U.S. Review

While Risk Remains, The Worst Appears to Be Behind Us

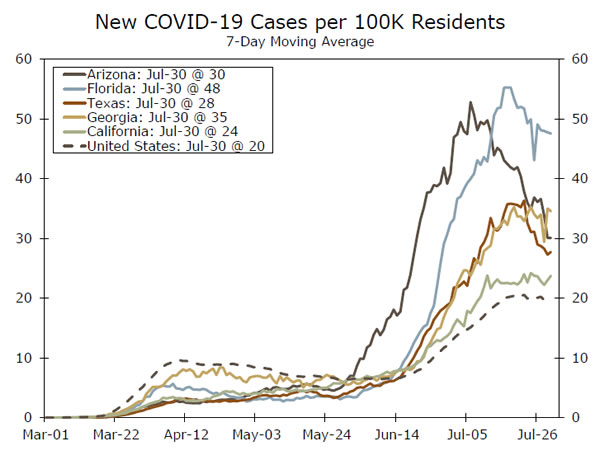

- The resurgence in COVID-19 in much of the Sun Belt appears to have topped out, although cases are rising faster in some smaller mid-Atlantic states and in parts of Europe, Asia and Australia.

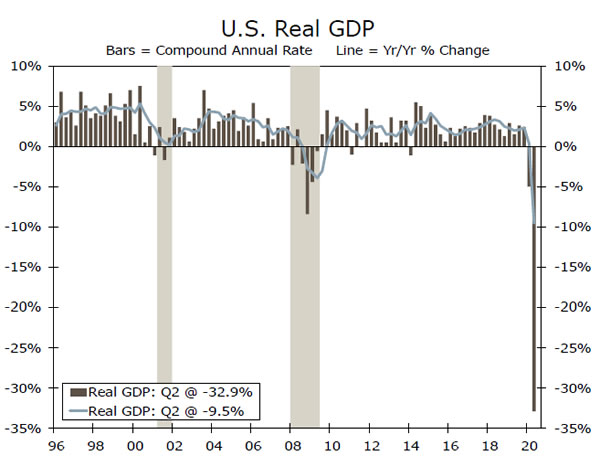

- Real GDP declined in line with expectations, plunging at a record 32.9% annual rate.

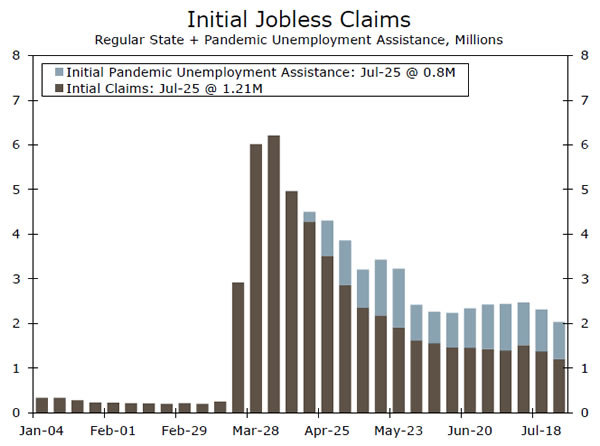

- Jobless claims rose for a second consecutive week, and continuing claims also increased.

- Consumer confidence faltered as the second wave of COVID-19 infections triggered a pullback in economic engagement.

The Second Wave Appears to Have Crested

Fed Chair Jerome Powell made it clear this week that the spread of COVID-19 and efforts to contain it will largely determine the path and pace of the economic recovery. While the FOMC policy statement was widely interpreted to be dovish, there is little the Fed can do in the near-term to bolster economic prospects. Fiscal policy is crucial and an agreement needs to be reached soon to extend a significant level of pandemic unemployment insurance and provide additional relief to businesses and households. The Senate’s recess is scheduled to start August 10 and they will not meet until after Labor Day, when campaigns shift into high gear.

The latest data on the spread of the virus are a bit more encouraging. The troubling flare-up of cases throughout many of the most populous parts of the Sun Belt appears to have topped out. The seven-day moving average of new cases has fallen nearly 40% in Arizona over the past three weeks. Over the last two weeks in Texas and Florida, the same metric has fallen 19% and 13.9%, respectively. The number of deaths, which lags new cases by about three weeks, continues to trend higher.

