The Canadian Dollar was where the action was at on the currency space overnight, when the Bank of Canada (BoC) threw another pleasant surprise to market with a hawkish hike.

Fears of a dovish hike when higher growth inflation expectations were expected, prompting traders to anticipate the next hike. At 0.75%, it was their first rise since September 2010 and followed on from its longest and least eventful easing cycle in history (2 cuts in 7 years).

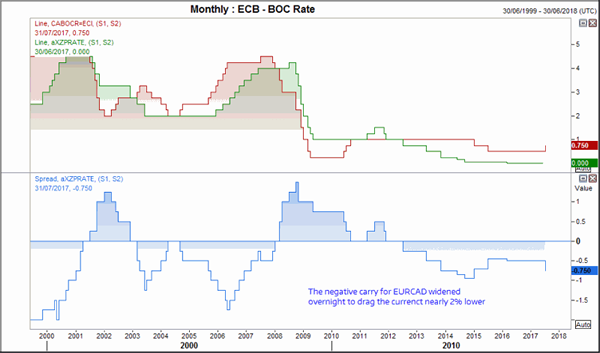

The Canadian Dollar jumped higher across the board but most surprisingly, enjoyed its best run against the mighty Euro. Plummeting -1.8% by the close, EURCAD experienced its most bearish session since Jan 2018. Technicals could partly explain the bearish move as many Euro crosses had stalled at technical resistance levels, making profit taking tempting for short-term traders. Yet with ECB’s deposit rate remaining at -0.4%, the negative carry for Euro has now widened to -75 basis points.

We’ll admit to the moves on EURCAD catching us a little off guard. Whilst losses following the meeting were not rules out, it was the magnitude of them which came as the surprise. The clear and decisive break of 1.4650 took it from the top of the channel and almost to its lower boundary, where is found support around the 61.8% retracement and the close prior to the French election gap higher. Due to the bearish momentum of the preceding move, we prefer to fade into rallies below 1.4650 for near-term short trades. If data continuous to support CAD and / or if Euro data cools a little, this may help it move below 1.440. For now, 1.440 is the near-term target but we are not yet ready to write of EURCAD just yet as we think ECB are yet to catch up with the curve and begin tightening.

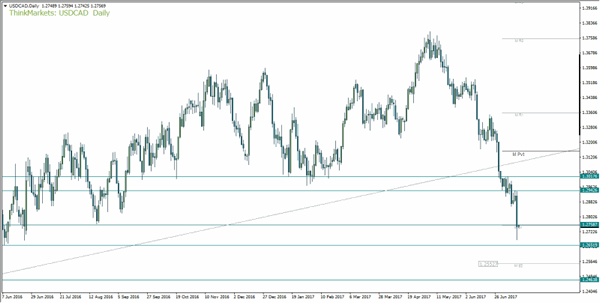

The -1.3% close was its worst since March ’16, yet the intraday low found itself down by 1.8% at one point. With no meaningful signs of bullish divergences forming on H4 or H1, further downside is the more likely route from here. With US CPI data out tonight, this too serves as a potential weak spot for the Greenback and cold simply send USDCAD lower towards 1.6520 support. Of course, at some point we are to see a correction of some sort, but price action from the 2017 is clearly impulsive, which means we are to see it break below 1.2464 low and continue its decline. So perhaps a correction may take place at or above this key swing low, with the monthly S2 at 1.2552 making a likely interim support level. Due to the bearish momentum from the 2017 high, we could seek to short rallies all the way up to 1.30 to assume an eventual break below 1.2464 as the year progresses.

NZD teeters on the edge of the bullish trendline from the 2015 low. This may prove a tough level to crack upon first attempt, although also going against significant downside for NZDCAD is the 1% positive carry for the cross. Yes, it has narrowed by 25bps and the spread could shrink to 0.75% over the coming months, but if inflation stabilizes for NZ then expectations for a hike could quickly surface here too. For now, if we are to see a break of the trendline then the 50% and 0.908 low make a likely stalling point from a technical perspective.

View the full BoC statement here

- The recent softness in inflation is assumed to be temporary

- The economy has been robust, fuelled by household spending

- Significant amount of economic slack has been absorbed

- Growth is broadening across industries and regions

- Household spending will likely remain solid in the months ahead

- Exports should make an increasing contribution to GDP growth

- The Bank estimates real GDP growth will moderate further

- Output gap is now projected to close around the end of 2017

- The Bank’s three measures of core inflation all remain below 2 per cent.

- Factors behind soft inflation appear to be mostly temporary

- The Bank expects inflation to return to close to 2 per cent by the middle of 2018

- The current outlook warrants today’s withdrawal of some of the monetary policy stimulus in the economy

- Future adjustments to the target for the overnight rate will be guided by incoming data