Summary

- The Federal Reserve is currently purchasing $80 billion worth of Treasury securities and $40 billion worth of MBS every month, and many market participants look for the FOMC to commence a “tapering” of its asset purchases in the near future.

- In our view, the disappointing labor market report for August and the uncertainties imparted by the recent surge in COVID cases on the economic outlook mean that an announcement of tapering at the upcoming meeting is quite unlikely.

- However, it is important not to miss the forest for the trees. Progress continues to be made toward the Committee’s goal of “maximum” employment. Unless the economic recovery is completely derailed over the next few months, we believe a taper announcement will be forthcoming at either the November or the December FOMC meetings.

- The Committee could potentially use its statement to signal the timing of tapering commencement. For example, changing the first sentence of the statement and/or characterizing the risks to the economic outlook as more “balanced” could signal that the FOMC believes that tapering is imminent.

- That said, we believe that the Committee will refrain from making substantive changes to the wording that it uses in the September 22 statement.

- Will the “dot plot,” which shows the expected pace of rate hike among the 18 Committee members, shift? A downgrade to GDP growth forecasts could cause some dots to shift lower. But forecasts of lingering inflation next year may lead some members to conclude that the pace of tightening that they expected three months ago is still warranted.

Crunch Time: November and December FOMC Meetings Likely To Be “Live”

The Federal Open Market Committee (FOMC) will hold a highly anticipated meeting on September 21-22. We describe the meeting as “highly anticipated” because the issue of the Fed tapering its asset purchases is very much on the minds of most market participants. To recap, the Federal Reserve bought significant amounts of U.S. Treasury securities and mortgage-backed securities (MBS) when the pandemic essentially shut down the economy in the spring of 2020. Last December, the Committee said that the Fed would continue to buy Treasury securities and MBS at monthly rates of $80 billion and $40 billion, respectively, until “substantial further progress has been made toward the Committee’s maximum employment and price stability goals.”

The statement that was released following the most recent FOMC meeting on July 28 indicated that the economy had “made progress” toward meeting these goals. Left unsaid was that evidently this progress was not quite “substantial” enough to warrant tapering of asset purchases. Consequently, it seems that commencement of tapering is drawing nearer. The question is when?