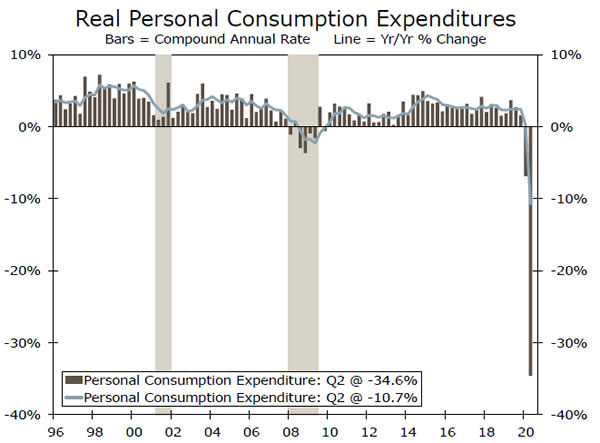

Real GDP plunged at a 32.9% annual rate, which was actually a little less horrid than expected. Cutbacks in consumer spending accounted for most of the drop, with the bulk of cutbacks occurring on services spending, which tumbled at a 43.5% annual rate. This category picks up spending on many of the hardest hit parts of the economy, such as restaurants & bars, travel & leisure as well as medical care, which tumbled as many medical and dental practices completely shut down in April. A 49% annual rate plunge in investment outlays was a big downside surprise, including a 39% annualized decline in residential investment.

Data since April have largely been more positive and the economy ended the second quarter at a much higher level than it averaged for the quarter, meaning that third quarter GDP growth is poised for a blowout to the upside, even if economic activity hits a soft spot this summer. Real consumer spending, for example, rose 5.2% in June. The quarter-end value for personal consumption outlays is 6.1% above the average for the quarter, meaning that personal consumption would rise at a 26.8% annual rate in the third quarter if consumer spending was unchanged for the every month of the quarter. Of course, that is not likely to happen. Spending is still rising and the resurgence in home buying should provide quite a bit of follow through to many important consumer categories.

The assist from the base effect is well timed, as most of the high frequency data that we track suggest that economic activity did in fact pull back a notch in mid-to-late July. First-time claims for unemployment insurance have risen for two weeks in row, after falling for 15 consecutive weeks. The absolute level of claims remains atrociously high, with the latest four-week moving average at a 1.369 million, or more than twice its worst level during the Great Recession. High frequency data, such as the number of restaurant diners tracked by OpenTable and hours worked according to Womply, also show activity pulled back in July, although the most recent data looked a touch stronger, suggesting a pause rather than a double dip.

U.S. Outlook

ISM Indices • Monday & Wednesday

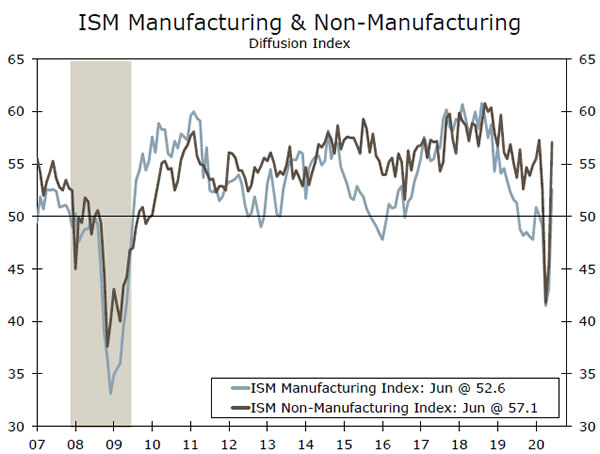

Last month’s increase in the non-manufacturing index brought it roughly in line with its February level, while the manufacturing index reached its highest level in more than a year. A V-shaped recovery was perhaps unsurprising for these purchasing manager indices. One would expect survey respondents to indicate business activity improved as lockdown orders were lifted. While the survey period for July will correspond with the rising case growth and a slower mobility recovery seen through the late-June and early-July, we expect the re-opening momentum will keep both of these indices in expansion territory for the month. Absent new, blanket lockdown orders, a steep drop similar to what we saw in April seems unlikely, but these sectors are far from out of the woods. Global demand remains weak, which should keep a lid on manufacturing’s resurgence, while localized setbacks stemming from virus flare-ups threaten the nascent service sector recovery.

