Summary

United States: Summer Hiring Heats Up

- Data this week highlighted the economy’s resilience in the face of ongoing supply constraints, while financial markets weighed the impact of the Delta variant wave on the outlook for the economy and Fed policy. ISM surveys for the manufacturing and service sectors continued to show businesses’ ability to operate in this supply-strained world, with the latter hitting a new record high. Finally, this morning’s virtually blemish-free employment report marked a big step down the road of “substantial further progress.”

- Next week: CPI (Wednesday), U. of Mich. Consumer Sentiment (Friday)

International: China Hit by COVID; Brazilian Central Bank Picks Up Pace of Tightening

- The spread of the Delta variant has hit China, and in response, authorities have reimposed restrictions. Also this week, the Brazilian Central Bank signaled it will become more aggressive in tightening monetary policy as the fight against inflation persists.

- Next week: Mexico CPI (Tuesday), U.K. GDP (Thursday), Central Bank of Turkey (Thursday)

Interest Rate Watch: The Bank of England Turns a Bit More Hawkish

- As widely expected, the Monetary Policy Committee (MPC) at the Bank of England (BoE) left its main policy settings unchanged at its meeting this week, keeping its Bank Rate at 0.10%.

- Credit Market Insights: What Will Happen When Pandemic Emergency Programs End?

- The recent housing market frenzy in the United States, driven by people seeking more space and refinancing in this low mortgage rate environment, led mortgage debt to jump 2.8% to $10.44 trillion in Q2 2021.

Topic of the Week: Red Ink Recedes

- After hitting a budget deficit of $3.1T in FY 2020 due to extensive borrowing and spending measures, the U.S. Treasury is looking to decrease both its borrowing and the federal deficit in the coming months.

U.S. Review

Summer Hiring Heats Up

Data this week highlighted the economy’s resilience in the face of ongoing supply constraints, while financial markets weighed the impact of the Delta variant wave on the outlook for the economy and Fed policy. On Monday, construction spending data for June came in slightly below expectations. Construction spending continued to be held back by outlays on nonresidential projects, reflecting sluggish demand in the most pandemic-afflicted sectors as well as shortages of key materials that are delaying the start of new projects. Home building remained strong, however, rising 1.1% in June, as builders work to restock the country’s depleted inventory of homes for sale.

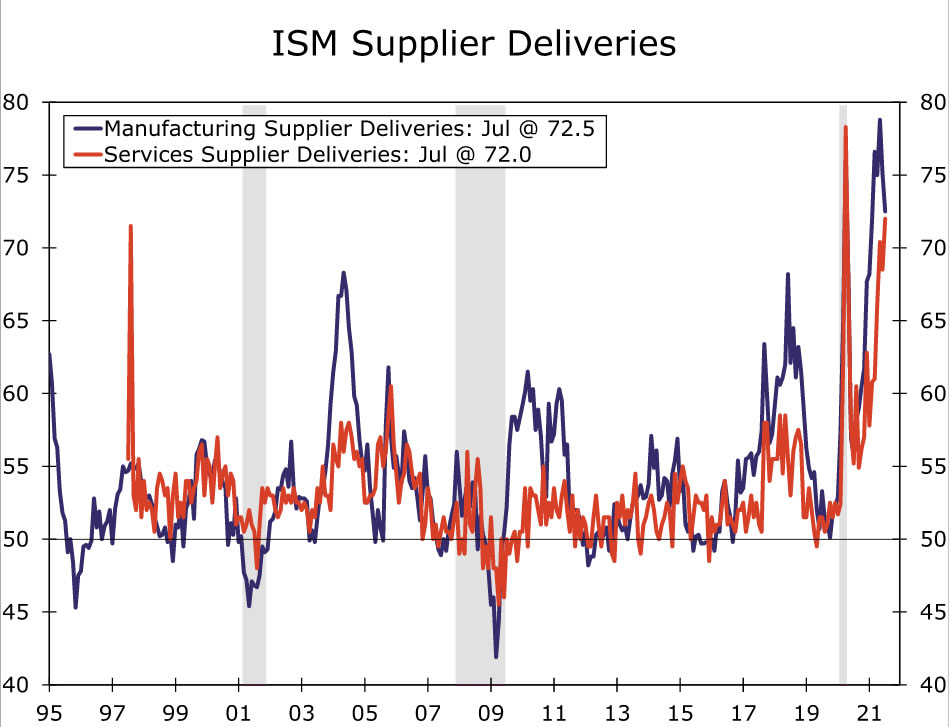

The ISM manufacturing index for July came in slightly below expectations at 59.5, the first sub-60 headline reading since January. Below the headline, there was some indication that supply and demand were coming back into balance. Supplier deliveries fell to a five-month low of 72.5, as the pace of new orders eased 1.1 points, but it is likely too soon to call the end of the supply-chain saga. Meanwhile, activity in the service sector expanded at record breadth in July. Despite their divergence this month, both sectors continue to suggest broad-based expansion, but operating in this environment has not come cheap, and the prices paid sub-index for both sectors remain historically elevated.

