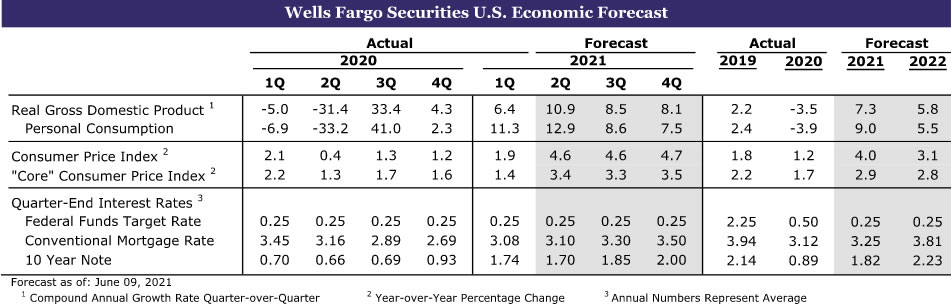

Summary

United States: The Moderation in Home Sales May Hold Some Lessons for the Broader Economy

- Home sales moderated further in May, but home prices continue to rise. The astonishing surge in prices has reduced affordability at a time when supply bottlenecks are limiting new construction.

- Advanced durable goods orders came in slightly below expectations for May, but revisions to the prior month’s data put the level of orders and shipments at or above what had been expected.

- Jobless claims fell slightly in the third week of June, while personal income fell again, as the stimulus payments’ impact unwinds. Wages and salaries rose solidly, while spending was unchanged for the month.

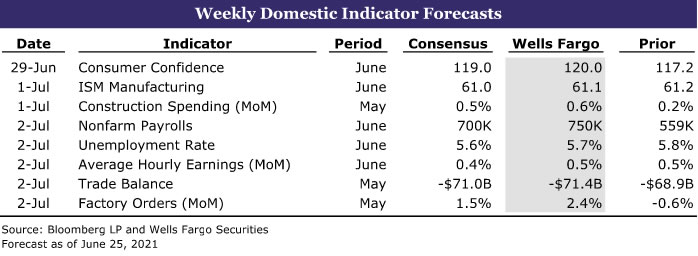

- Next week: Construction spending (Thurs.), ISM Manufacturing (Thurs.), Employment (Fri.)

International: The U.S. Has Led the Recovery, but the Rest of the World Is Starting to Catch Up

- Recent data have offered the clearest signs yet that a more meaningful Eurozone economic upturn is underway.

- Similarly, June PMI data for the United Kingdom were also released this week and reaffirmed that the U.K. is on track for booming economic growth in the summer months.

- Next week: Eurozone CPI (Wed.), Canada April GDP (Wed.), Brazil Industrial Production (Fri.)

Interest Rate Watch: Eventual Tapering to Send Rates Higher, but a Tantrum, à la 2013, Less Likely

- After sharp swings following last week’s FOMC meeting when the committee started “talking about talking about tapering,” the 10-year is back near its pre-meeting yield. When more concrete hints around the timing of tapering are dropped, we expect longer-end yields to move higher, but the reaction is likely to be more modest than in 2013’s “taper tantrum.”

Topic of the Week: Big Investors Move into the Housing Market

- A wide array of large investors, ranging from traditional real estate investment firms to private equity and pension funds, are buying single-family homes and setting up companies to professionally manage them.