Previous: 52.6 & 57.1 Wells Fargo: 53.4 & 55.3 Consensus: 53.6 & 55.0 (Mfg. & Non-Mfg.)

Trade Balance • Wednesday

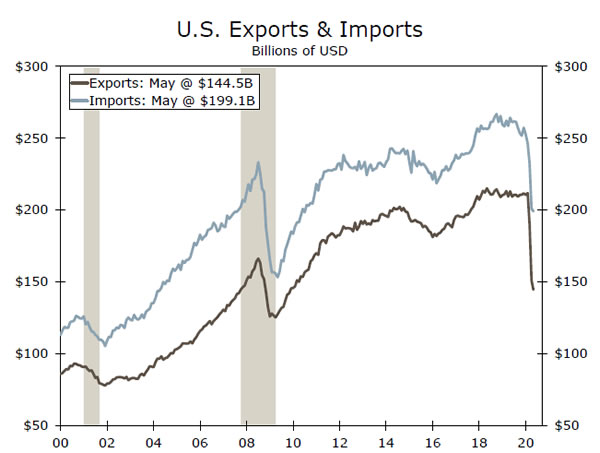

Trade flows have been anemic since the global economy closed its doors in April. The advanced trade report released Wednesday showed that imports and exports increased in June, but both remain meaningfully off of their pre-COVID levels. After accounting for June’s increase, advance exports are still down nearly a quarter and imports are off roughly 12% from pre-virus February levels. As with so many indicators in the wake of the COVID crisis, headline jumps may be flattering, but it will be some time before the level can return to normal. Moreover, it is not exactly clear what normal will look like. Trade flows were slowing even before the pandemic, and the immense shock to global supply chains witnessed over the past few months could lead to some permanent reorientation. While these trends in globalization continue to develop, the gargantuan swings in consumption and investment mean that trade is unlikely to play an outsized role in the GDP conversation in the coming months.

Previous: -$54.6B Wells Fargo: -$49.7B Consensus: -$50.3B

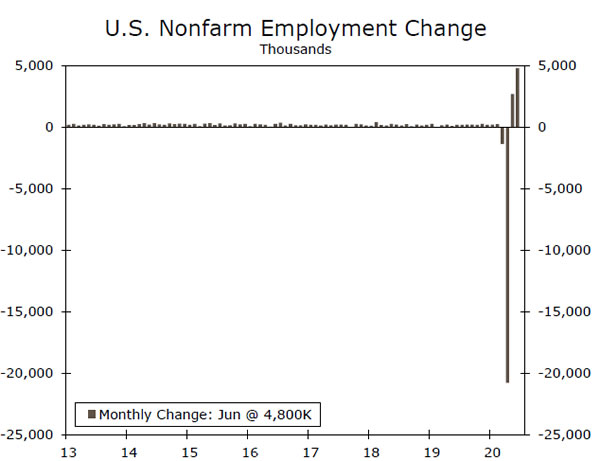

Employment • Friday

The past few months have seen historic swings in the number of people on nonfarm payrolls. These moves have reflected the unusual nature of this recession, which is more of a surreal exogenous event than a typical cyclical recession. They have also been tremendously difficult to anticipate. While jobless claims have been tracked closely over the past few months, they can only tell some of the story. The labor market has seen an unprecedented level of churn and even if one can infer the number of people let go in a month, it is difficult to know how many people were hired back in other parts of the economy.

For July, continued declines in the number of people claiming unemployment suggest that people were still being hired back from the shutdown period. There have been a number of indications, however, that the recovery has lost momentum. While the stalling recovery may not be captured in July’s report, if activity continues to flat-line it could certainly weigh on job figures in the months ahead.

