Sunrise Market Commentary

- Rates: Technical features vs. risk sentiment and Fed Brainard

Last week’s bearish engulfing pattern in the US Note future (potential trend reversal) needs confirmation this week. The technical picture, which argues in favour of a correction lower, hangs in the balance with risk sentiment (several potential negatives) and a (dovish?) speech by Fed governor Brainard. - Currencies: Korean tensions keep dollar near recent lows

The dollar traded slightly softer in thin market conditions yesterday. The US currency underperformed the yen and even the euro, as Korean uncertainty weighs. This pattern might continue today even as the eco calendar is better filled. More consolidation in EUR/USD and EUR/GBP might be on the cards going into Thursday’s ECB meeting.

The Sunrise Headlines

- US markets return after yesterday’s Labour Day Holiday. Risk sentiment on Asian stock markets is mixed overnight with Japan underperforming (stronger yen). The US Note future gains modest ground.

- China’s services sector expanded at a faster clip in August as new business orders picked up, according to the Caixin Services PMI, pointing to renewed strength in a key part of the world’s second-largest economy.

- South Korea warned that North Korea appears to be preparing to test another intercontinental ballistic missile, and the US told the UN that the regime is “begging for war” after Pyongyang set off its most powerful nuclear bomb yet.

- The RBA kept its policy rate unchanged at 1.5%, remaining on the side-lines as lending curbs take steam out of housing markets in Sydney/Melbourne and as prospects for a pickup in business investment emerge. AUD/USD barely moves.

- Officials across the north eastern Caribbean cancelled airline flights, shuttered schools and urged people to hunker down indoors as Hurricane Irma barrelled toward the region as a powerful Category 4 storm expected to strengthen more before nearing land late Tuesday.

- The number of European banks in grave danger rose sharply last year and is now close to its 2013 level, despite extensive efforts by lenders to bolster balance sheets and profits, analysis by consultancy Bain shows.

- The eco calendar includes August Services PMI’s in the UK and EMU (final). Fed governors Brainard and Kashkari are scheduled to speak while Austria taps the bond markets.

Currencies: Korean Tensions Keep Dollar Near Recent Lows

Geopolitical uncertainty prevents USD comeback

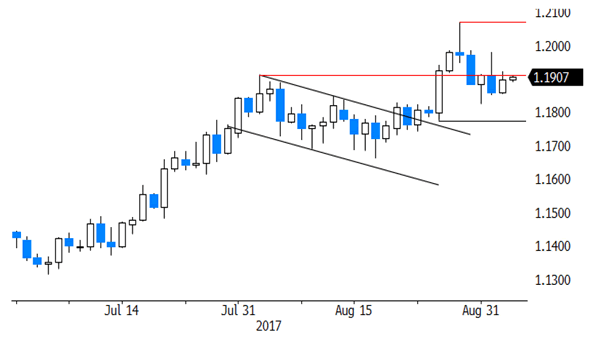

Tensions on the Korean peninsula were the only driver for global FX trading yesterday with the EMU eco calendar empty and US markets closed in observance of Labour Day Holiday. The dollar and equities were in the defensive, but reversed part of the early session setback during the day. EUR/USD closed the session at 1.1896 (from 1.1860). USD/JPY finished the day at 109.82 (from 110.25 on Friday).

This morning, Asian markets continue to trade with a slight risk-off bias, awaiting the next developments in the Korean crisis. The Chinese Caixin services PMI improved from 51.5 to 52.7. Chinese equity indices trade with slight gains. Other regional indices are trading mixed to slightly lower, Japan and South Korea underperforming. Safe havens like the yen are favoured. USD/JPY dropped to the 109.25 area. EUR/USD is again little affected, trading just north of 1.19. The RBA as expected left its policy unchanged at 1.5%. The central bank says that the higher A$ is weighing on the outlook for growth and employment. The A$ gained slightly after the publication of the Caixin PMI’s but lost a few ticks after the RBA policy statement. AUD/USD trades currently in the 0.7965 area.

Geopolitical tension on Korean peninsula continue to attract investors’ attention. EMU eco data, while interesting, will probably have little impact on FX trading. US headline factory orders are expected weak after a transport-driven decline in the durables. Aside from the volatile transportation items, the durable report was strong. Fed speeches of Kashari and especially Brainard may be more important. The former is well-known as an arch dove. Governor Brainard of the Washington-based board is also a dove, but she supported the gradual rate Fed hike path. A change in accent in her comments might affect US yields and the dollar.

