Sunrise Market Commentary

- Rates: Markets (too) dovish positioned ahead of JH?

Expectations of pre-announced policy changes by Draghi and/or Yellen at the Jackson Hole economic symposium seem too low. Therefore, we think that the market reaction will be bigger in case of a hawkish hint (initiate sell-on-upticks) than in case of keeping the dovish line (test of contract highs). - Currencies: Yellen and Draghi to decide on next directional USD move

FX traders will focus on the Jackson Hole speeches. Fed’s Yellen giving more weight to financial stability risks might support the dollar, especially if Draghi refrains from given concrete details on the scaling back of APP. However, several other scenarios are possible.

The Sunrise Headlines

- US equities ended up to 0.2% lower yesterday with investors mainly waiting on comments from the central bankers meeting in Jackson Hole. Overnight, most Asian stock markets manage to eke out some gains.

- US President Trump has blamed the two most powerful Republican leaders in Congress for a looming crisis over the debt ceiling that must be raised this autumn in order to prevent the US from defaulting on its national debt.

- Japan’s core consumer prices rose 0.5% Y/Y in July to mark a seventh straight gaining month, a sign the economy is making steady but painfully slow progress toward meeting the central bank’s 2% inflation target. The August Tokyo core CPI rose by 0.4% Y/Y, beating 0.3% Y/Y expectations.

- A Gulf of Mexico storm rapidly intensified spinning into the potentially biggest hurricane to hit the mainland United States in 12 years and taking aim at the heart of nation’s oil refining industry.

- German FM Schaeuble said the ECB should raise rates ‘sooner rather than later.’ He added that the EMU needs a common economic and finance policy to fix a shortcoming that’s plagued the union from the start.

- Dallas Fed Kaplan has warned against watering down the stress tests on America’s biggest banks, saying it would be hazardous to loosen regulation at a time of soaring asset prices.

- Today’s eco calendar contains German Ifo business sentiment and US durable goods orders. Fed chair Yellen and ECB president Draghi take centre stage at the economic symposium in Jackson Hole.

Currencies: Yellen And Draghi To Decide On Next Directional USD Move

Yellen and Draghi to decide on next USD move

Yesterday, the dollar was little changed against the euro and regained marginally ground against the yen as the impact from Tuesday’s comments of president Trump faded. Investors refrained from placing big bets ahead of today’s Jackson Hole speeches. EUR/USD held near the 1.18 pivot. USD/JPY reversed Wednesday’s Trump-related setback and finished the day at 109.56.

Overnight, most Asian equity markets trade with a positive bias counting down to the speeches of Fed’s Yellen and ECB’s Draghi in Wyoming. The dollar records marginal gains. EUR/USD is changing hands just below 1.18. USD/JPY trades in the 109.60 area. All eyes are on Jackson Hole, but maybe markets are also growing a bit more confident that a US government shutdown can be avoided. This is slightly supportive for risky assets and for the dollar. Japan inflation trended cautiously higher in July (0.5% Y/Y for the measure ex Fresh food). However, the data are no reason to expect a change in BOJ tactics anytime soon.

The eco calendar is interesting today even as main attention will go to central bankers. In Germany the Q2 GDP and the IFO business sentiment will be published. July IFO sentiment was at the highest level since the unification. We don’t predict further gains, but the German August PMI’s showed still progress. In the US, July headline durable orders are expected sharply down after a transportation-induced gain in June. The underlying measures should show a modestly constructive increase. Positive eco data, higher yields and a constructive risk sentiment might be marginally USD supportive. However, the attention will go to Yellen’s speech on financial stability. The start of the tapering of the balance sheet is key, but the Fed’s views on the missing link between a strong labour market and ongoing soft prices are also important. If Yellen suggests asset valuations are high, financial risks might get more weight in policymaking. This would be a signal that the Fed still intends to raise rates manifold. It is a slippery slope though as she need to contain the market reaction too. Regarding the ECB, the outlook for the tapering of APP matters most. Inflation and the strength of the euro are crucial. Both Yellen and Draghi can bring unexpected elements. However, if Yellen gives more weight to risks of financial stability and if Draghi keeps the options open on the timing and the pace of reducing APP, this scenario might be positive for the dollar. Several different combinations can come to the forefront as well.

Broader context and technical picture. Late June, EUR/USD started a new up-leg as investors anticipated a reduction of ECB bond buying. The Fed was expected to remove policy stimulation only in a very gradual way as US inflation remains soft. Uncertainty on the policy of the Trump administration was a secondary negative factor for the dollar. EUR/USD set a new correction top north of 1.19 before consolidating in a narrow 1.1662/1.1910 range. If US data remain ok (as most were this month) and if Draghi gives little information on next ECB steps, there might be room for a modest USD comeback. A return of EUR/USD to the 1.15/16 area is possible. Pockets of US political risk are negative for the dollar.

A downward correction in core yields supported the yen in August. USD/JPY declined from mid-114 mid-July to 108.60. The April correction low (108.13) remains the line in the sand. This level won’t be easy to break as quite some USD bad news is discounted after the recent protracted setback. A cautious buyon- dips approach (with stop-loss protection below 108) may be considered

EUR/USD: awaiting clearer CB guidance

EUR/GBP

EUR/GBP rally slows, at last

The longstanding decline of sterling (against the euro) finally took a breather yesterday. EUR/GBP came slightly off the recent top around 0.9235. Cable returned north of 1.28. The UK data couldn’t explain the pause in the sterling decline, as they disappointed. There was no high profile news from the Brexit negotiations. Immigration data indicated that net migration to the UK fell significantly in the year to March. Whatever, the market apparently found itself a bit too much sterling short and needed a pause. The move was already partially reversed later in the session, indicating that the global picture for sterling didn’t change. EUR/GBP closed the session at 0.9218. Cable finished the day at 1.2801.

There are no important UK data today. Sterling trading will be driven by technical considerations and global factors. If the Jackson Hole speeches result in a rebound of the dollar (Fed giving more weight to financial stability risks), it will evidently also be negative for cable. The impact on EUR/GBP is less clear. A setback in EUR/USD might also inspire some further correction in EUR/GBP. Headlines on Brexit ahead of the next round of negotiations remain a wildcard. Will markets build on yesterday’s ‘correction’ of EUR/GBP?

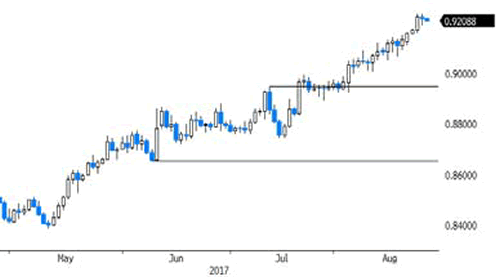

From a technical point of view, EUR/GBP cleared 0.8854/80 resistance (top end June), opening the way for further gains. The move was the result of euro strength (strong EMU data and expectations of APP tapering). Simultaneously, UK price data were soft enough to keep the BoE side-lined as the Brexit negotiations continue. MT, we maintain a buy EUR/GBP on dips approach as we expect the combination of relative euro strength and sterling softness to persist. The 0.9415 ‘flash-crash spike’ is the next target on the charts. However, we don’t jump on the up-trend anymore after the recent rally and wait for a correction, e.g. to the technical support in the 0.88/89 area

EUR/GBP: uptrend slows, at last…?