U.S. Review

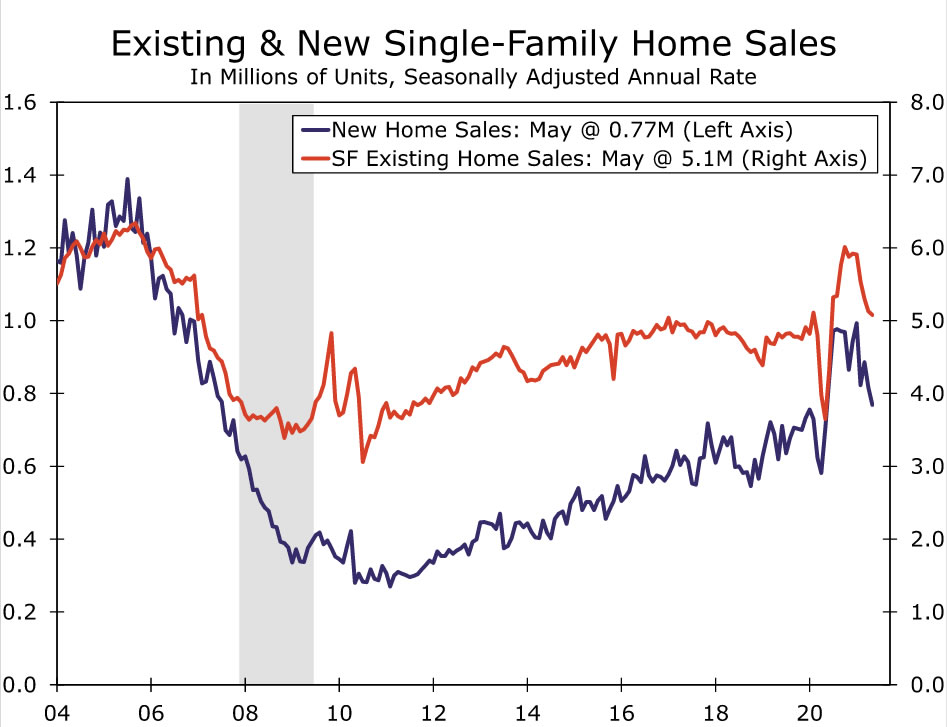

Home Sales Moderate as Pandemic Tailwinds Ease

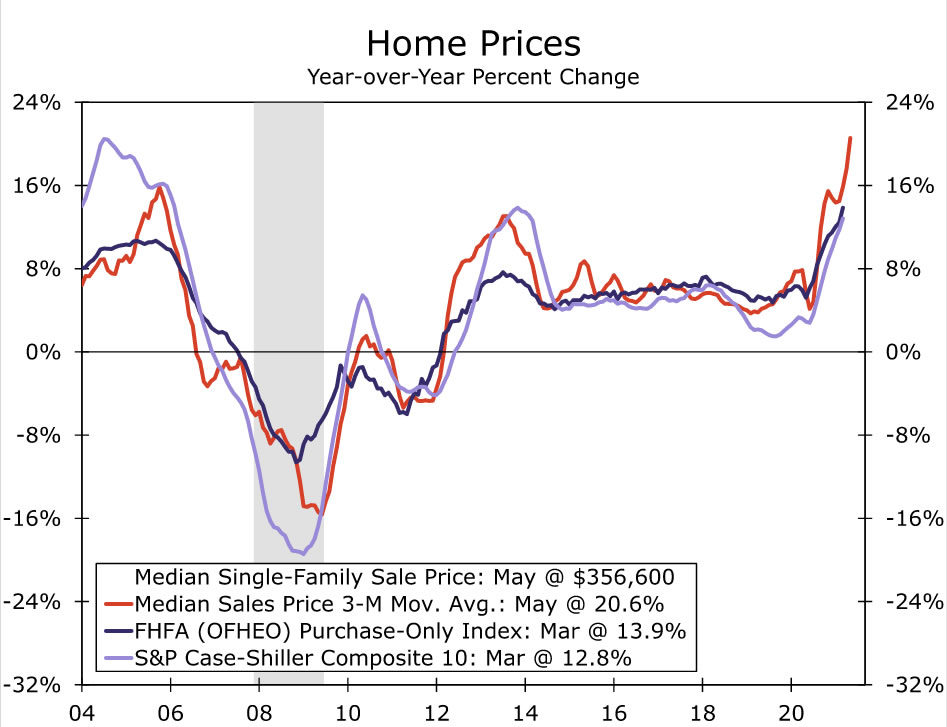

The housing data headlined this week’s light schedule of major economic reports. Sales of both new and existing homes fell in May. Both declines were in line with expectations, which had been tempered by earlier declines in mortgage applications and pending home sales. May’s drop in new home sales was accompanied by downward revisions to sales for each of the prior three months. Even with the pullback, sales are exceptionally strong, with existing home sales falling to a 5.8 million-unit annual pace and new home sales moderating to a 769,000-unit pace. Home prices did not moderate, however, with the median price of an existing single-family home surging a record 24.4% over the past year and the median price of a new home spiking 18.1%.

While buyer traffic has clearly eased, as evidenced by last week’s report from the National Association of Home Builders, we suspect demand has not cooled off all that much. Home builders are still selling homes faster than they can build them, and most have lengthy backlogs. Buyer traffic has clearly slowed, however, particularly in many of what have been the nation’s hottest housing markets. The culprit is likely some combination of the astonishing rise in home prices over the past year, which has curbed affordability, as well as some lessening of the tailwind from buyers seeking trendy locations for remote working. Another factor restraining buyer traffic is that there are not that many homes for home buyers to look through. The number of completed homes available for sale remains near an all-time low, and inventories of existing homes also remain extraordinarily low, with homes typically selling in two weeks or fewer.

Supply chain bottlenecks and price hikes are likely tempering demand somewhat, as consumers pullback from some discretionary purchases. Overall consumer spending was flat during May, and, after factoring in a 0.4% rise in prices, real spending fell 0.4%. Most of the drop was in spending on big-ticket items, such as motor vehicles and household appliances. Inventories of both remain exceptionally lean amid parts shortages, most notably for microchips. Supply-chain bottlenecks for nondurable goods have received attention but are real, nonetheless. The problems are mostly on the logistics end, with shortages of shipping containers, truck drivers and shipping pallets topping the list. Leaner inventories have meant less promotional activity, particularly around holiday weekends, which shows up as higher prices and weaker sales. Shortages of plastic bottles and shipping pallets, for example, mean there were fewer bottles of soda to sell Memorial Day weekend.