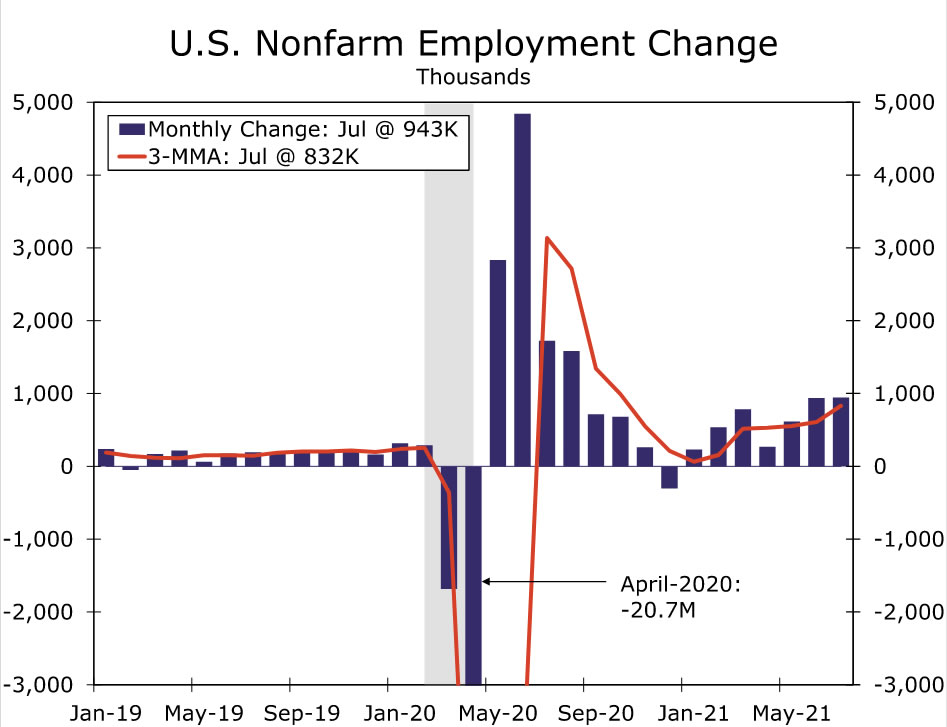

In addition to snarled supply chains and rising material costs, labor supply has been a key obstacle for businesses trying to scale up to meet the rising tide of demand. This morning’s employment report showed that some of these constraints eased in July as employers added 943K net jobs. The strong gain was boosted by a 261K job gain in private and public education payrolls, due to fewer seasonal layoffs, but details elsewhere indicated that the labor market recovery heated up this summer. The reopening was on fully display, as the leisure & hospitality sector added 380K jobs, accounting for more than half of the gain in private sector payrolls. In the household survey, the unemployed rate fell by the most since last October to 5.4%, and the percentage of employed persons who teleworked due to the pandemic dropped to 13.2%, the lowest level since records began last May.

The employment report for July and healthy revisions to prior months marked a strong step toward the Fed’s desire for “substantial further progress,” before it starts tapering its asset purchases. That said, the report is somewhat backward looking. Cases have risen rapidly since the survey week in mid-July. The level of reported new cases now stands above the spring and summer waves of 2020 and is roughly on par with November 2020 before the pandemic’s winter peak in the United States. Thus far, visits to retail and recreation locations and seated diners at restaurants have rolled over only modestly, reflecting a further delay in the return to normal rather than a drop in activity, like what we saw last winter. While Fed officials will certainly be pleased with this morning’s strong report and the lack of a clear reversal in activity measures, we still expect them to wait and see if progress can be sustained and if constraints boil down to short-term frictions or longer-lasting damage before kicking off tapering.

U.S. Outlook

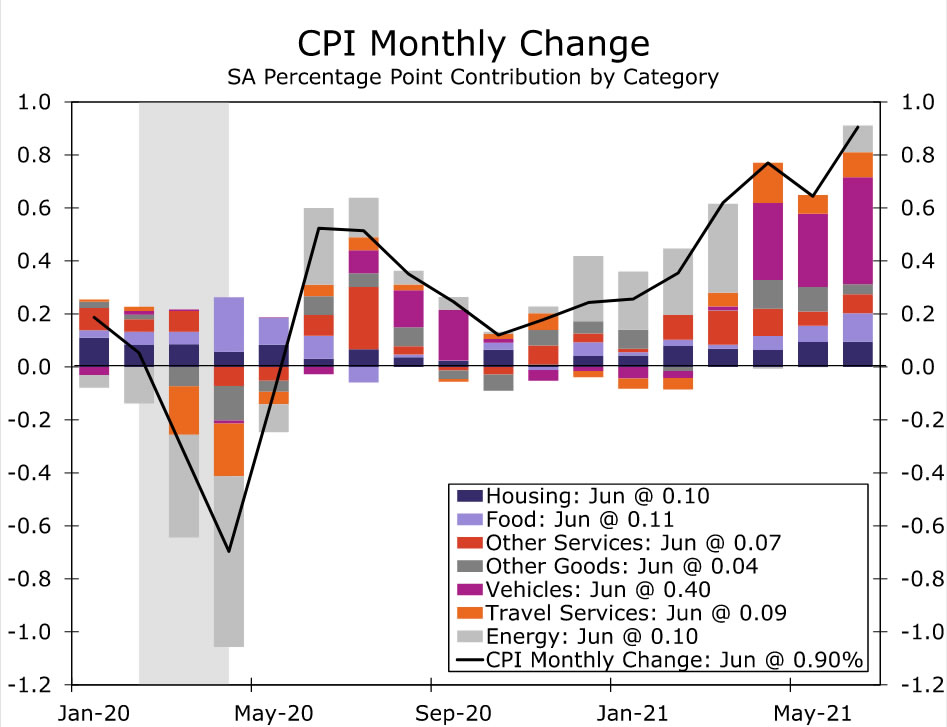

Consumer Price Index (CPI) • Wednesday

We forecast consumer prices advanced another 0.5% in July, which would cause the year-ago rate to slip modestly to 5.3%. Excluding food and energy costs, we suspect the core CPI rose 0.4%.

The underlying details of the report should continue to show price pressure broadening out beyond categories most acutely associated with the reopening. Shelter inflation, for example, likely continued to rise in June and will be a source of upward pressure on prices for some time to come as the run-up in home prices over the past year filters into the CPI and rents are quickly bouncing back. Similarly, food prices were still poised for some considerable strength in July based on the recent run up in food-related commodity prices and average hourly earnings at restaurants.

We suspect persistent supply problems across a number of sectors also kept the heat turned up on prices of particular categories, as did the fact that businesses have continued to struggle to meet surging demand. Categories like travel services and apparel may still have had some scope for a pickup in prices last month. But price gains may soon become more challenging to the extent that the Delta variant dampens near-term demand and the effects from the reopening begin to fade.