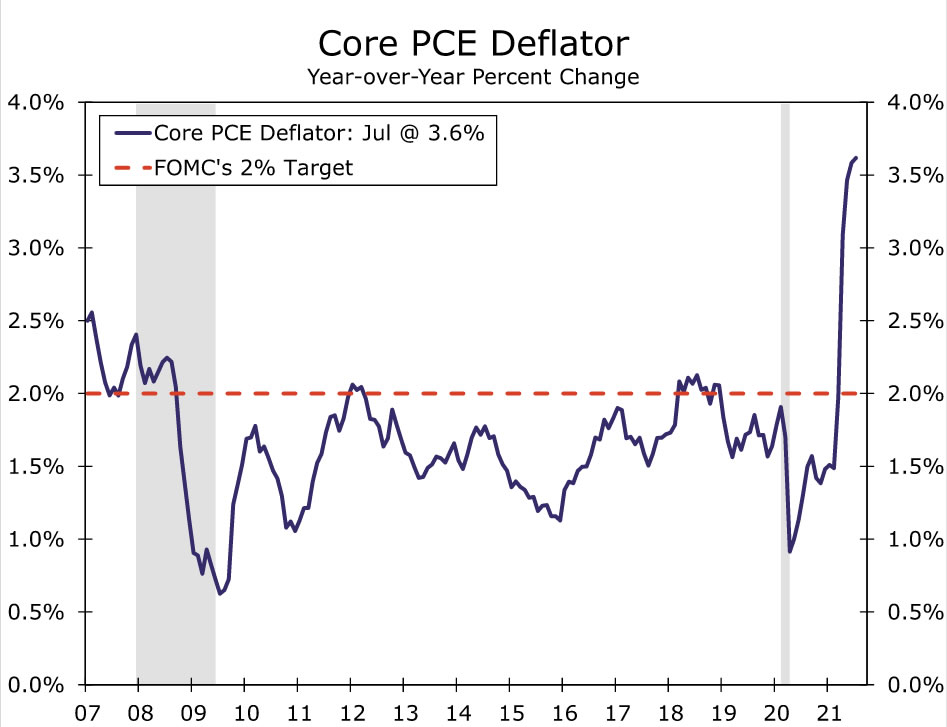

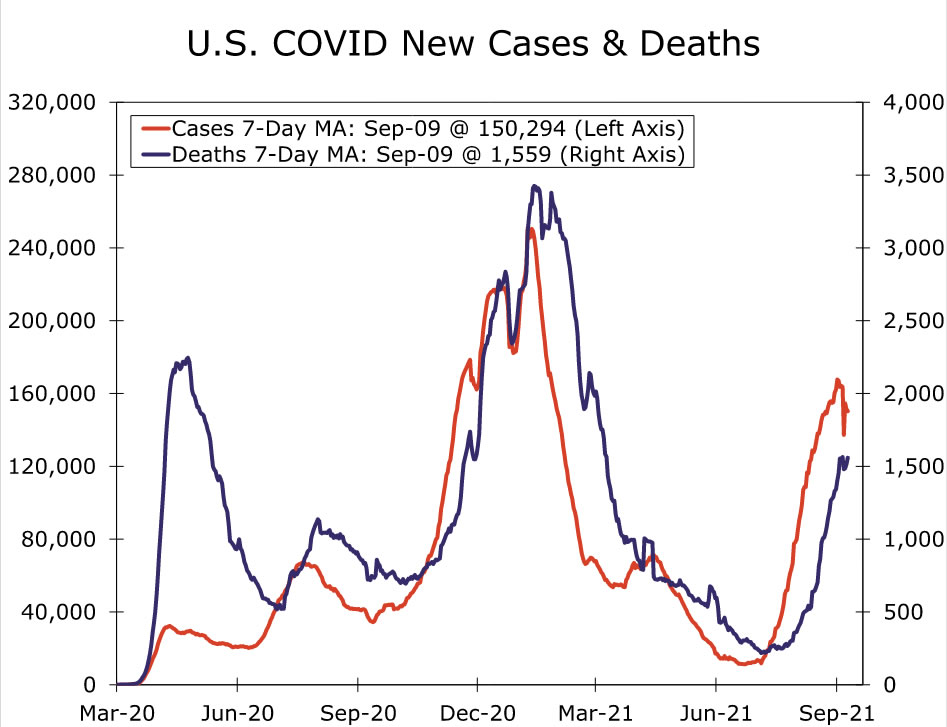

With inflation still running well above the FOMC’s 2% target, most Fed officials, including Chair Powell, have signaled that they believe the inflation half of “substantial further progress” has been met (Figure 1). This indicates that the labor market data will be critical to a taper announcement at either the November 2-3 or December 14-15 FOMC meetings. Since the July 28 FOMC meeting, the pace of the economic recovery has slowed amid the rapid ascent of new COVID cases (Figure 2). High frequency data and consumer confidence surveys softened in August, while nonfarm payrolls grew just 235,000 in August, the smallest increase since January. We suspect the additional “hard data” for August will be similarly weak when it is released later this month.