Real spending for durable goods tumbled 4.3% in May, while spending on nondurables fell 0.5%. Overall goods purchases fell 2.0% in May, following a 0.4% drop the prior month, but a 9.6% surge in outlays during March will still ensure a healthy gain for goods purchases for the quarter. Another contributor to the shortfall in goods purchases is that spending and services is rebounding as more of the country reopens and more people dine out, attend concerts and sports events, and travel. Spending on services, which accounts for about 60% of overall spending, rose 0.4% in May and is likely headed for a string of solid gains, given recent data on air travel and restaurant dining. Our latest forecast has consumer spending rising at a whopping 12.9% annual rate in Q2, but the latest data suggest there is some slight downside risk to that estimate.

While supply-chain bottlenecks and price spikes might shave a few percentage points off Q2 growth, real GDP is still likely to rise at an extraordinary double-digit, or near double-digit, pace during the quarter. Moreover, there is still plenty of fuel in the tank to support growth during the second half of this year, during which supply-chain concerns are likely to ease somewhat. Wages and salaries rose a solid 0.8% in May, following gains of 1.0% during each of the prior two months. The saving rate fell to 12.4%, but remains more than double its pre-pandemic trend.

Supply-chain bottlenecks remain a challenge, but there are some signs they are beginning to ease a bit. The backlog of ships waiting to get into ports continues to decline, but shipping volumes continue to increase. Rising production is also making an impact and will likely rise further due to the persistence of exceptionally low inventories throughout much of the economy. Once again, the housing sector, which was one of the first areas to demonstrate just how quickly the economy would rebound, is also providing some idea of how and when supply-chain bottlenecks will ease. Lumber prices have tumbled over the past month and are likely to decline further as more supply comes online from the reopening of sawmills around the country and in Canada, as well as increased imports from Scandinavia. Home construction has eased the past few months as builders held off building spec homes and limited sales at many new communities. Construction is set to rise later this year, as a rising proportion of new home sales have been for homes where construction has not yet started, which implies that housing starts will likely rise before home sales rebound.

U.S. Outlook

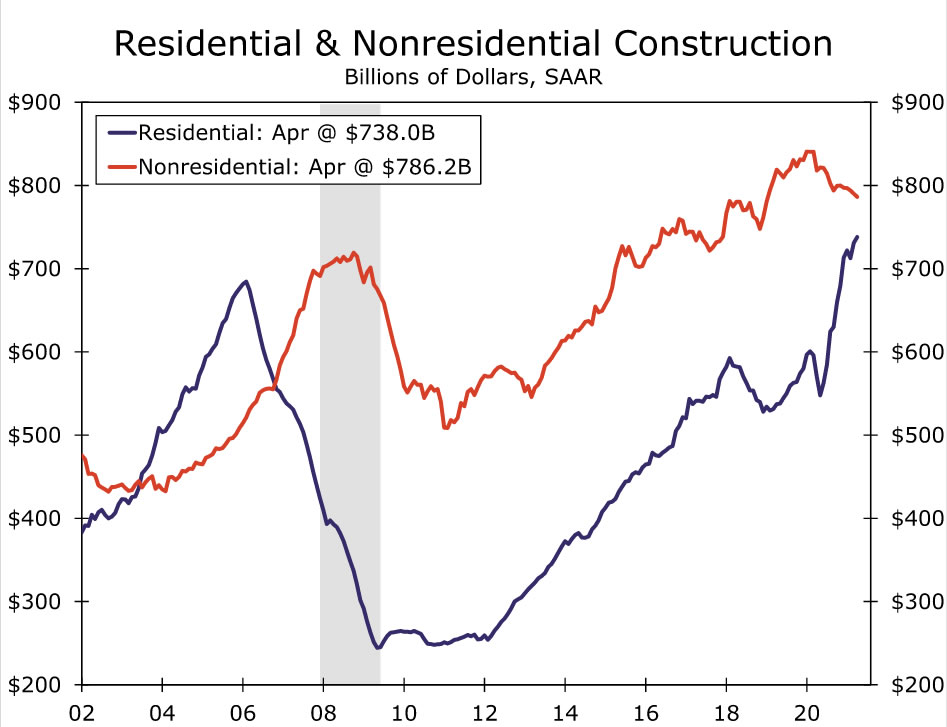

Construction Spending • Thursday

Total construction spending edged up 0.2% in April. Residential spending once again accounted for most of the modest monthly gain as builders rushed to build homes to meet the surge in demand. Meanwhile, the nonresidential sector continues to absorb the aftershocks of the pandemic. Nonresidential outlays slipped during the month, marking the fifth straight decline.

Looking ahead, longer lead times and sharply higher prices for materials stand to be a significant obstacle for construction spending. Still, the recent rise in housing starts suggests residential construction should continue to run at a fairly strong pace. During May, the forward-looking Architecture Billings Index rose to the highest on record, which means nonresidential construction activity is poised for improvement. Overall, we expect total construction spending to climb to 0.6% during May.

