The monthly read of CPI suggests a rosier outlook than the official quarterly read, although at 0.1% MoM this too may soften over the coming months. The RBA is in focus tomorrow to see if a fresh round of jawboning ensues.

Inflation data for Q2 was met with some scepticism, although we prefer to look at the brighter side of it. Yes, broad CPI softened and missed expectations yet the trimmed and weighted mean remained steady and hot the consensus. It is these latter CPI reads the RBA takes more notice of and as they have stabilised at record lows it does raise the potential for a base to occur.

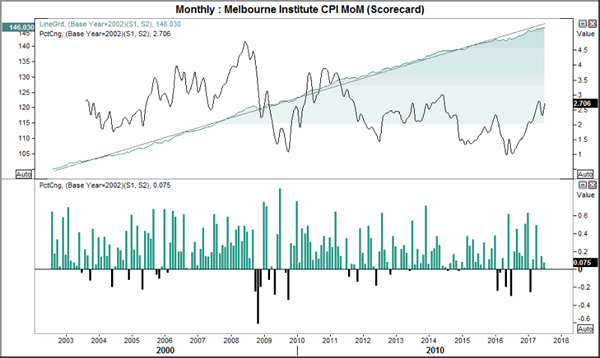

Today the Melbourne Institute released their monthly inflation read which estimates CPI to be at 2.7% YoY and 0.1% MoM. This is the third consecutive month below 0.2% which suggests the YoY rate will soften in due course unless the underlying index spikes higher.

Private sector credit increased by 0.5% MoM, its highest level since December which suggests support for growth and inflation. It is making headway after declining to just 0.2% in January, although seasonality is likely at play here.

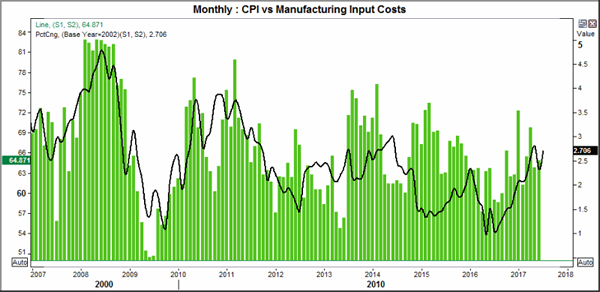

Early tomorrow AiG release their manufacturing PMIs. Currently at 55, the index sits above the 1yr average and the sector has enjoyed 9 consecutive months of expansion. We will keep an eye on the input costs as this tends to track CPI relatively well. So, a rise of input costs assumes this to be passed onto the consumer and therefor provide cost-push inflation.

Private sector credit increased by 0.5% MoM, its highest level since December which suggests support for growth and inflation. It is making headway after declining to just 0.2% in January, although seasonality is likely at play here.

Early tomorrow AiG release their manufacturing PMIs. Currently at 55, the index sits above the 1yr average and the sector has enjoyed 9 consecutive months of expansion. We will keep an eye on the input costs as this tends to track CPI relatively well. So, a rise of input costs assumes this to be passed onto the consumer and therefor provide cost-push inflation.

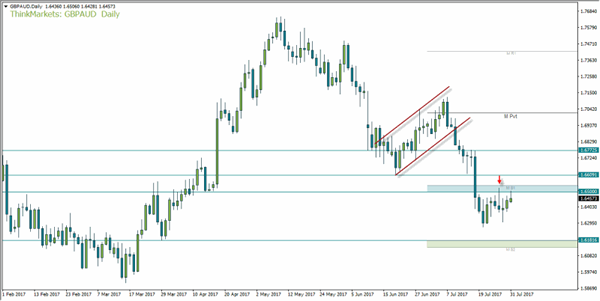

GBPAUD remains beneath the monthly S1 and 1.65 resistance zone. The upper wick of Wednesdays’ bearish pinbar remains unchallenged, so we are seeking signs of weakness on H1 and H4 to consider a bearish swing trade. If we are to see prices move higher from here we can still consider fading below 1.66. It’s possible we may see an ABC correction terminate here before losses resume.

As this is the last trading day of the month the pivots will be recalculated. So we can finetune potential targets from tomorrow, although the 1.62 area is still viable support as it is just above the 30th March low.