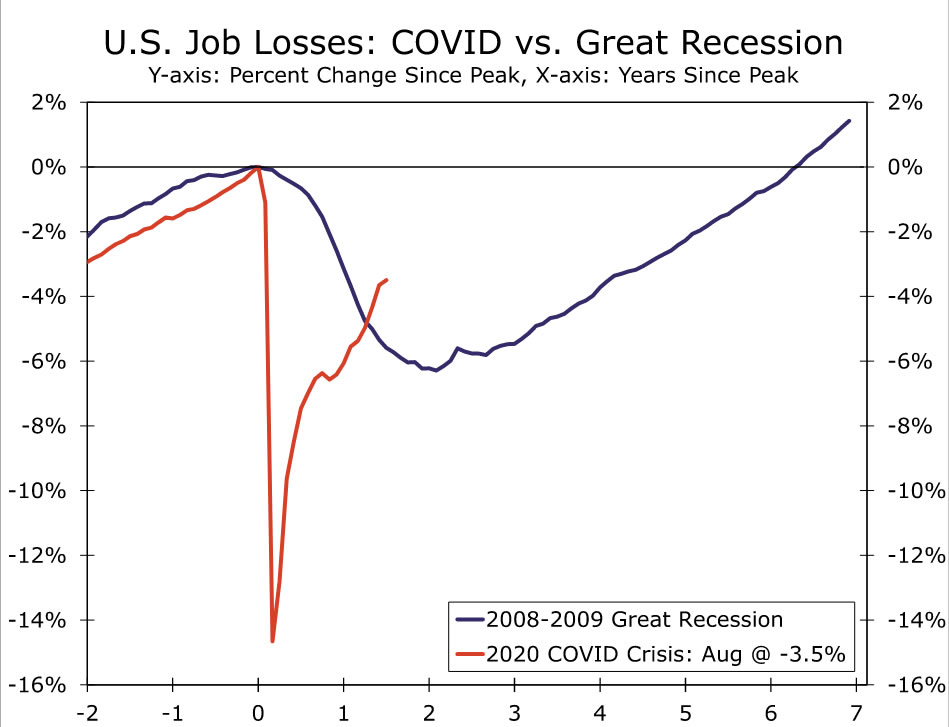

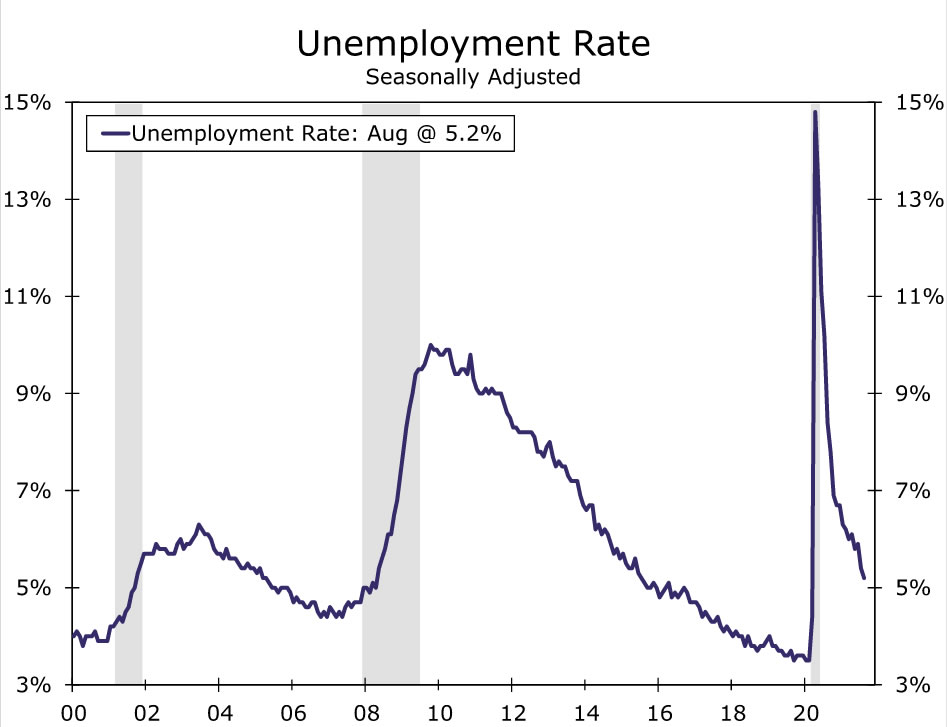

At first blush, this might suggest that the FOMC has taken a step backwards when it comes to tapering. Although we readily acknowledge that an announcement of tapering commencement at the September 22 meeting is quite unlikely, we would argue that November or December are still very much “in play.” The pace of progress may have slowed, but progress did continue as employment rose by 235,000 in August plus another 134,000 in upward revisions to the previous two months. Progress is cumulative, and employment continues to rebound much faster in this recovery than it did following the downturn in 2007-2009 (Figure 3). The unemployment rate has also fallen 0.7 points since the FOMC’s July meeting (Figure 4).

Furthermore, the Committee may view August as a useful model for how the economy will perform in additional post-vaccine COVID waves. It is encouraging to us that the economy continued to expand despite COVID cases that are at levels not seen since February, and this continued expansion may ease some concern among Fed officials as they look ahead to the winter.