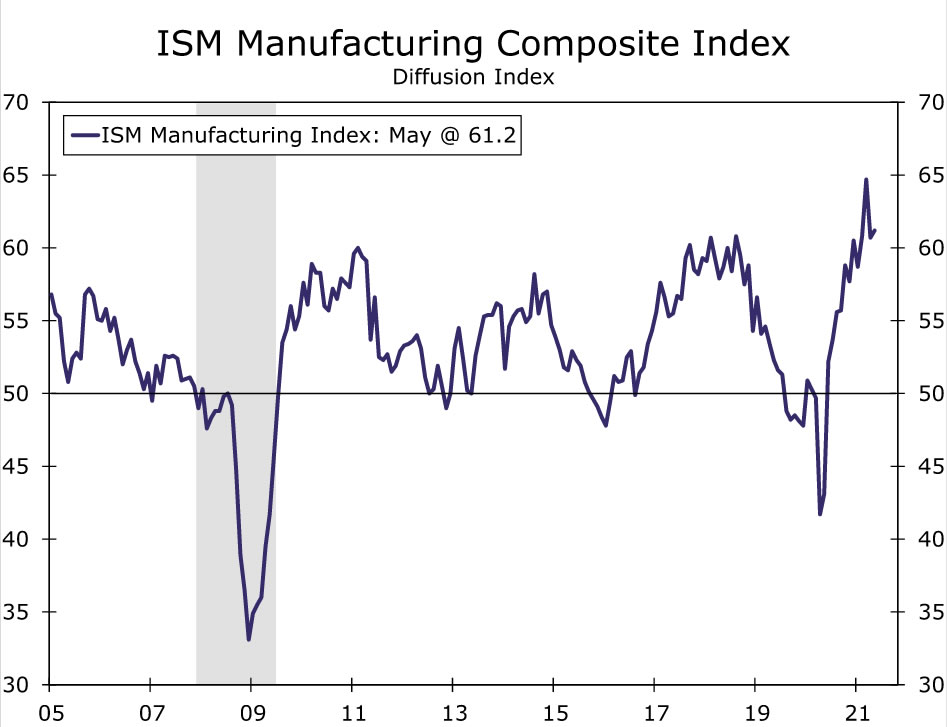

ISM Manufacturing • Thursday

The ISM manufacturing index beat expectations and rose to a reading of 61.2 during May. The supplier deliveries index reached the highest level since 1974 during the month, reflecting the ongoing supply-side constraints many producers are currently experiencing. Not surprisingly, longer wait times are weighing heavily on the production index, which declined to 58.5 from 62.5 the month prior. The prices paid index fell in May, although the index remains elevated.

In addition to raw material shortages, qualified workers are increasingly difficult to find. The hiring index fell by over four points, more than any other sub-component. Many of these supply side constraints will likely continue to be a headwind moving forward. That noted, the new orders index increased solidly during May, meaning producers will likely continue to report strong conditions in the factory sector. The ISM index should remain elevated in June, but we look for a small decline as supply chain dislocations continue to weigh on manufacturing activity.