Previous: 4,800K Wells Fargo: 2,000K Consensus: 1,510K

Global Review

Q2 GDP Data Shows Impact of COVID-19

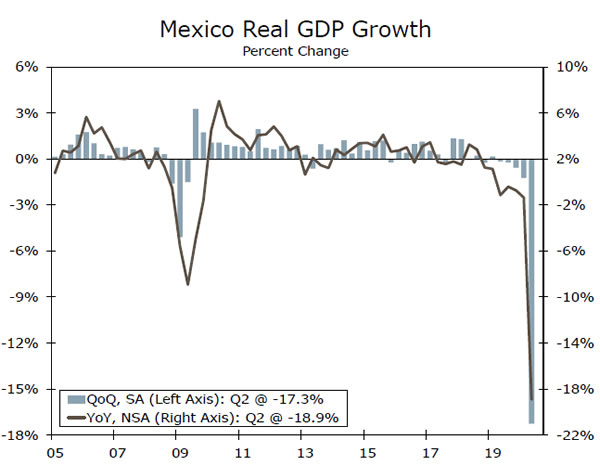

- As expected, Mexico’s economy contracted significantly in the second quarter. The effects of COVID-19 and collapse in oil prices weighed heavily on the economy in Q2, while a lack of fiscal policy support from the current administration adds challenges to Mexico’s growth outlook going forward.

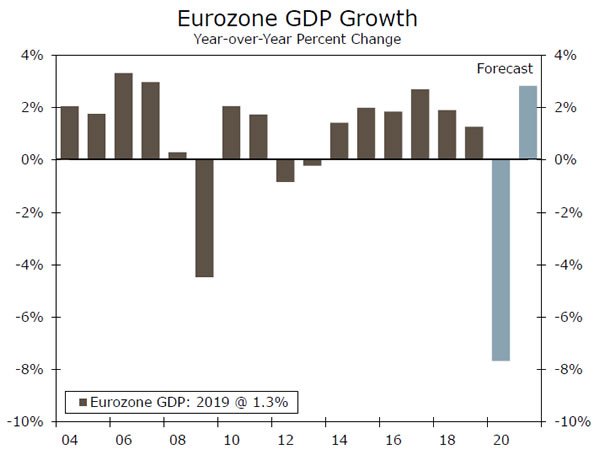

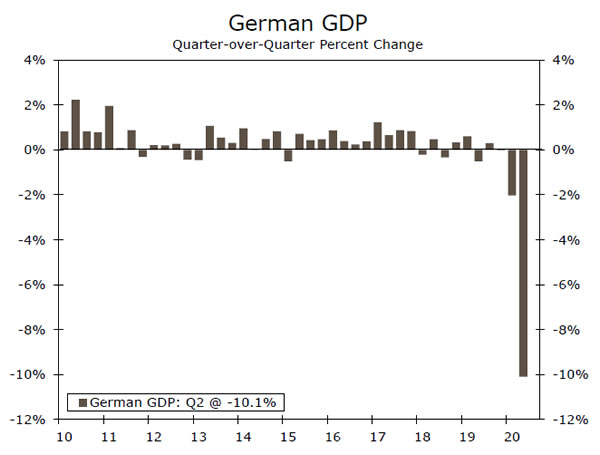

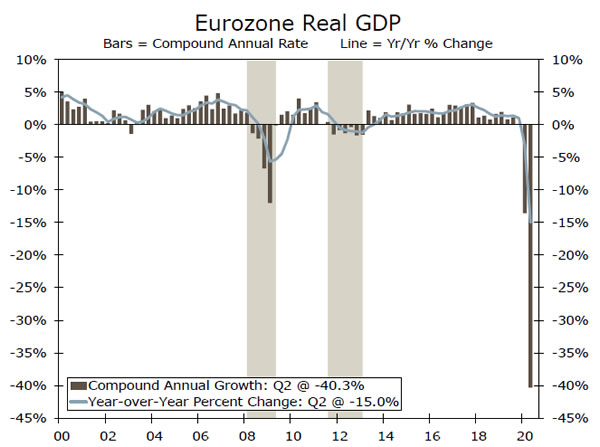

- GDP data were released across Europe as well, with the German economy recording a third straight quarterly contraction. Eurozone GDP performed roughly in line with expectations, recording a large decline in Q2. Despite the large contraction, we are optimistic on the Eurozone economy’s prospects for the second half of the year.

