The Bank of England will conclude its latest policy meeting on Thursday, announcing its decision at 12:00 GMT. As it’s November, the Bank will also be publishing its quarterly Monetary Policy Report alongside the meeting minutes. But while a virtual press conference is pencilled in too, it will be pre-recorded and released at 14:15 GMT, as has become the customary practice for the BoE during the pandemic. Following the UK government’s decision to place England under a month-long lockdown, it’s almost certain the Bank will beef up its asset purchases this week. However, pound traders will likely be more preoccupied with what policymakers have to say about the possibility of negative interest rates as the medium-term outlook for the economy remains bleak.

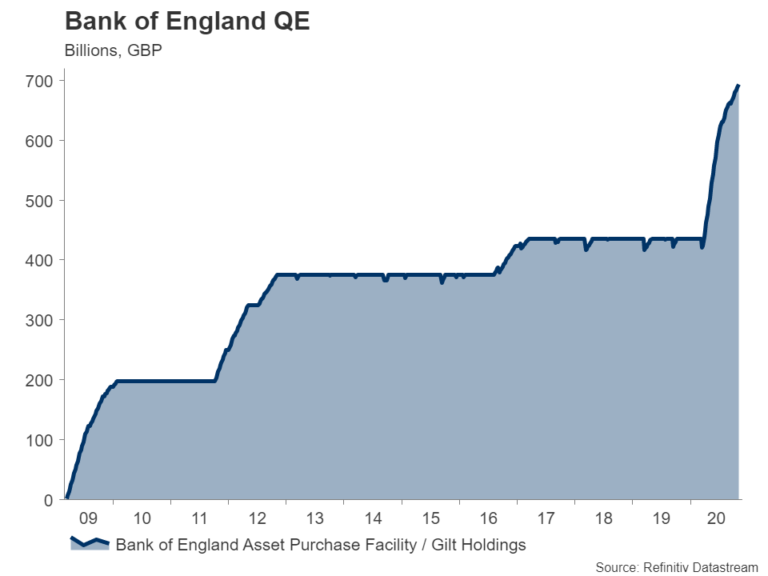

More QE on the way

The BoE last increased its bond purchases in June, adding a further £100 billion to the £200 billion announced in March at the height of the virus crisis. It’s widely expected that Monetary Policy Committee (MPC) members will ramp up the programme by another £100 billion in November as an end to the pandemic is nowhere near in site.

Like many other European countries, England has been forced into a second national lockdown as coronavirus cases continue to surge, threatening to overwhelm health services. Wales and Northern Ireland, which had already imposed tougher curbs, are set to exit those measures in the coming days, with only Scotland so far escaping a wider lockdown. The renewed restrictions are bound to derail the recovery, which has been on shaky ground since August when Covid cases first started spiralling out of control again.

A recovery in trouble

Subsequently, analyst forecasts for Q4 GDP are being sharply revised lower and the BoE’s latest projections will probably underscore the deteriorating growth outlook. Although, any contraction recorded in the December quarter is unlikely to be anywhere on the scale experienced under the first lockdown, it would nevertheless push a full recovery further into the future and exacerbate the pain for businesses striving to survive under the tough virus restrictions.

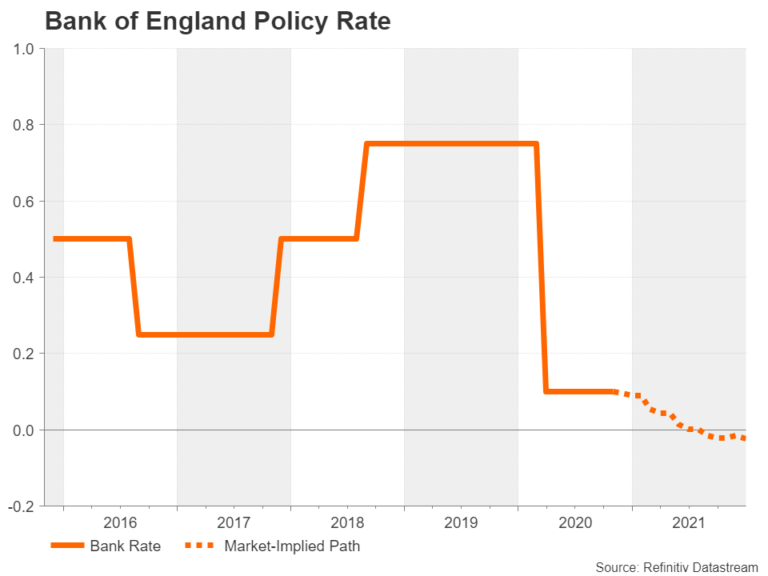

If the MPC is more downbeat about the economy’s prospects than what investors are anticipating, that could intensify speculation that the Bank will eventually lower its benchmark rate to below zero as it seeks to enhance its policy tools to fight the downturn. Any comments on negative rates in the policy statement or Governor Andrew Bailey’s press briefing will also be watched closely for fresh clues.

Too early for negative rates?

However, Bailey will probably steer clear of adding anything new to the conversation as the Bank has yet to complete its review about the effects of negative rates on the banking system. Moreover, with negotiations on a post-Brexit trade deal yet to be completed and given the unpredictable path of the virus, the BoE’s November forecasts will have a lot of uncertainty attached to them. That implies policymakers won’t have a clearer view on the economy until February’s Monetary Policy Report when the Brexit outcome will be known and a vaccine might also be available by then.