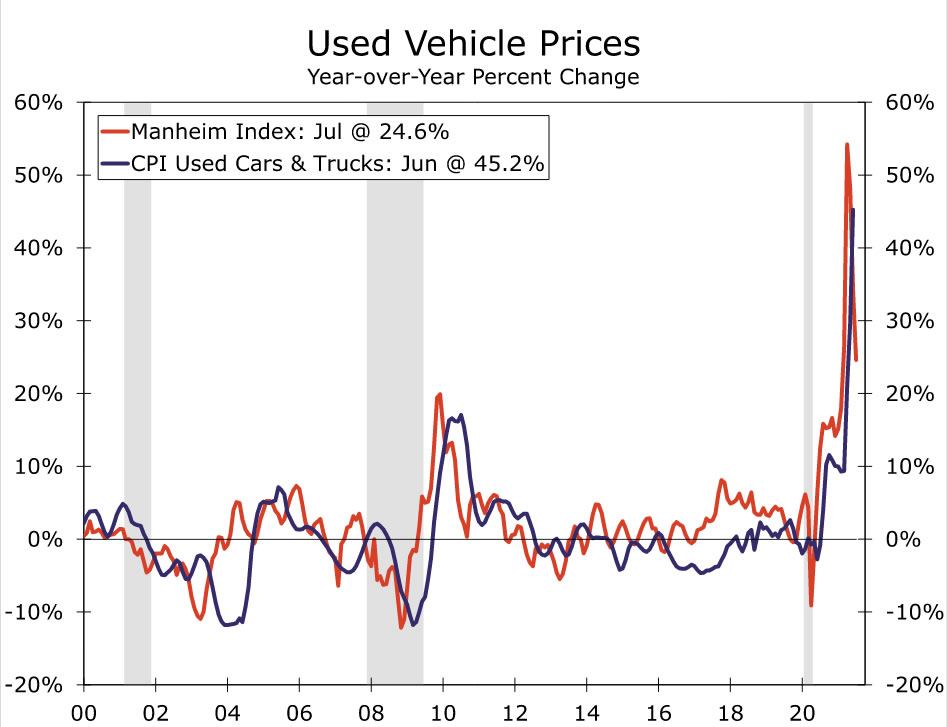

For used autos, some payback could begin as early as the July reading. Wholesale used auto auction prices measured by the Manheim index and prices in the CPI are more in alignment now (see chart), and with auction prices declining the past two months, it seems that the rise in used car prices is close to running its course. We look for declines in this segment over the next few months, potentially beginning in July, which would weigh on the overall CPI after supporting the monthly gain in prices in recent months.

If the July inflation data come in a tenth or so in either direction of our forecast, we do not think it will overly concern the Fed. The Fed believes the current degree of inflation to be transitory, which means it’ll continue to wait for inflation to settle prior to taking too much stock in what the current data is showing.

While the Fed is effectively calling for an eventual slowdown in the pace of inflation rather than a reversal in the price level, we see a number of categories where the price level seems ripe for reversal. This suggests inflation could slow markedly by the middle of next year, following sharp gains in categories where prices were already well-above their pre-COVID trend, such as used autos and car rentals. The overall rate of inflation may therefore temporarily fall below what will eventually be its post-COVID trend, keeping the inflation picture for the Fed unsettled for a while yet.

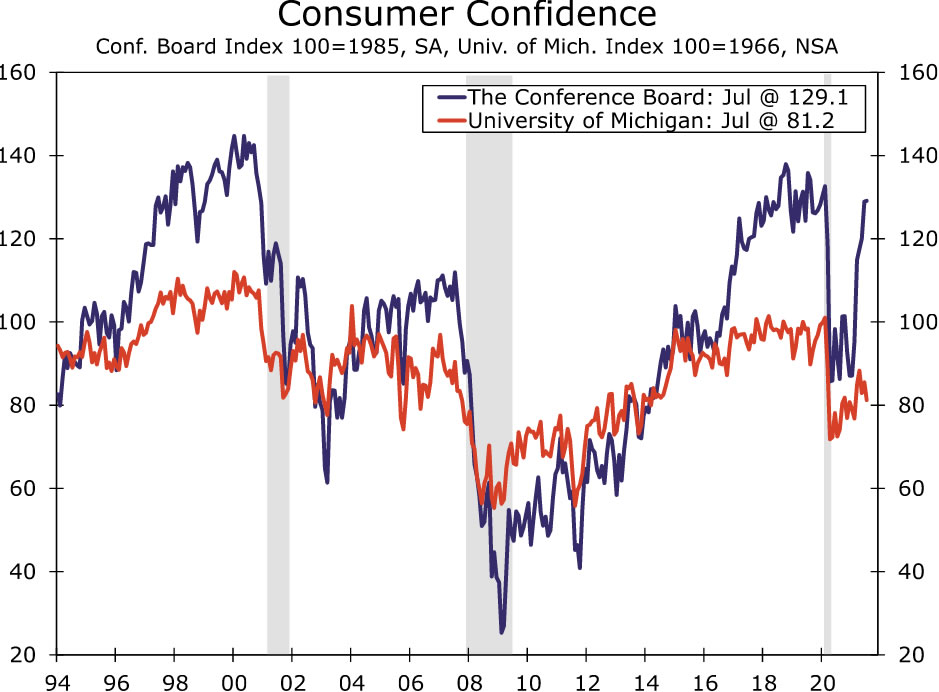

Michigan Consumer Sentiment • Friday

July’s confidence data were mixed. Despite widespread expectations that inflation and a resurgence in COVID cases would weigh on sentiment, the Conference Board’s measure of consumer confidence rose in July to its highest level of the post-pandemic era. That was at odds with the University of Michigan’s Consumer Sentiment survey, which showed inflation fears pulling the measure lower in July.

There have been mixed signals from the consumer side of the economy. The hard data have generally exceeded expectations, with the 11.8% annualized growth rate for second quarter consumer spending being one of the few bright spots in an otherwise underwhelming GDP report. The ISM services component for July released earlier this week was the highest figure on record and signals the services economy was chugging along at full steam in July.

Next Friday will bring with it the first look at August sentiment and will serve as an indication of how consumer psyches are holding up amid the latest flare up in COVID cases and persistently high inflation.