Mexico’s Economy Experiences Significant Contraction

Over the last few months, we have highlighted the dire situation the Mexican economy is currently in. Following an annual contraction last year, Mexico’s economy is poised to experience another annual contraction this year, close to 10% in our view, as the effects of COVID-19 and the collapse in oil prices are likely to weigh heavily on the economy. On Thursday, we received additional insight into just how sharp the deceleration this year will be as the Mexican economy contracted 17.3% quarter-overquarter in Q2, the deepest contraction on record in Mexico. While Q3 GDP data should be better, we still forecast a Q3 contraction as the AMLO administration has done little to provide fiscal stimulus to support the economy. Without fiscal support the Mexican economy will struggle to gather momentum into the end of the year, especially as COVID-19 confirmed cases continue to rise. In addition, we believe the Central Bank of Mexico may be close to ending its monetary easing cycle. Recent commentary from policymakers lead us to believe the pace of rate cuts will slow in the coming months, which relatively high policy rates could also act as a further drag on the economy.

German Economy Posts Sharp Decline

GDP data were released across Europe as well, with Germany reporting Q2 data on Thursday. As expected, the German economy contracted significantly in the second quarter, declining 10.1% quarter-over-quarter. The Q2 contraction was also worse than consensus forecasts, which could mean the annual contraction in Europe’s largest economy could be deeper than previously estimated. The contraction marks the largest quarterly drop in GDP on record in Germany and confirms the German economy has now contracted for three straight quarters. Considering Germany is typically one of the stronger economies within the Eurozone from an underlying fundamentals perspective, the Q2 decline just shows how severe the impact of COVID-19 has been. Going forward, we are optimistic on the German economy’s ability to recover and exit technical recession in Q3. Some of the leading indicators we track have shown improvement and signal the economy is on track for a strong rebound in the second half of the year.

Eurozone Economy Performed as Expected

On Friday, GDP data for the Eurozone region were also released. As expected, the Eurozone economy contracted rather significantly in Q2. On a sequential basis, the Eurozone economy declined 12.1%, which matched consensus forecasts. One a year-over-year basis, the economy contracted 15%, a little more than the consensus forecast of 14.5%; however, given the magnitude of the contraction, we view this as being relatively in line with expectations. As we have highlighted in the past, we believe the Eurozone economy is on pace to exhibit a strong recovery in the second half of the year. Activity indicators such as retail sales have rebounded quite nicely, while sentiment indicators such as manufacturing and services PMIs are back in expansion territory. In addition, and perhaps more encouraging, all 27 European Union countries have approved the EU recovery fund, which will enable shared lending across all countries with proceeds going to countries hit hardest by the COVID-19 pandemic. As of now, we feel the Eurozone is in good position to rebound and we recently upgraded our annual 2020 GDP forecast to reflect more optimism.

Global Outlook

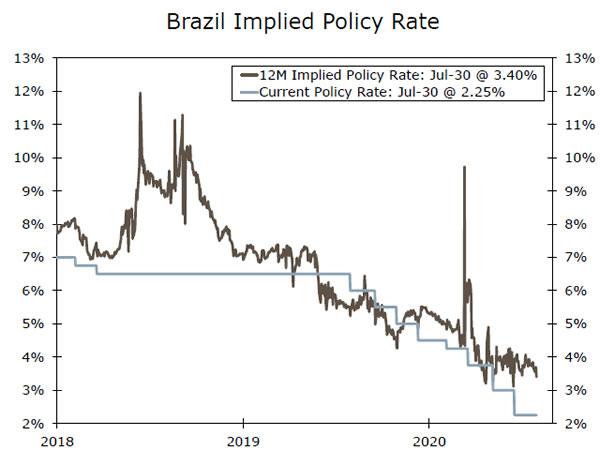

Brazilian Central Bank • Wednesday

Brazil has been among the countries hit hardest by the COVID-19 pandemic. As of now, the country has the second highest amount of infections, while authorities have done little to contain the spread of the virus or flatten the curve. In response, the Brazilian Central Bank (BCB) has eased monetary policy rather aggressively, arguably more aggressively than any other emerging market central bank. Through the end of July, the BCB cut its Selic rate 225 bps and we believe it will opt to cut rates another 25 bps at next week’s meeting. With growth and inflation dynamics still relatively subdued, and the currency recouping some of its earlier losses, we believe there is scope for additional rate cuts. However, going forward, markets are pricing in eventual rate hikes from the BCB. In fact, over the next 12 months, markets believe the BCB could raise rates by 150 bps. We believe the market is mispriced and that the Selic rate will rise much slower than what is currently priced in.