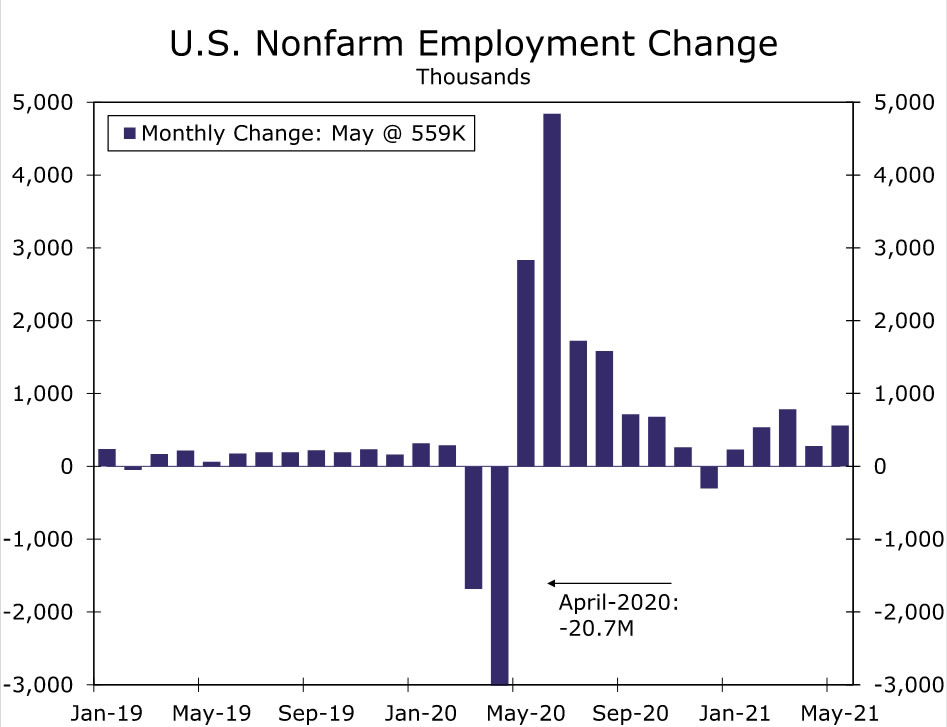

Employment • Friday

Labor scarcities continue to hold back hiring. Employers added 559,000 net new jobs during May, yet for the second month in a row, the monthly gain came in below expectations. The unemployment rate slipped to 5.8% from 6.1% in April, however, the drop was mostly owed to a decline in labor force participation. In an effort to fill open positions, employers continue to raise wages. Average hourly earnings rose 0.5% in May, which pushed the three-month annualized rate up to 4.5%.

In the months ahead, we do not foresee labor shortages being as tight of a constraint on the pace of hiring as they have been recently. Some of the factors which have been a limitation on hiring now appear to be easing. Vaccinations have greatly reduced health concerns related to COVID, and the pace of retirements brought on by the pandemic appears to have slowed. On the other hand, childcare issues remain a hurdle, and none of the 26 states that have announced plans to cut off the extra unemployment payments ended benefits before the payroll survey week. Overall, we expect that hiring picked up further in June and anticipate a 750,000 gain in nonfarm payrolls.

International Review

The U.S. Has Led the Recovery, but the Rest of the World Is Starting to Catch Up

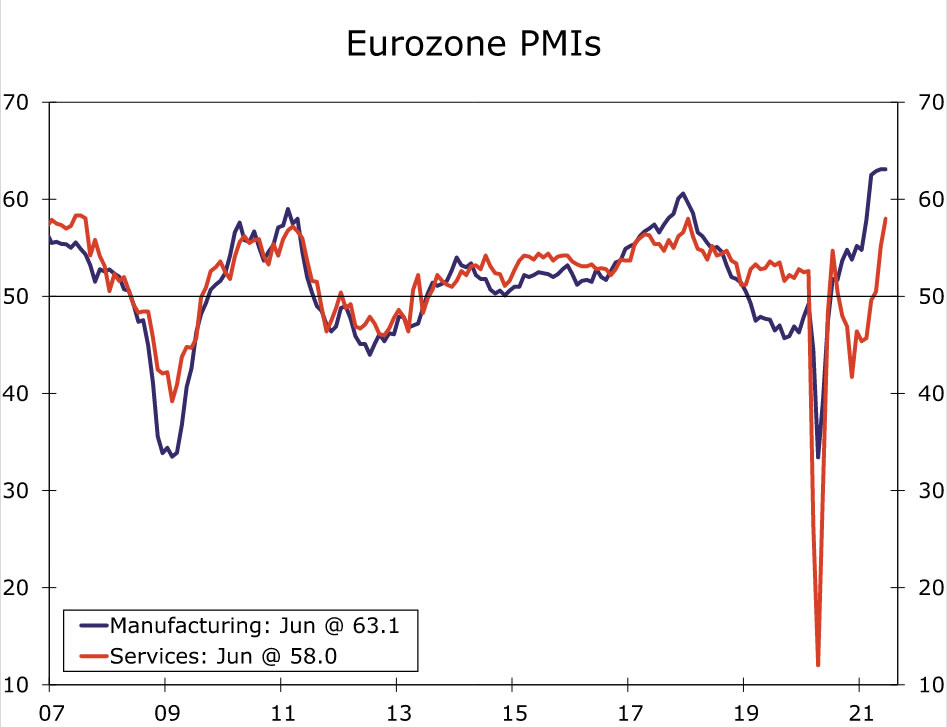

Recent data have offered the clearest signs yet that a more meaningful Eurozone economic upturn is underway. The Eurozone June manufacturing PMI held steady at 63.1 (see chart). Although there was no improvement in the manufacturing index over the month, its abiity to hold steady at May’s all-time high signals that the factory sector is booming in Europe like it is in much of the rest of the world. Perhaps even more important, however, the services PMI rose to 58.0, the highest level since January 2018. The services PMI dipped below the key 50 level in September 2020 and remained in contraction territory until April 2021, when it hit 50.5. May and June have shown much stronger readings and suggest that the service sector is seeing a broader recovery as COVID cases fall, vaccinations rise and government restrictions melt away. We released our latest monthly International Economic Outlook yesterday, and it included an upward revision to our forecast for the Eurozone economy. We now forecast Eurozone GDP to grow 4.3% in 2021 (compared to 3.9% previously), while our GDP growth forecast of 4.2% for 2022 is unchanged.