International Review

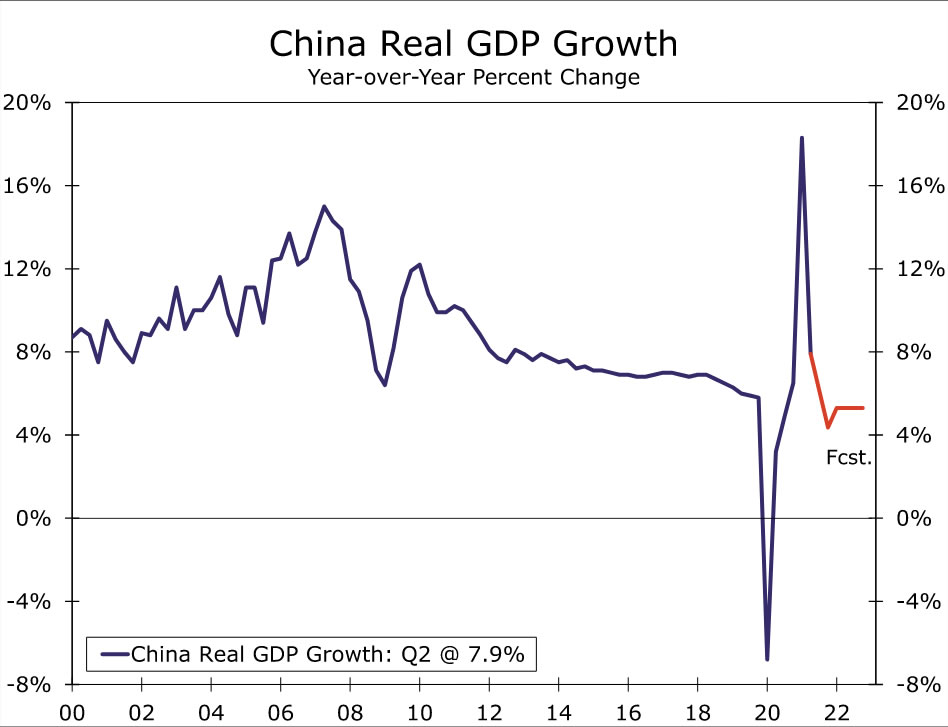

Renewed Pressure on China’s Economy

We have revised our annual 2021 GDP growth forecast for China’s economy lower over the past few months, and recent developments will likely result in another downward revision in the near future. Multiple factors are at play in considering another downward GDP revision, most notably a COVID outbreak and harsh restrictions being put back in place. In addition, a nationwide flood has damaged some output potential, while a regulatory crackdown on certain sectors could also lead to reduced portfolio and capital flows into China. As far as COVID infections, case numbers have spiked to levels with which Chinese authorities are uncomfortable. Local travel restrictions, including public transportation, have been shuttered in the hardest-hit areas, while quarantine requirements are back in place for foreign travelers. Business-related travel and other non-essential trips have been canceled, with reports suggesting airline capacity has been reduced for many local providers. In addition, mass testing will occur in Wuhan, the origin city of the virus.

New restrictions are likely to have an impact on consumer activity nationwide. China’s service sector, more formally known as the Tertiary Industry, and of which retail trade is a significant influence, accounts for close to 60% of China’s economy. A major slowdown in retail activity could have a relatively large impact on the overall economy. On the other hand, given the renewed global spread of the Delta variant, China’s export sector could slow as global demand dips. The timeframe around new restrictions is unclear; however, we believe there will be economic implications for Q3 GDP growth. On a quarterly basis, Q3 GDP may slow in line with how the economy performed in Q1-2021, growth of just 0.40%, when China also responded to a COVID outbreak with restrictions. For now, we forecast Q3-2021 GDP growth of 1.3% on a sequential basis; however, given the COVID-related risks, we will likely make downward revisions to our Q3 growth forecast and will formally make adjustments in our monthly update.

Brazilian Central Bank Tightening Quicker

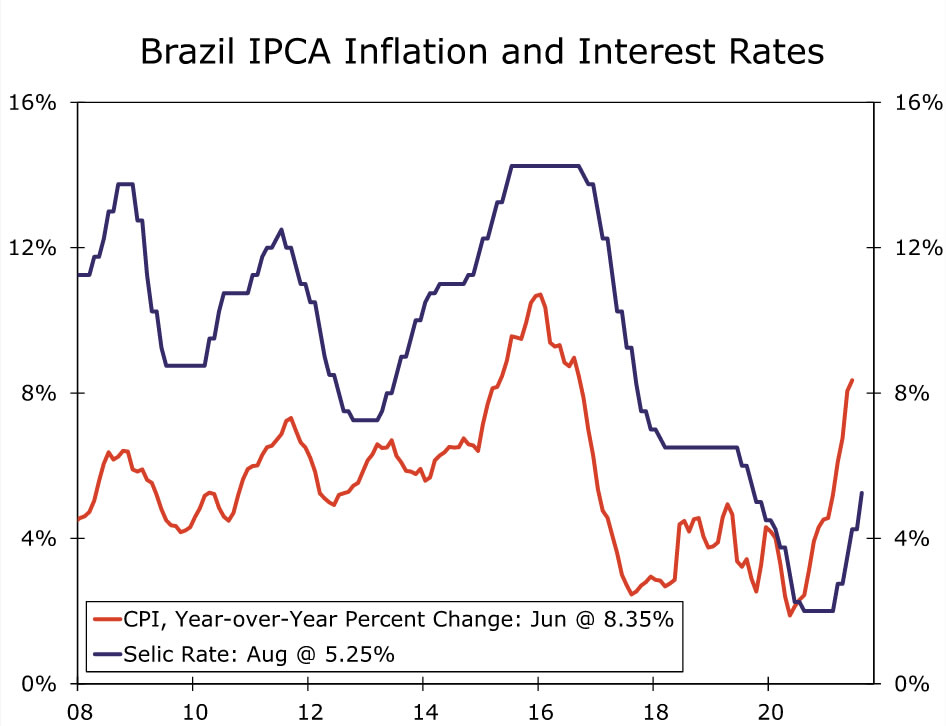

The Brazilian Central Bank (BCB) maintained its place as one of the most hawkish central banks in the world this week. At its latest meeting, BCB policymakers opted to raise its Selic Rate 100 bps, lifting the main interest rate to 5.25%. While the hike was not a surprise, the official statement and accompanying hawkish language was more of a shock as the BCB signaled a more aggressive pace of monetary tightening in an effort to contain inflation. To that point, the BCB told markets another 100-bp interest rate is likely at its next meeting, and policy rates would be lifted above “neutral” by the end of this year. Estimates of “neutral interest rates” are between 6% to 7%, which means the Selic Rate could be lifted another 200 bps before the end of 2021.