Previous: 2.25% Wells Fargo: 2.00% Consensus: 2.00%

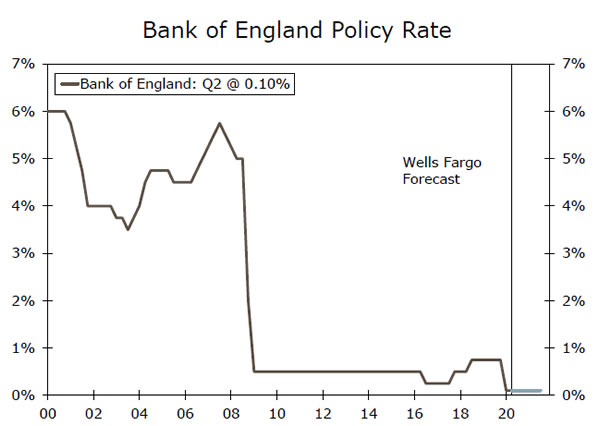

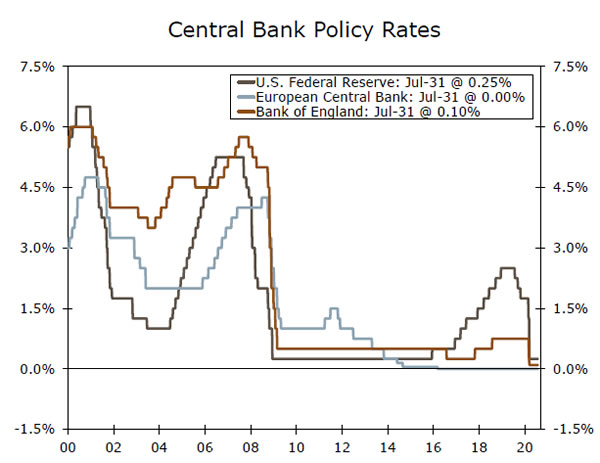

Bank of England • Thursday

Earlier this year, the Bank of England (BoE) followed the trend of cutting interest rates aggressively following the COVID-19 outbreak. In mid-March, the BoE cut its Bank Rate to 0.10% and has signaled rates will be held around 0% for the foreseeable future. In addition to lowering interest rates, the BoE also moved forward with an asset purchase program in an effort to jumpstart the economy in the midst of a sharp COVID-19 led slowdown. In June, the BoE raised the overall asset purchase target to £745B and we feel as if the central bank has scope to raise the purchase target even further. While raising the asset purchase target likely won’t occur next week, we believe the Bank of England may begin to signal markets that its quantitative easing program may be expanded soon. In that context, we believe monetary policymakers will look to raise the asset purchase target another £100B to £845B in Q4, while keeping policy rates on hold at 0.10%.