June PMI data for the United Kingdom were also released this week and reaffirmed that the U.K. is on track for booming economic growth in the summer months. Both the manufacturing and services PMIs fell slightly, but they remained exceptionally high at 64.2 and 61.7, respectively. The composite PMI has now been above 60 for three consecutive months. For some context, its highest reading in all of 2019 was 51.5. When the Bank of England’s (BoE) Monetary Policy Committee met this week, it made no change to monetary policy, but it did revise up its expectations for the level of U.K. GDP in Q2 2021 by about 1.5% relative to what it expected in May. The BoE noted that the recovery in activity has been most pronounced in the consumer-facing services, which loosened restrictions in April. The U.K. government delayed the fourth and final phase of its plan to ease pandemic rules in England by around one month, pushing it to July 19 from the previous June 21 date. Subsequently, Prime Minister Boris Johnson said that the COVID data is looking good for those restrictions to be lifted in July (see chart). Overall, we do not see anything that would alter our outlook for a strong GDP gain for full-year 2021 of 7.0%.

In our updated International Economic Outlook, we left our outlook unchanged for a strong GDP gain for full-year 2021 of 7.0%, and we expect the pound to strengthen against the U.S. dollar over the medium-term. The U.K. may be restrained in the near-term given a brief pause in reopening and mildly unsettled global markets. However, as the U.K.’s steady economic recovery continues and inflation also firms modestly, we expect the Bank of England to continue along its path to less accommodative monetary policy.

In a surprise move, the Central Bank of Mexico raised its official overnight rate 25 basis points to 4.25% on Thursday afternoon. Consensus forecasters, including us, expected the central bank to hold rates steady, although we did expect Mexican policymakers to signal a more hawkish stance on monetary policy. According to the statement, policymakers have become more concerned over the path of inflation, citing more permanent price pressures than initially expected. Supply chain disruptions and higher commodity prices were highlighted as contributing factors to higher inflation, although Banxico also mentioned that a nationwide drought is pushing up prices as well. As of mid-June, bi-weekly CPI inflation topped 6%, well above the central bank’s target of 3% +/- 1%.

The decision to raise interest rates took financial markets by surprise as well. In the immediate aftermath of Banxico’s decision, the Mexican peso rallied and closed over 1.5% stronger against the U.S. dollar. In addition, yields moved sharply higher as Mexican 10-year yields jumped over 10 basis points on the day. While policymakers did not commit to additional interest rate hikes, it is possible that the central bank looks to tighten monetary policy even further, especially if inflation remains above target for an extended period of time. Central bank inflation forecasts have been revised higher recently, and any additional commentary or indications that inflation remains elevated could result in further rate increases in the future.

International Outlook

Eurozone CPI • Wednesday

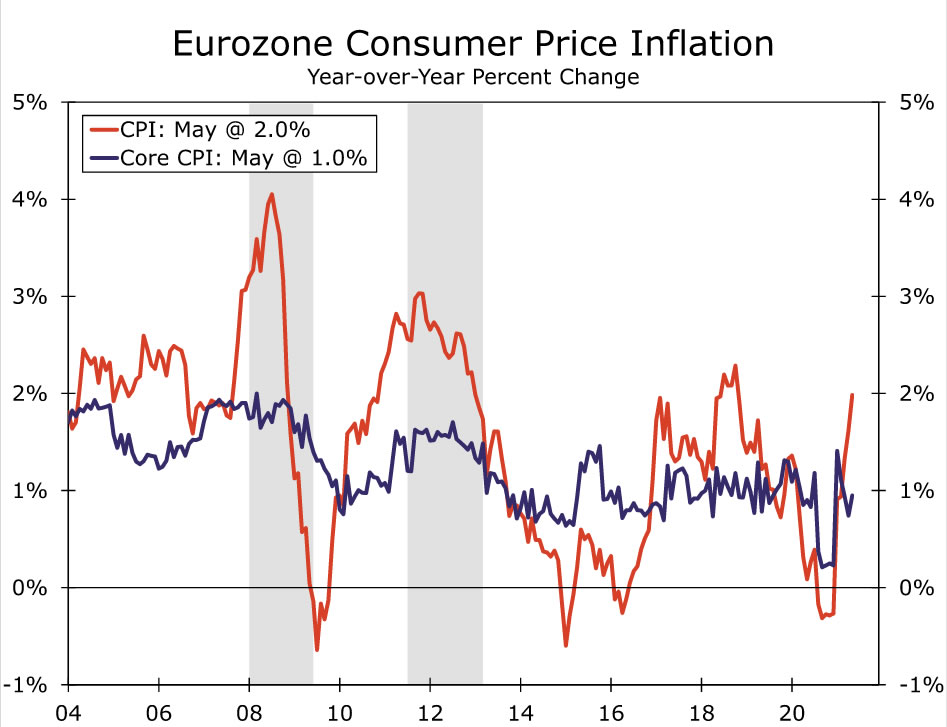

Thus far in 2021, inflation in the Eurozone has not been nearly as hot as it has been in the United States. Headline CPI inflation in the Eurozone was 2.0% in May, and core inflation was just half of that at 1.0%. This slower pace of inflation makes sense given that Europe was generally slower to vaccinate its citizens than the United States, and government restrictions took longer to come off. But does this mean U.S. style inflation is right around the corner for Europe? Next week’s CPI for June will offer an initial look at price pressures as Europe goes through the reopening process.