More hawkish guidance from the Brazilian policymakers will likely lead to adjustments in our Selic rate forecasts in the near future. Inflation is expected to hit close to 9% in July, well above the central bank’s target range, while policymakers also cited fiscal stimulus risk could result in a deteriorating inflation outlook. The proactive stance of the BCB should be a welcome development and enhance the credibility of Brazil’s central bank; however, we note that tighter monetary policy may not be all that effective against fiscal stimulus, the reopening of Brazil’s economy and even higher commodity prices. In addition, Brazil has experienced weather-related developments such as extreme drought and even freezing temperatures that complicate the domestic inflation outlook as well. Despite these external developments, we believe policy rates will continue to rise over the remainder of the year, likely to reach at least 7% over the next few months.

International Outlook

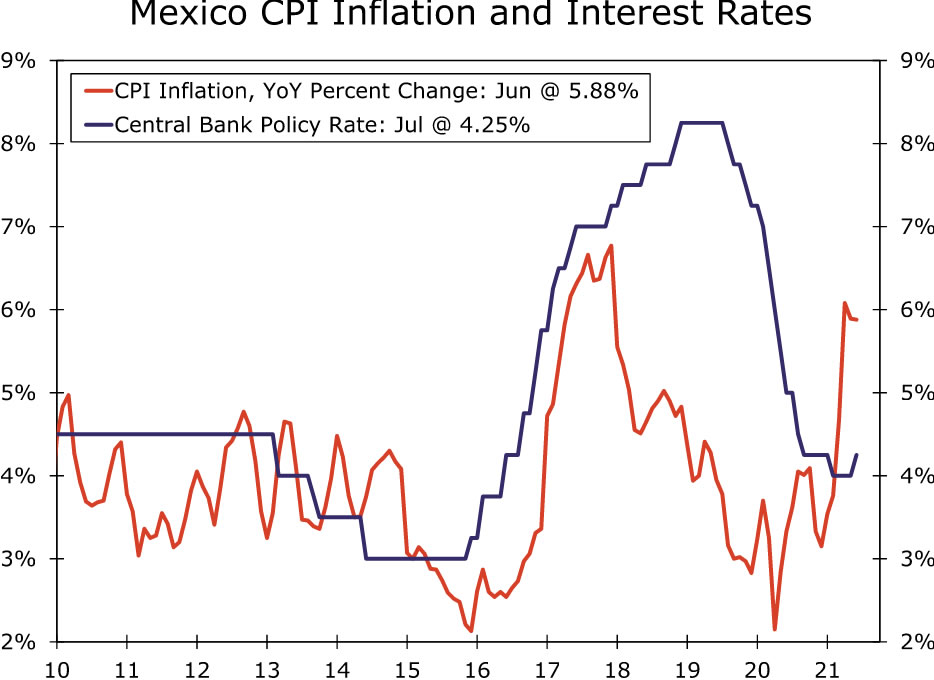

Mexico Inflation • Tuesday

Inflation in Mexico is proving to be stickier than policymakers initially expected, with June inflation still well above the central bank’s target. Elevated commodity prices, supply chain disruptions and weather-related impacts have all played a role in pushing the CPI higher; however, policymakers may have also underestimated the effects reopening the economy could have on prices. During the past few monetary policy meetings, Mexican policymakers have also cited inflation as being higher than they expected and as rationale for a surprise 25-bp rate hike not long ago.

Next week, July inflation data will be released, and prices are likely to remain above target for at least another month, likely longer. In that sense, financial markets have priced more aggressive monetary tightening from the central bank as market participants believe policymakers will need to turn more proactive to contain inflation. We have also adjusted our policy rate forecast as well, and now believe policy rates will be lifted at least another 50 bps before the end of this year. Should inflation continue to rise, policymakers may turn even more hawkish than we expect over time.

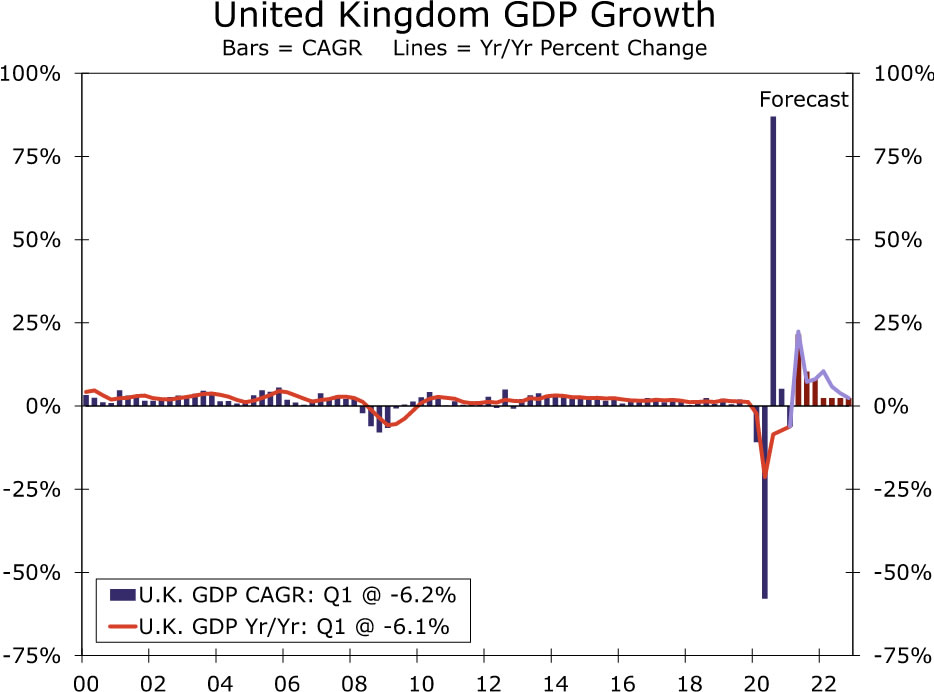

U.K. Q2 GDP • Thursday

Economic activity in the United Kingdom, for the most part, has held up well over the past few months. Early this year, the economy came under modest pressure as a spike in COVID cases tied to the Delta variant delayed the reopening; however, with restrictions lifted, the outlook remains bright. Next week, Q2 GDP data should reflect momentum building within the economy, particularly as it relates to consumer spending. Household balance sheet data in the U.K. suggest consumers have plenty of cash ready to deploy, which should support the economy going forward.