Hence, the biggest surprise that the BoE could deliver on Thursday is a smaller- or bigger-than expected change to its asset purchase programme, with the former being a more likely scenario. Following the £300 billion boost announced already this year, the BoE is on course to own 50% of all outstanding UK government bonds. Whilst there can be no doubt the supply of new gilt issuance will remain high over the coming year, the Bank may nonetheless be wary about the pace at which it increases its quantitative easing (QE) programme going forward for fear of draining liquidity out of the bond market.

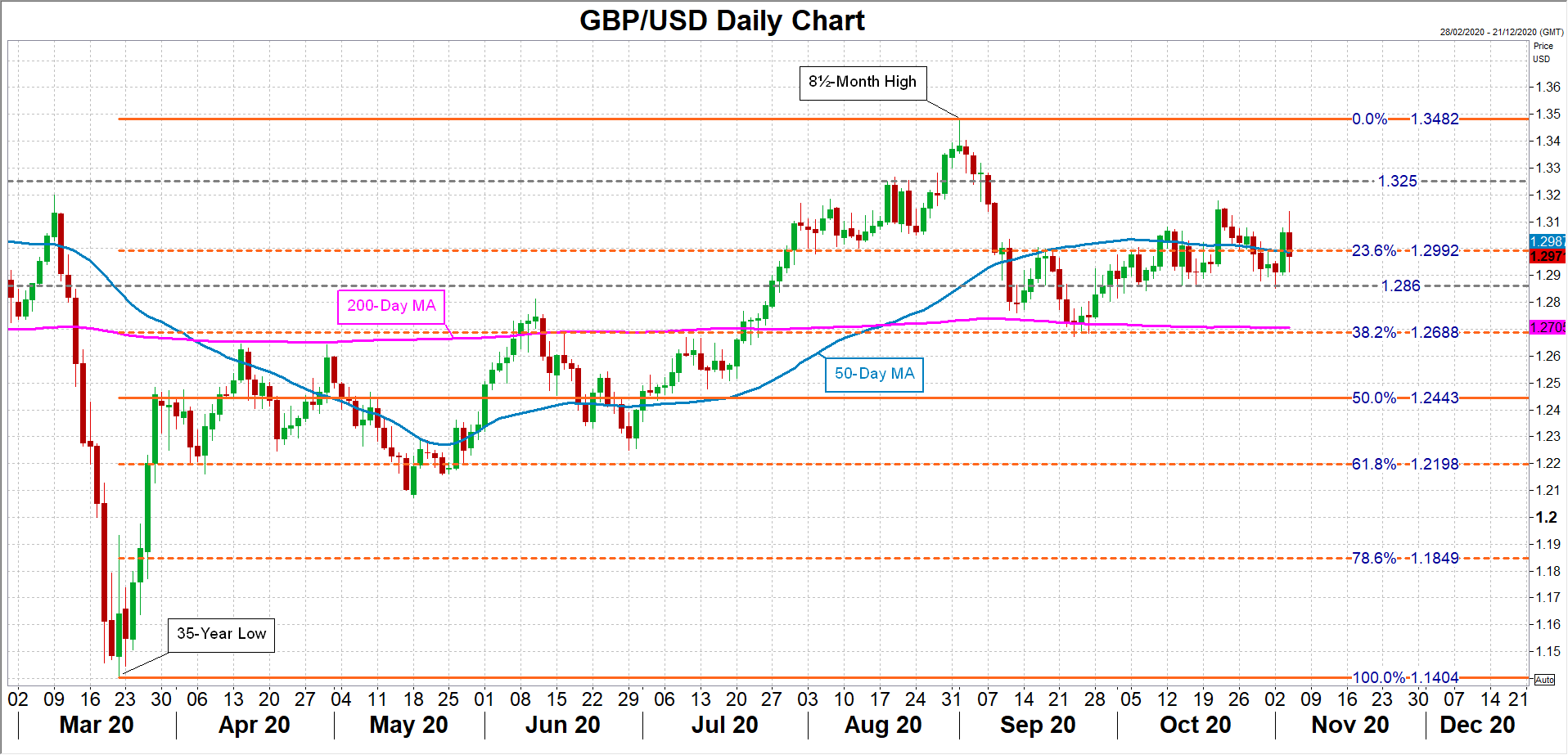

Brexit and risk appetite are bigger drivers for pound

Should the Bank raise QE by £100 billion as expected, the pound’s moves will be driven entirely by the Brexit headlines as talks continue on the future trading relationship with the EU. Having rebounded to around the $1.30 level, cable will have its sights on the October top of $1.3177 followed by the $1.3250 resistance area if there’s progress in those talks. Though, a smaller injection of cash by the BoE, say in the region of £75 billion, could also provide a short-term lift for the pound.

However, in the event that MPC members provide explicit signals about negative rates, cable will have a hard time holding above the $1.30 level and could re-test the $1.2860 support before retreating towards its 200-day moving average in the $1.27 region. Having said that, broader risk appetite will be just as important as Brexit and virus developments in setting the tone for sterling in the coming weeks.

{kind=link}