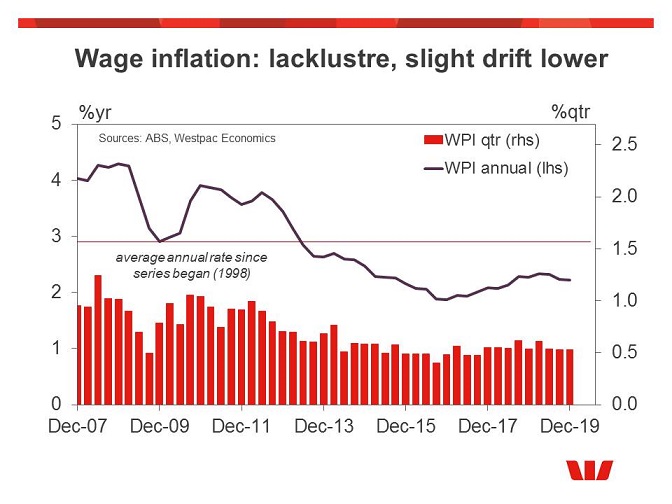

Q4 Wage Price: 0.5%qtr, 2.2%yr. Weak growth continues with no end in sight.

Australian wages continue their lacklustre performance. In the September quarter the Wage Price Index (WPI) lifted 0.5%, on par with market expectations and holding annual growth at 2.2%yr. That said, the second half of 2019 showed a very slight moderation, wage growth running at a 2.1% annual pace over the second half compared to a 2.2% pace over the first half of the year and a 2.3% pace over the second half of 2018. That compares to a cycle low of 1.6% over the second half of 2016.

Westpac’s current forecasts have wage inflation drifting holding around this lacklustre pace with a 2.3%yr gain in 2020 and a 2.2%yr gain in 2021. Weak wage inflation looks set to remain a signficant headwind to growth and, to the extent that it becomes more firmly embedded in expectations, an increasingly intractable problem for policymakers.

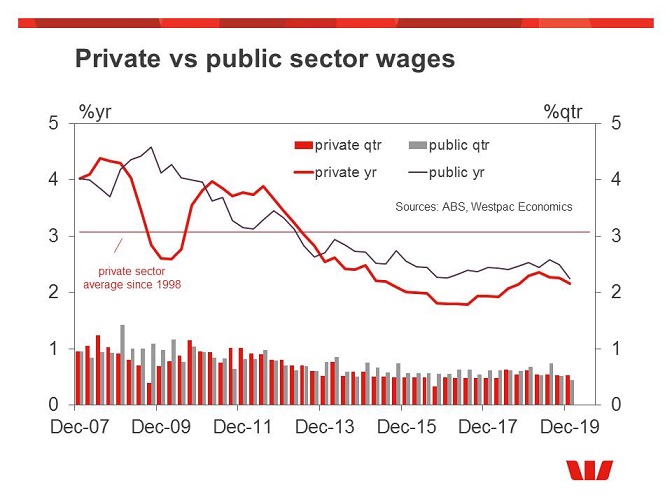

Private sector wages printed 0.53% in the quarter, a repeat of the 0.53% printed in the previous quarter and a slight step down from the 0.56% average over the year to June. The annual pace for private wages remained at 2.2%yr in rounded terms but eased in unrounded terms. This is in line with the average over the last six and a half years but well below the 3.1%yr average recorded over the longer history of the series (back to 1998).

Public sector wages growth is looking notably weaker, wages rising just 0.44% in the quarter, annual growth slowing to 2.2%yr. While that is in line with private sector gain, it is a record low for the public sector. The state detail shows a marked deceleration in Qld and SA and a more moderate slowing in NSW.