In our view, we expect the U.K. economy to grow 5% on a quarter-over-quarter basis, 21.6% quarterly annualized. Growth in this range would be one of the strongest quarterly growth figures on record in the U.K. Given the full reopening of the economy and consumers flush with cash, we expect consumption to be the key driver of the economy in Q2 as well as in future quarters. Strong GDP data should also support our view for further Bank of England monetary tightening over time, especially if strong GDP data are matched with elevated inflation prints in the coming months.

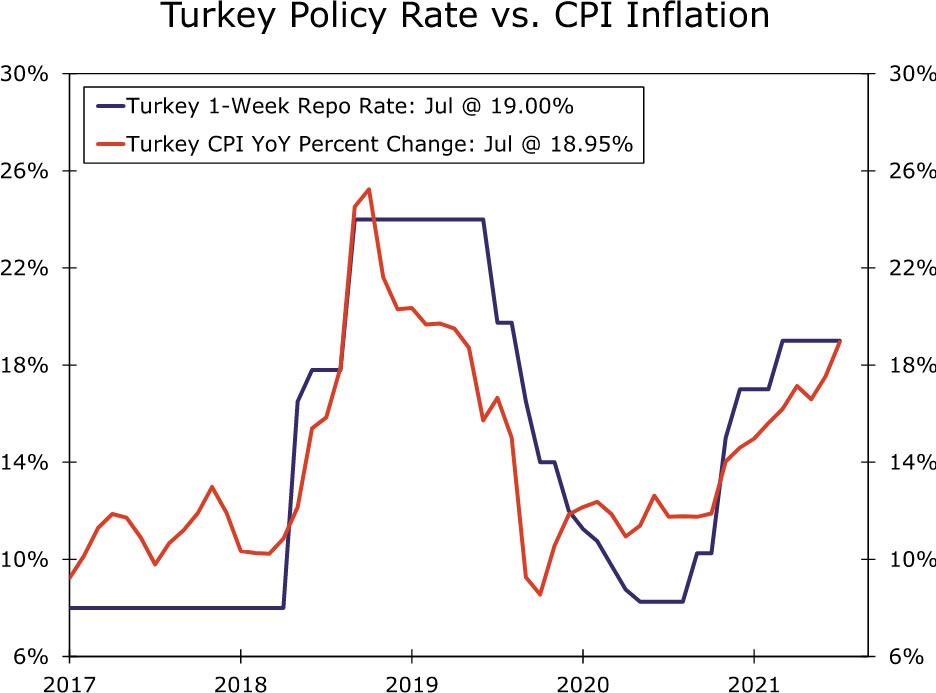

Central Bank of Turkey • Thursday

The unpredictability of monetary policy in Turkey always makes for interesting rate decisions. To that point, the Turkish Monetary Policy Committee will meet next week to decide on interest rates amid another sharp rise in inflation and heightened rhetoric from President Erdogan. While we expect interest rates to be held steady next week, President Erdogan has recently become more outspoken regarding his views on monetary policy and the path for policy rates. Historically, President Erdogan’s monetary policy rhetoric has resulted in elevated currency volatility or a reshuffle of central bank policymakers. Since March, central bank officials have remained in office, and the currency has been somewhat stable; however, we would not be surprised if another bout of volatility hit the lira in the near future.

Rising inflation has typically been coupled with Erdogan calling for interest rate cuts, an unorthodox view. Should rates be left on hold and inflation continue to rise, Erdogan could become more aggressive and possibly look to replace central bankers with a team more likely to implement his views. Should this scenario unfold, we would expect another large depreciation in the lira and for inflation to continue to trend higher over time.

Interest Rate Watch

The Bank of England Turns a Bit More Hawkish

As widely expected, the Monetary Policy Committee (MPC) at the Bank of England (BoE) left its main policy settings unchanged at its meeting this week. The MPC voted unanimously to keep its Bank Rate at 0.10%, where it has been since March 2020, and it reaffirmed its commitment to purchase up to £875 billion worth of government bonds and £20 billion worth of corporate bonds. At the current rates of purchase, these targets should be met in December.

But, the MPC also said some modest tightening of monetary policy over its forecast period, which goes through mid-2024, is likely to be necessary if the economy evolves in line with its projections. In that regard, the BoE revised its forecast for real GDP growth in 2022 to 6% from the 5.75% rate that it had forecasted in its last Monetary Policy Report in May. It also expects that CPI inflation will jump to 4% by Q4-2021, which is a sharp upward revision from its projection in May, although the BoE still suspects that the spike in inflation will largely prove to be transitory. In addition, policymakers indicated that the threshold for unwinding the BoE’s quantitative easing purchases was lower than previously. That is, the MPC previously had said that its Bank Rate would need to rise to 1.50% before it would stop re-investing the proceeds from its portfolio holdings that had matured. That new threshold is now 0.50% “if appropriate given the economic circumstances.” In short, it appears that the MPC may start removing monetary accommodation a bit earlier than we had previously anticipated.

Given the MPC’s new guidance, we have made some modest revisions to our forecast. Previously, we had looked for MPC tightening to begin in early 2023, but we now look for the first rate hike to occur in Q3-2022. That said, we think that the initial rate hike will only be 15 bps, which would take the Bank Rate to 0.25%. Although our current forecast officially ends in Q4-2022, we think there is a reasonable chance that the MPC could sanction another 50 bps or 75 bps of further rate hikes over the course of 2023.