Previous: 0.10% Wells Fargo: 0.10% Consensus: 0.10%

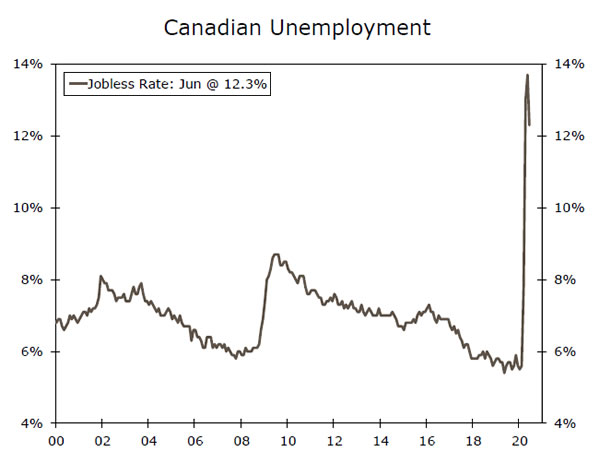

Canada Jobless Rate • Friday

The Canadian economy has been impacted through multiple channels over the course of 2020. Obviously, the COVID-19 shock and subsequent lockdown measures placed pressure on the economy, while the sharp sell-off in oil prices also weighed on activity and economic output. In response, the labor market came under stress, with millions of jobless claims being filed and the unemployment rate reaching 13.7% in May. In recent months, the labor market has shown signs of improvement as the Canadian economy created almost 953K in June and the jobless rate has started to tick lower. In June, the jobless rate dropped to 12.3%, and in July, we expect the labor market to again show signs of improving and for the unemployment rate to tick lower. We also believe the Canadian economy bottomed out in April and is on the long road to recovery. While the GDP contraction in Q2 will be severe, we expect a strong Q3 rebound and for the recovery to persist in 2021.

Previous: 12.3%

Point of View

Interest Rate Watch

No July Fireworks at Fed Meeting

The Federal Open Market Committee (FOMC) made no major policy changes at its meeting this week and by unanimous decision, kept its target range unchanged at 0.00% to 0.25%. The FOMC also announced that it would continue to buy Treasuries at the current pace of $80 billion/month as well as mortgage-backed securities (MBS) at the current $40 billion/month. Further liquidity to the financial system through repurchase agreements (repos) is something the FOMC said it stands ready to do, although there has not been much demand for repo transactions by financial institutions in recent weeks.

The committee continued to stress that the economy is very weak at present and acknowledged that the outlook is highly uncertain and “will depend significantly on the course of the virus.”

As it did at the June 10 policy meeting, the FOMC opened its statement pledging to use “its full range of tools to support the U.S. economy in this challenging time.”

No Forward Guidance

There was no explicit mention of forward guidance in the FOMC’s statement. That is coming eventually, though we suspect the committee will wait until its strategic review is finished before adopting some form of explicit forward guidance. Given our outlook for unemployment to remain high and inflation to remain low, we feel confident that the FOMC will adopt some form of explicit forward guidance at either its September 16 policy meeting or its meeting on November 5.

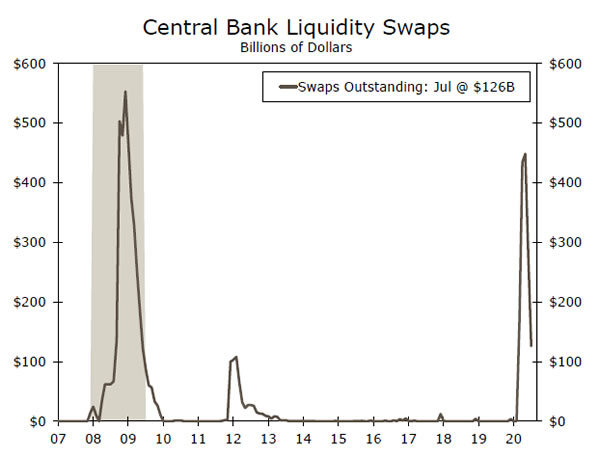

Foreign Currency Swap Lines

The FOMC also announced that it would extend the temporary swap lines and repurchase agreements that it put in place with foreign central banks through March 2021. These liquidity facilities were instrumental in easing strains in dollar funding markets earlier this year. Foreign currency swaps outstanding shot up to nearly $450 billion in late May, but have been rolling off the Fed’s balance sheet subsequently as they have matured. This move could help mitigate strains in the dollar funding markets.

Credit Market Insights

Investors Exit Turkey’s Bond Market

Turkey is experiencing widespread withdrawals from its local currency bond market, adding to the country’s liquidity and economic issues. Foreign investors withdrew just over USD$7B in the first half of 2020, a record six-month drawdown at a time when the share of non-resident ownership of outstanding Turkish bonds has fallen significantly. Recently, the Turkish Ministry of Finance has taken steps to boost access to Turkey’s local currency denominated bonds, including the agreement with Euroclear to allow international investors access to the Turkish government bond market, including lira, euro, U.S. dollar and gold denominated bonds. Despite these efforts, local bonds have become less attractive to foreign investors given the imbalances within the Turkish economy. During the height of the COVID-19 pandemic, investors fled riskier assets such as Turkish bonds, while other factors such as a negative real yield on Turkish sovereign debt also contributed to foreign investors retreating from Turkish bonds.

