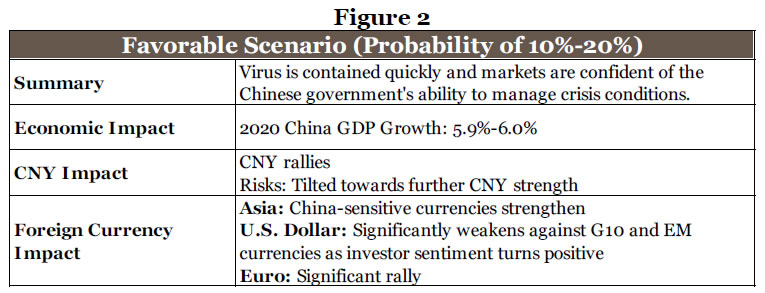

Favorable Scenario – Crisis Conditions Managed

Despite our base case assumption, there is the possibility that the Chinese government takes more aggressive and preemptive measures to contain the virus more effectively and quicker than expected. In this event, we would expect investor sentiment to turn positive as the Chinese government proves its ability to manage crisis conditions and limit the impact of the virus on financial markets and the Chinese economy. In this favorable scenario, we would expect the impact on the Chinese economy to be relatively limited and could even see growth prospects improve to 6.0% for full-year 2020. As fear of the coronavirus fades, we would expect the renminbi to firm back to pre-virus levels and potentially stronger, while we are optimistic on the currency’s medium-term prospects. In addition, emerging Asian currencies would likely strengthen, while we would expect the U.S. dollar to significantly weaken against both G10 and emerging currencies as risk-on sentiment spreads across currency markets, benefitting the euro as well.

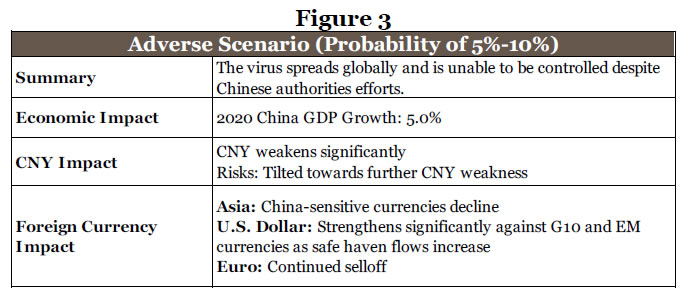

Adverse Scenario – Virus Spreads Globally

The likelihood of an extreme adverse scenario also exists. We define this scenario as the coronavirus spreading aggressively and globally, with the virus unable to be contained. In this scenario, fear spreads globally, negatively impacting investor sentiment and global growth prospects. Stricter travel restrictions are likely implemented with domestic Chinese activity slowing sharply. In this scenario we forecast the Chinese economy could slow significantly, falling to annual 2020 growth of 5.0%. This growth effect is similar to the impact SARS had on the Chinese economy. Developments surrounding a global spread of the coronavirus would likely have a major influence over currency markets and we anticipate the Chinese renminbi to exhibit uncommon volatility, while China-sensitive currencies are likely to selloff. As far as the path of the U.S. dollar, we would expect the greenback to strengthen significantly against G10 and emerging currencies, while the euro would likely decline.

Key Takeaways

As of now, we place a 70%-80% probability that our base case scenario materializes. Given how fluid the current situation is, we will be monitoring coronavirus developments very closely and will keep readers abreast of any updates to our scenarios, and if our base case changes meaningfully. However, given some degree of confidence in the base case, we remain comfortable with our assumption that the Chinese economy will grow slightly slower in 2020 than previously anticipated.

{kind=link}