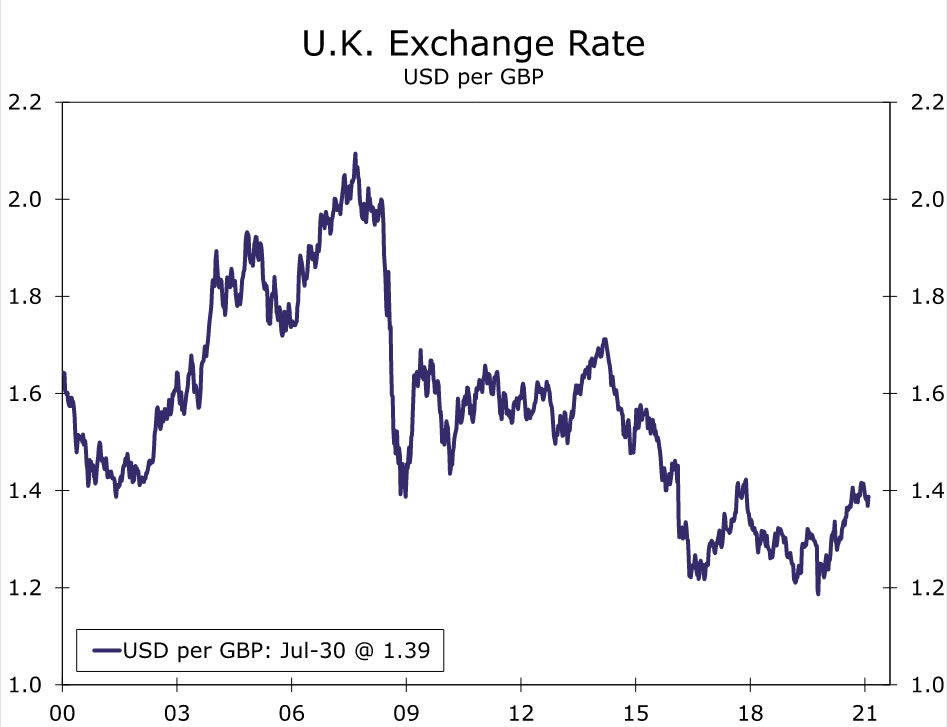

The British pound, which has traded in a 5% range versus the U.S. dollar since the beginning of the year, ticked up versus the greenback on the heels of the announcement (see chart). Looking forward, we expect sterling to remain largely within its year-to-date range through the end of 2021 as market participants continue to digest incoming data regarding the U.S. and U.K. economies. However, we look for the British pound to move higher against the U.S. dollar next year as expectations of BoE monetary tightening begin to ramp up.

For further reading on the MPC’s announcement this week see “Bank of England’s Subdued Signal of Future Tightening.” See our International Economic Outlook for further reading on our sterling forecast.

Credit Market Insights

What Will Happen When Pandemic Emergency Programs End?

Mortgage debt jumped 2.8% to $10.44 trillion in Q2-2021 from $10.16 trillion last quarter, as rising home prices have pushed up the size of new home loans and homeowners have refinanced to take advantage of the summer downturn in mortgage rates. This increase in mortgage balances was the primary contributor to overall household debt rising 2.1% in Q2, the largest increase since 2013, to almost $15 trillion. Auto loans and credit card borrowing were also up from the previous quarter, increasing by 2.4% and 2.2%, respectively.

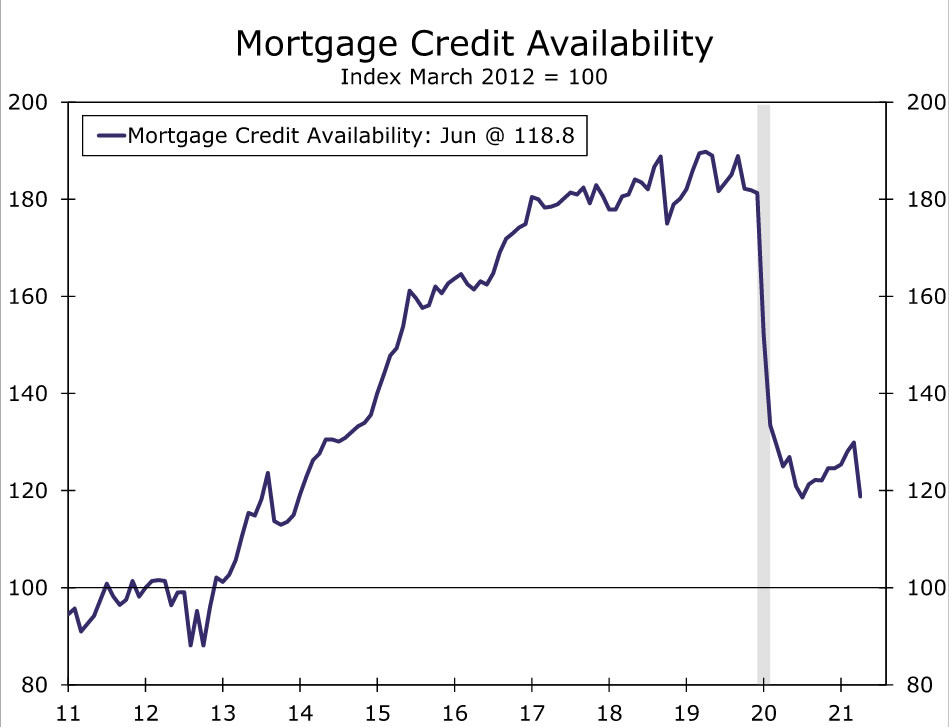

The level of mortgage debt is increasing, despite lending standards remaining tight. The mortgage credit availability index is still well below where it was pre-pandemic, according to the Mortgage Bankers Association. In addition, more than 70% of mortgage originations went to people with a credit score over 760 in Q2, near the record high of 73% set last quarter. However, according to the Fed’s Senior Loan Officer Opinion Survey, a net share of banks reported loosening lending standards for auto loans and credit card borrowing in Q2.