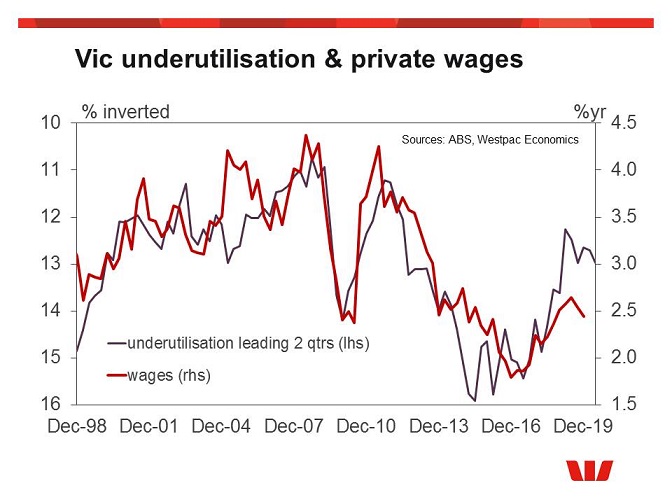

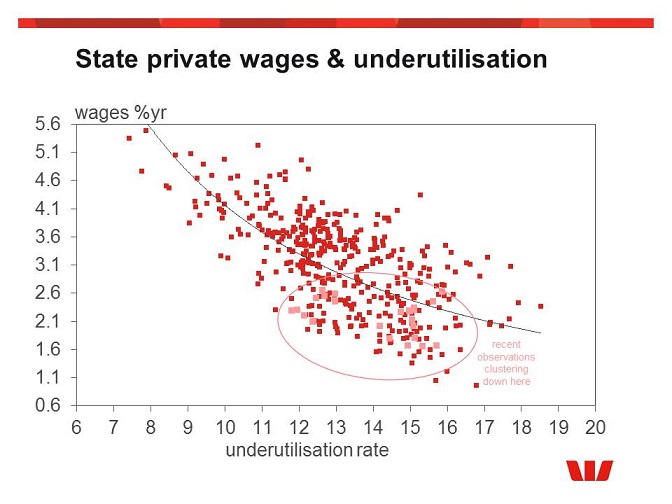

The wider state detail continues to suggest the very modest lift in wage inflation since 2017has run out of puff. Over the last year and a half, we have been been particularly interested how falling labour force underutlisation in Victoria would affect private sector wages growth in the state. After lifting from a low of 1.8%yr in 2016 to 2.2%yr in 2017 and 2.6%yr in early 2019, private wages growth in Vic has moderated slightly to 2.4%yr in Decembr 2019. Victoria still has the equal fastest pace of private sector wage inflation of the major states (now equal with SA), but ACT and Tas are outpacing slightly, both at 2.7%yr. NSW remains sluggish at 2.1%yr while Qld is 2.0%yr and WA is 1.8%yr.

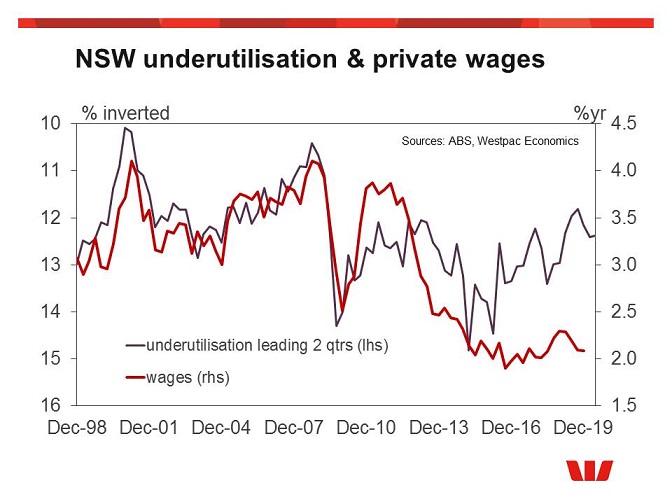

NSW continues to show the starkest disconnect between apparent labour market slock and wages growth. Despite the underutilisation rate trending lower from late 2016 to early 2019, private sector wage inflation has remained subdued, lifting only slightly from 2.0%yr in 2017 to 2.3%yr in 2018, and eased back to 2.1%yr in Q4 2019. This performance suggests it will be very difficult to generate a meaningful lift in wage inflation.

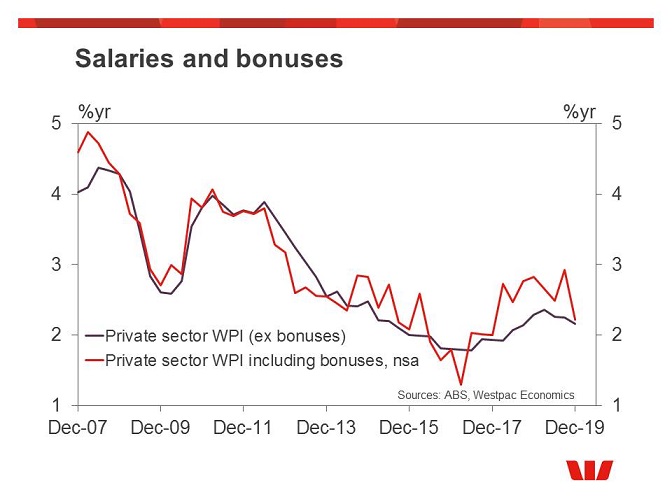

Private sector wages including bonuses had been seeing stronger growth pace than the main headline measure which excluding bonuses, but this outperformance ended abruptly in Q4, with annual growth in both converging to 2.2%yr. Indeed, the measure including bonuses flatlined in Q4 suggesting pressures on profitability significantly curtailed total wage payments. Note that some of this may also reflect slower growth in commissions in sectors such as real estate, which are in turn a byproduct of the house price cycle.

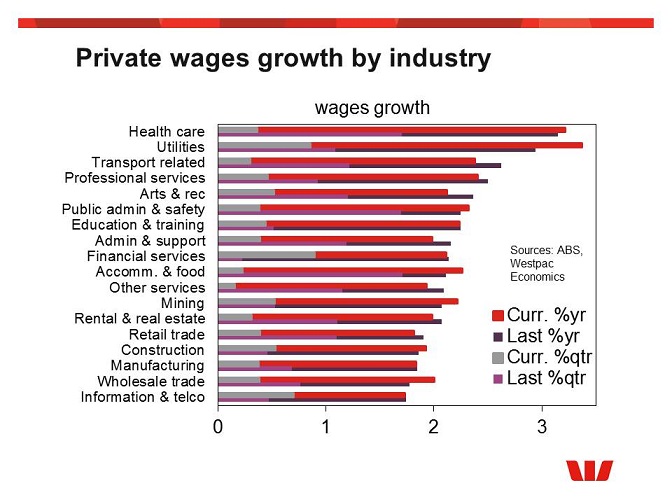

By industry, the fastest gains in wages are still mostly in what we consider to be non-cyclical sectors such as health care (3.1%yr); utilities (2.9%yr); professional & scientific (2.3%yr); and arts & recreation (2.2%yr). In contrast, key cyclical industries continue to show relatively weak wage growth, including: retail trade, construction and manufacturing (all running at 1.8%yr). Even in mining, where there is talk of a modest recovery in investment and talk of emerging shortages of skilled labour, wages are growing just 2.2%yr.

Strikingly, across the eighteen industries covered, only two (health and utilities) are seeing wages growth above 2.5%yr.

{kind=link}