Prices probably will accelerate in Europe over the next few months, but we doubt inflation will reach U.S. levels. Disinflationary pressures before COVID were stronger in Europe than they were in the United States, and the U.S. fiscal response for households was generally more robust. We project Eurozone CPI inflation in 2021 will average 1.9% for the year. If realized, this would be much faster than the 1.2% seen in 2019, but still well below our 4.0% projection for the United States.

Canada April GDP • Wednesday

Canada’s monthly GDP for April will likely show a contraction in activity amid an increase in COVID cases and government restrictions that were put in place during the month. COVID cases in Canada began to accelerate in late March and did not meaningfully begin to decline until May. Previously released employment data show the Canadian economy shed 207,000 jobs in April and another 68,000 in May.

As a result, Q2 GDP in Canada may be weaker than other economies, such as the United States and Eurozone. We anticipate that this weakness will be short-lived. COVID cases have fallen significantly as vaccinations have become more widespread. Consumer fundamentals remain favorable and should support the economy over time as should elevated commodity prices. With inflation also quickening, the Bank of Canada should continue to taper its bond purchases in the months ahead and start raising interest rates in the latter part of 2022.

Brazil Industrial Production • Friday

The Brazilian economy is in an interesting state. Elevated COVID cases and deaths continue to plague the country, and like many other developing countries, the vaccination campaign has been slow to get off the ground. At the same time, the Brazilian Central Bank (BCB) has been aggressively hiking interest rates. The BCB has hiked its main policy rate 225bps year-to-date, and markets are priced for another 400bps of hikes over the next 12 months. Elevated inflation is playing a major role in the BCB’s decisions to hike interest rates as the CPI is now above 8% on a year-over-year basis.

Nevertheless, current dynamics have made the Brazilian real the top performing emerging market currency this year. Aggressive rate hikes, fiscal and political stability and higher commodity prices have pushed the Brazilian real close to pre-pandemic levels. Industrial production declined by more than 1% in each month from February through April. Next week’s print, which will be for industrial output in May, will show if the Brazilian economy is starting to turn the corner. We expect economic growth to turn positive in Q3, so an inflection point should be near.

Interest Rate Watch

Eventual Tapering to Send Rates Higher, Yes, but a Tantrum, à la 2013, Less Likely

It is easy to consider last week’s FOMC meeting as surprisingly hawkish. The upward shift in the “dot plot” illustrated that Fed officials believe their goals for employment and inflation are likely to be met earlier, leading policy accommodation to be removed somewhat sooner. In addition, Chair Powell made clear the process for eventually scaling back asset purchases got started as they had the “talking about talking about” meeting. Yet, despite the more hawkish tone and the ball starting to at least modestly start moving on tapering, the Treasury market reaction at the long-end of the curve has been rather tame. After some sharp swings in the second half of last week, the yield on the 10-year Treasury is essentially unchanged from its pre-meeting rate on June 15. That stands in sharp contrast to the first 10 days after then-Chair Bernanke first hinted at tapering and the 10-year yield rose 20 bps from May 21-31 in 2013.

Why the apparent calm, at least at the long-end of the curve, when the first whiff of tapering roiled the market in 2013? For one, even though the dot plot signaled somewhat earlier policy tightening, the upward shift puts it more in line with markets. As last week’s meeting kicked off, futures contracts had already priced two hikes by the end of 2023, which is now the median expectation among FOMC members.

At the same time, Powell, and even more hawkish members of the committee, in subsequent public statements, have indicated that the FOMC is only easing into a discussion. It is clear that the committee is not about to make plans, let alone reduce purchases, imminently. The 2013 tantrum looms large in policymakers’ minds. Officials across the spectrum have made clear they will give ample notice in an effort for a smoother tapering process.

We expect that once Powell or the FOMC gives a more concrete hint that tapering is nearing on the horizon, long-end yields will quickly move higher. However, the extent of the increase is likely to be more modest than in 2013. Market participants appear to be more dialed-in to the fact that the Fed eventually will scale back its purchases, having been through quantitative easing before. In addition, the Fed has signaled a lower neutral level of interest rates (known as r*), with the committee’s median estimate of the fed funds rate over the long run declining to 2.5% today from 4.0% in 2013. If the FOMC does not fall behind the curve on inflation this cycle and has estimated r* reasonably well, then presumably, rates would have less road to travel, which would also keep the eventual move higher more modest than in the original “taper tantrum.” It is not that tapering will be a non-event in markets, it is just not likely to be as dramatic as in 2013.