Unemployment benefits, stimulus checks and loan forbearance have all helped people stay on top of their debt during the lingering pandemic. Only 5.7% of student debt is 90 days plus delinquent currently, compared to 11% pre-pandemic, and the share of mortgages becoming delinquent fell to 0.4%, a record low. In addition, the national forbearance rate, excluding forbearances due to the storms in Texas and Oklahoma, is trending downward with just 2.7% of mortgages in forbearance at the end of Q2. But, even though only 18% of mortgage holders are subprime, they make up a significant portion of mortgage borrowers in forbearance; 39% of borrowers in forbearance have a credit score lower than 620 versus 26% a year ago. The question of what will happen to these borrowers when forbearances end remains.

With most active forbearances ending this September and October, according to Black Knight, and unemployment benefits, the freeze on student loan repayments and the ban on evictions all expiring soon, delinquencies on debt could increase. With the Delta variant emerging, the robust pace of job and income growth could slow. That said, we do not anticipate a surge in foreclosures over the coming months. Many borrowers and loan officers will likely enter repayment plans once forbearances expire and, more broadly, we believe the economic recovery will remain intact despite the recent uptick in cases.

Topic of the Week

Red Ink Recedes

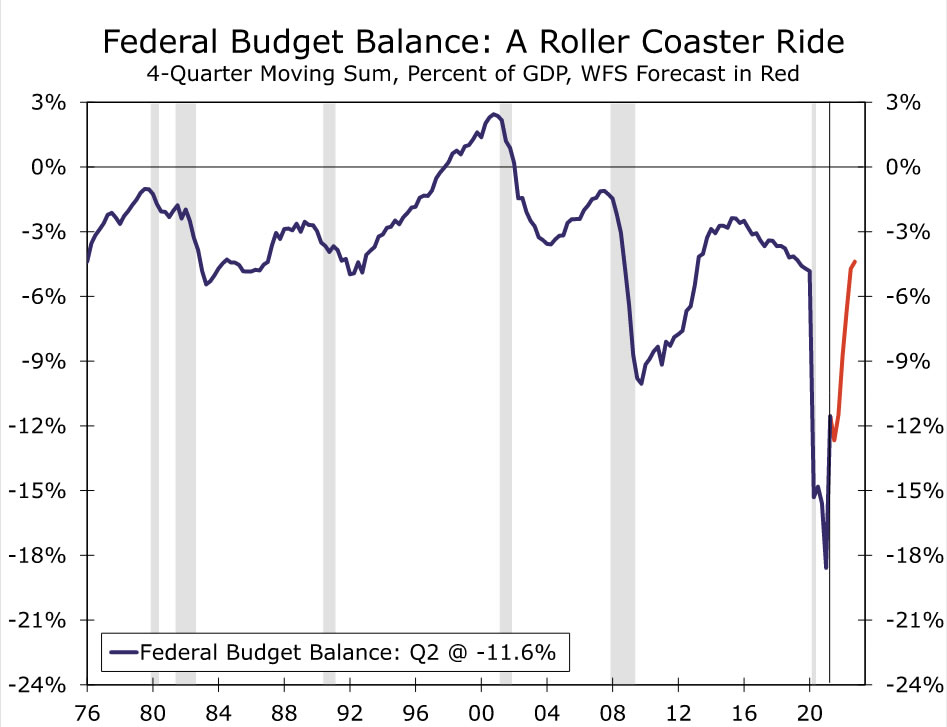

Since the COVID pandemic began, the federal budget deficit has widened significantly amid the sharp contraction in economic activity and the slew of measures adopted to provide financial relief to households, businesses and state and local governments. The federal budget deficit was about $3.1 trillion in FY 2020 and will likely be about $3 trillion when FY 2021 ends on September 30.

As the eventual tapering of the Federal Reserve’s asset purchase program draws nearer, some market participants are concerned about the supply and demand dynamics of the Treasury market. The Fed is currently buying $80 billion worth of Treasury securities and $40 billion worth of mortgage-backed securities per month. As of July 28, the Federal Reserve holds $5.3 trillion of Treasury securities, roughly half of which were purchased since the pandemic began. Currently, we expect the Federal Open Market Committee (FOMC) to announce a tapering of its asset purchases at its December meeting. Our expectation is that the Fed will begin to taper its purchases of Treasury securities and mortgage-backed securities by $10 billion and $5 billion, respectively, per FOMC meeting, in 2022. Will the Treasury market be disrupted by its largest buyer stepping away?

For the most part, we suspect the answer is no, as slowing Federal Reserve asset purchases should be mitigated by a sizable reduction in the federal budget deficit. The U.S. economy has strengthened significantly in recent months, and we anticipate further progress in the months ahead. This should boost tax collections on the revenue side of the ledger. And on the spending side of the ledger, most COVID relief money has been dispersed. Some money is still trickling out in the form of state and local relief, aid to renters, child tax credit payments and enhanced unemployment benefits, but by 2022, these payments largely should have ended as well.

Accordingly, our forecast for the FY 2022 budget deficit is $1.2 trillion, which is about $1.8 trillion smaller than our projected deficit for FY 2021. Smaller budget deficits should mean less debt issuance by the federal government, and the U.S. Treasury signaled as much in its quarterly refunding statement released this week. The Treasury signaled that reductions to its debt issuance schedule are likely later this year and into 2022, as its borrowing needs lessen. More specifically, we are looking for across-the-board reductions to all nominal coupon auction sizes starting in November 2021, with particularly large reductions in both the seven-year and 20-year Treasury securities. T-bills outstanding will also likely continue to contract in the quarters ahead.

Our FY 2022 budget deficit does not assume any major policy changes on the fiscal front, and as a result, we believe the risks are skewed toward larger rather than smaller deficits. However, even if Congress enacts $2 trillion-$3 trillion of new spending on infrastructure and social welfare programs, this money would likely be spread out over an entire decade. Contrast that with the nearly $2 trillion American Rescue Plan (ARP) enacted in mid-March. In that bill, nearly all the money would be sent out within the first year of enactment, which concentrates the deficit/borrowing impact into a much tighter window. Furthermore, we suspect tax increases would finance at least some of this new spending, another divergence from the ARP. Thus, even if major tax and spend policy changes are on the horizon, we suspect they would “only” add a few hundred billion dollars to next year’s deficit, which would still imply a sharp narrowing in the FY 2022 budget deficit compared to FY 2021.

{kind=link}