Concerns are building over the country’s reliance on foreign investing, given that Turkey has one of the largest gross external financing needs among its peers. As foreign investors continue to flee, and COVID-19 looms over the Turkish economy, the central bank has been purchasing government bonds to support its economy. The central bank set the bond purchase limit at 10% of its assets, up from 5% in December, and now holds roughly USD$13B of government domestic debt. Overall, we remain concerned about building imbalances within the Turkish economy, including a widening current account balance.

Topic of the Week

No One CARES Anymore?

Under the CARES Act passed in late March, recipients of unemployment insurance have been receiving an additional payment of $600 per week. This emergency portion of benefits is slated to expire Saturday, however, leading to a substantial drop in household income if no new program takes its place.

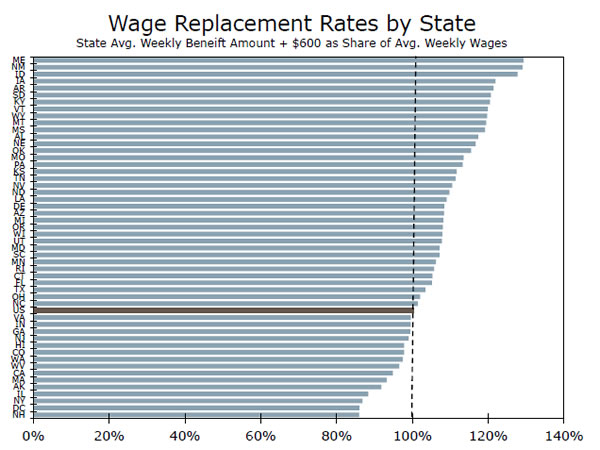

It is hard to overstate the scale of the emergency unemployment benefits. In 36 states, workers on average can earn more than the state’s pre-pandemic wages (top chart). On the whole, the Congressional Budget Office estimates five out of six laid off workers are earning more under enhanced benefits than when working. While the generosity of the emergency benefits creates a shortterm financial disincentive to return to work, millions of workers do not have that option; currently there are only 5.4 million jobs available compared to 17.8 million unemployed workers.

How Bad a Hit to Household Spending?

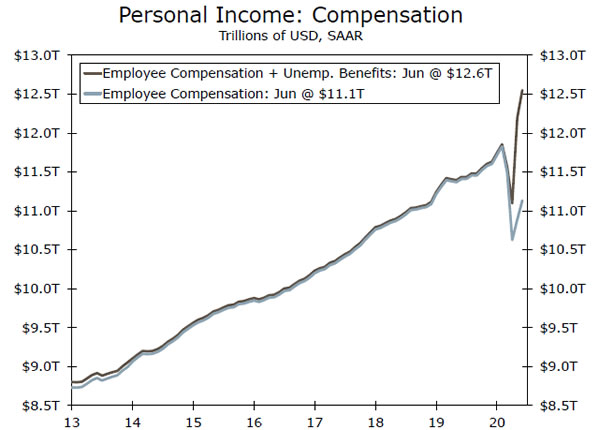

Income from unemployment benefits has more than offset the drop in employee compensation in recent months (middle chart). Thus if we account for roughly 30 million unemployed Americans, the rough math works out to about $72 billion per month of lost income when the additional $600 weekly benefit expires. The June personal income and spending report showed total Pandemic Unemployment Compensation payments (where the temporary weekly supplemental payment is recorded) of about $78 billion in June; so the rough estimate fits the reported figures.

Over the past three months, consumer spending has averaged $1.1 trillion dollars a month. Assuming all of the lost income were to translate into a commensurate drop in personal consumption, all else equal, spending for August could come in about $78 billion lower, a monthly decline in the neighborhood of 7%. Prior to the current crisis, the largest monthly decline on record was 2.1% in figures that go back to the 1950s. That is not our baseline assumption, but it puts the size of the loss in scope.