The Korean-inspired risk-off weighed slightly on the dollar yesterday and will probably remain in play today. Of late, geopolitical tensions seldom had a protracted impact on global (FX) markets. Even so, we have the impression that it may take a bit longer for the ‘buy risk assets on dip’ paradigm to return. Investors will also look forward to the ECB meeting. More headlines/rumours on the ECB’s assessment of the recent euro rebound are likely. For now they had only a limited (negative) impact on the euro. In this context, we expect some USD softness to persist as long the Korea story dominates the news headlines. We expect EUR/USD to hold the 1.1825/1.2070 range going into the ECB meeting.

Global context. Dollar sentiment improved after the Jackson-Hole sell-off, but USD didn’t regain any technically relevant level against the euro or the yen yet. So, the jury is still out whether a sustained USD rebound is on the cards. The data might be slightly USD supportive, but a (moderate) risk-off sentiment doesn’t help the dollar. Therefore, we maintain a EUR/USD neutral bias ahead of the ECB policy meeting. If EUR/USD falls below the 1.18/1.1775 area, it would suggest more downside short-term. For such a move, the USD needs good data and higher US yields. On the euro side of the story, Draghi has to convince markets that low inflation is enough a reason for the ECB to maintain a loose monetary policy. On the topside, the 1.2070 correction top remains the first reference. A downward correction in core (US and European) yields supported the yen in August. USD/JPY declined from mid-114 mid-July and came within reach of the key 108.13 range bottom, but the support did its job. We maintain the working hypothesis that this level won’t be broken easily as a lot of USD bad news is discounted. A cautious buy-on-dips (with stop-loss protection below 108) may be considered. USD/JPY needs to regain 110.95 to improve the technical picture. Such a break might be difficult as long as global sentiment remains risk-off.

EUR/USD: in consolidation modus ahead of the ECB policy meeting

EUR/GBP

EUR/GBP correction doesn’t continue, at least for now

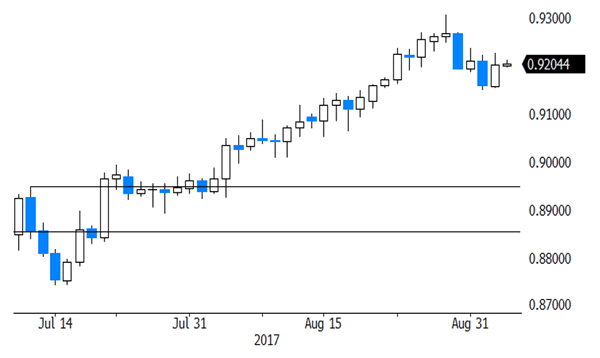

Sterling traders experienced an uneventful session yesterday. The UK currency traded slightly softer as risk aversion weighed slightly more on sterling than on the dollar and the euro. The UK construction PMI (51.1) also showed a further loss of momentum. However, both the moves in cable and in EUR/GBP were technically insignificant. EUR/GBP finished the session at 0.9202, cable at 1.2931.

Overnight, the BRC like-for-like retail sales rose from 0.9% Y/Y to 1.3% Y/Y. The report suggests that spending isn’t falling off a cliff even as consumers’ purchasing power is under pressure. Later today, the UK August services PMI is expected to ease slightly from 53.8 to 53.5. The manufacturing PMI was strong, but the sector profits most from the weaker pound. This won’t play for the services sector. A positive surprise might be slightly supportive for sterling, but we don’t expect a big reaction. Sterling entered calmer waters even as the third round of the Brexit negotiations entered a stalemate. Some more consolidation in EUR/GBP might be on the cards. A risk-off context is usually also of no help for sterling. From a technical point of view, EUR/GBP cleared 0.8854/80 resistance (top end June), opening the way for further gains. The move was the result of euro strength. Simultaneously, UK price data were soft enough to keep the BoE side-lined. MT, we maintain a buy EUR/GBP on dips approach as we expect the combination of euro strength and sterling softness to persist. The 0.9415 ‘flash-crash spike’ is the next target on the charts. We wait for a correction, e.g. to the technical support in the 0.88/89 area, to sell sterling again versus the euro.

EUR/GBP: sterling rebound stalls. Risk-off doesn’t help sterling