Topic of the Week

Big Investors Move Into the Housing Market

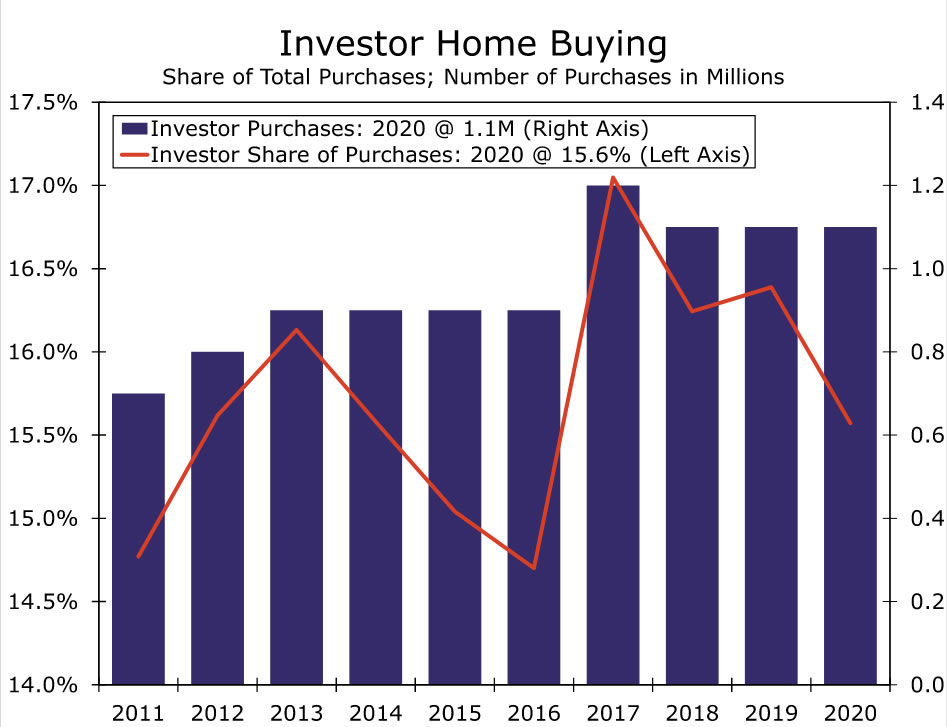

During the worst of the housing bust, famed investor Warren Buffett noted that smart investors would likely raise capital and buy up the then oversupply of homes and convert them to rentals. Once again, Buffett’s comments turned out to be sage advice. A wide array of large investors, ranging from traditional real estate investment firms to private equity and pension funds, soon began buying single-family homes and set up companies to professionally manage them, much like rental apartments. Many home builders also entered the market, developing entire communities for rent and either managing that business themselves or selling the homes to investors. Investors remain enamored with rental housing, as evidenced by Blackstone’s recently announced plan to purchase Home Partners of America, which owns 17,000 houses across the United States. Blackstone had been an early proponent of the single-family rental market (SFR), with its startup Invitation Homes, which was subsequently spun off and is now a publicly-traded company.

The continued influx of institutional capital comes as little surprise, given that robust demand for single-family homes and a paucity of homes available for sale has led to a surge in home prices and higher single-family home rents. According to the CoreLogic, single-family rent growth increased 5.3% in April 2021, the fastest increase since 2006. In addition to low mortgage rates, the pandemic-induced suburban shift and increased need for larger living spaces has pushed buyer demand to heights not seen in more than a decade. Housing supplies, however, remain extremely tight. The lack of homes on the market and increase in buyer demand have caused home values to skyrocket. The rapid run-up in prices now appears to be causing buyers to pull back, especially at the entry-level, where buyers are more sensitive to price changes. Even with some cooling lately, demand for single-family homes remains strong as there is still a massive cohort of Millennials at or near the age when family-forming and home-buying tend to occur. Bearing all this in mind, it makes sense that many priced-out buyers are increasingly turning to single-family rentals.

The inflow of institutional capital into the housing market has raised a few concerns. For one, large investors, who are competing for a relatively small pool of homes, are usually able to make all-cash offers, often well above list price. Some worry that the presence of investors in the bidding process is driving up home prices and making homes even less affordable. The counterargument is that, while investor participation in the housing market has grown over the past few years, investors still only represent a relatively small share of the roughly 90 million homes in the single-family housing market. Moreover, only about 300,000 of the roughly 15 million single-family rental units in the country are owned by large institutional investors. Most of the rest are owned by individual landlords, often referred to as mom-and-pops, which hold much less sway over the market. The bulk of the recent run-up in prices is more likely due to historically low mortgage rates and strong non-investor demand. According to CoreLogic, the number of investor purchases held steady in 2020, while traditional home sales soared to their highest levels since 2006.

Furthermore, investors actually play an important role in the housing market. Investors are more willing to seek out properties in disrepair, leveraging lower financing rates and economies of scale to fix them up at a lower cost in order to rent them out or sell them for a profit. Traditional buyers typically are put-off by fixer-uppers and prefer turn-key homes instead. Single-family rentals serve a useful purpose beyond providing yield for investors. For those who want to reside in a single-family home but do not have savings for a down payment, single-family rentals provide an alternative to homeownership and offer larger living spaces, backyards and greater access to schools and neighborhoods.

{kind=link}