- Stocks at records or near highs as US Republicans change tune on new stimulus

- Brexit talks go down to the wire, but will France cause a last-minute upset?

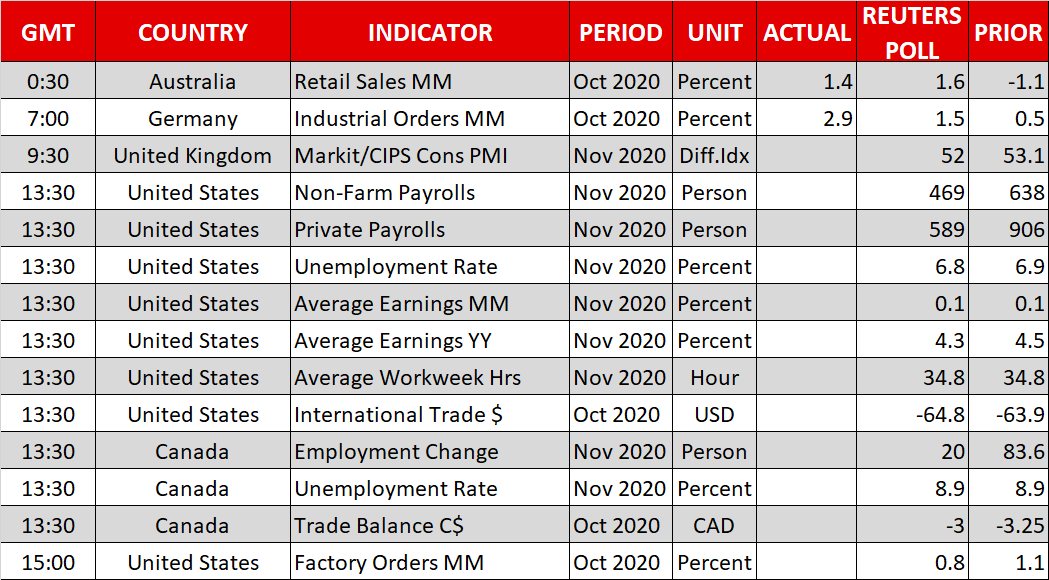

- Dollar slide pauses ahead of NFP report

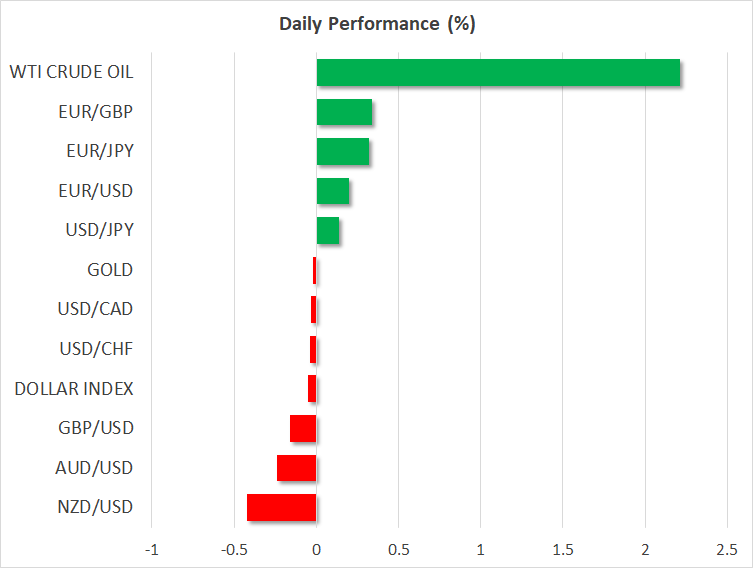

- Oil jumps to 9-month high despite OPEC+ raising production early

Fresh hopes for US stimulus deal before Christmas

Support for a bipartisan stimulus proposal of up to $908 billion gained unexpected traction yesterday as more and more Republicans threw their weight behind the plan. The worsening virus trend in the United States on all fronts – infections, hospitalizations and deaths – has raised the urgency for another substantial fiscal package to support the economy.

Without further aid, 14 million American workers will face losing their unemployment insurance from the federal government at the end of the month. Restrictions have been tightening across many states in recent weeks, with most of California now under a stay-at-home order as daily cases of Covid-19 continue to surge.

Senate Majority Leader Mitch McConnell, who has yet to drop his insistence that any new stimulus deal should not exceed $500 billion, is under pressure from all sides, including the White House, to reach some kind of a deal with the Democrats before the holiday recess.

If an agreement is struck, it would be Christmas coming early for the stock market, which is still riding high on the back of the vaccine optimism. The Nasdaq Composite and Nasdaq 100 both closed at new record highs on Thursday (though, just about), as traders are hopeful that the arrival of a vaccine will enable economic activity to return to normal by the middle of next year. The S&P 500 closed just shy of the previous day’s record, but e-mini futures for all Wall Street indices were headed higher at the start of European trading as the mood improved further.

Dollar bears pause for breath

The vaccine breakthrough and the renewed optimism for a fiscal boost by Congress has been a boon for the never-ending rally in equity markets but has spelled disaster for the mighty US dollar. The dollar index tumbled to a fresh 2½-year low yesterday, as stronger risk appetite combined with falling real yields have triggered widespread dollar selling.

This may be good news for the US economy as the weaker greenback would benefit American exporters but may cause headaches for policymakers in other countries, particularly those at the European Central Bank who are openly uncomfortable about the euro trading above $1.20. The single currency looks set to have a just as strong month in December as it did in November as it fast approaches the $1.22 level.

However, the dollar’s descent has slowed slightly today, as apart from the euro, other majors such as the pound, aussie and kiwi were down on the day. This is likely down to some caution ahead of the latest nonfarm payrolls report due out of the US at 13:30 GMT. Jobs growth is expected to have slowed in November but there is a risk of a small upside correction in the dollar should the numbers miss expectations by only a small margin.

Brexit talks hit a new snag, pound skids

British and European Union negotiators have been working around the clock this week to try and hammer out a deal on a post-Brexit trade accord. Increasing signs that a deal was imminent had lifted the pound to a one-year high of just under $1.35 yesterday. However, cable has since retreated to around $1.3425 as reports suggest France has toughened its position, prompting UK negotiators to complain about “new elements” being brought into the almost-ready agreement at the last minute.

Whether all this is one final round of posturing remains to be seen, but with the talks now being described as having gone backwards, negotiations could drag into next week.

Oil brushes off disappointing OPEC+ compromise

Crude oil prices raced higher on Friday to reach their highest level in nine months as the positive sentiment in the broader markets offset the disappointment that the OPEC+ cartel failed to agree on an extension of the output cuts beyond the end of this year. WTI futures rose above $46 a barrel, while Brent crude is eying the $50-a-barrel level.

Under the agreement reached, OPEC and non-OPEC countries will increase output by 500 million barrels a day from January and will meet each month to review whether to adjust output by no more than 500 million bpd in either direction thereafter. But other than a minor dip in prices, investors have barely reacted to the prospect that oil production will start to gradually rise in 2021, suggesting they see the compromise as being enough to prevent the build-up of oversupply.