That said, we believe the FOMC will be keenly watching the September employment report as it will be the last one the Committee sees before the November 2-3 meeting. The August miss is not the end-all-be-all for a November announcement if employment bounces back in September. The monthly job numbers have been very volatile throughout the re-opening process, and it is quite possible August’s miss will be revised higher and/or offset by a stronger number in September. A potential peak in COVID cases, school re-openings and the end of enhanced unemployment benefits all point towards a rebound in job growth in September.

Just how strong of a September employment report will be needed to bring about a November tapering announcement is difficult to say. Many factors beyond the headline number determine whether a report is “good” or “bad”. However, our sense is that a print of around 700K jobs or more would probably be enough to get the FOMC to announce a taper on November 3. Job growth around 700K would bring the combined rise in payrolls over August and September to around one million, and it would mean that the labor market has recovered just about 80% of the jobs lost at the beginning of the pandemic.

There is nothing magical about the 700K number. However, the further away the September employment report is from this mark in either direction, the more our conviction would likely grow regarding a November versus a December announcement. If the report comes in north of one million jobs with robust labor force and wage growth, it should be all-systems-go in November unless something else on the public health or economic front shows major deterioration. Conversely, if the September employment report shows another reading of just a few hundred thousand jobs, we suspect the FOMC will postpone a tapering announcement in November and wait until December to determine whether commencement is warranted. Although the two meetings are just six weeks apart, the timing of the October and November employment reports are such that the FOMC will have received two new employment readings between November 3 and December 15. Some Committee members have signaled the importance of seeing the autumn economic data, and a weak September employment reading may nudge them towards a bit more caution.

Although the exact timing of the taper announcement is relevant, we believe it is important to not miss the forest for the trees. Unless the economic recovery is completely derailed over the next few months, we believe a taper announcement will be forthcoming at one of the two final FOMC meetings of the year. In the grand scheme of things, tapering that starts in late November versus late December is a relatively small difference, and our impression is that markets are well-prepared for either of these outcomes. We will be reviewing the September FOMC statement and Chair Powell’s press conference closely for clues about the pace of tapering in addition to the timing.

During the tapering period that occurred over the course of 2014, the FOMC decided to reduce the Fed’s purchases of Treasury securities and MBS generally by $5 billion per meeting. Therefore, it took the Fed almost a year to wind down its monthly purchase rate of $45 billion for the former and $40 billion for the latter between December 2013 and November 2014.

As noted previously, the Federal Reserve is currently buying $80 billion and $40 billion worth of Treasury securities and MBS respectively every month. Our current forecast assumes the FOMC will reduce its pace of asset purchases by $10 billion for the former and $5 billion for the latter at each forthcoming FOMC meeting. But we acknowledge that the pace of reduction could be used as a counterbalance to the commencement of tapering. That is, if the FOMC decides to taper its asset purchases at the November 3 meeting, then it very well may opt for the $10B/$5B pace. Alternatively, if the Committee decides to wait one more meeting, then the continued inter-meeting economic progress might permit a faster pace of tapering along the lines of $15B/$7.5B per meeting. Either way, we believe the Fed will finish up its asset purchases sometime between next summer and fall.

Statement Changes Could Signal That Tapering is Drawing Closer

The statement that will be released at the conclusion of the meeting will outline the FOMC’s views about the current state of the economy, and the Committee could potentially use changes to its wording to give some clues on when tapering will commence. For example, the statement currently opens with the following sentence: “The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.” Indeed, this sentence has opened every statement since it was first used following the FOMC meeting on April 29, 2020. At the time, claims for unemployment insurance were spiking and economic activity was essentially in free fall. The prominent use of this sentence at the beginning of the statement signals that the Committee is willing to do everything in its power, including the purchase of Treasury securities and MBS, to support the U.S. economy. Removing this sentence entirely or moving it to a less prominent position would signal that the Committee believes that some of these tools may not be needed much longer and that tapering could potentially commence at the next FOMC meeting.

In addition, the FOMC noted in its March 2021 statement that “the path of the economy will depend significantly on the course of the virus, including progress on vaccinations. The ongoing public health crisis continues to weigh on economic activity, employment, and inflation, and poses considerable risks to the economic outlook.” The Committee implicitly upgraded its outlook at the April meeting by dropping “considerable” from the last sentence and stating simply that “the ongoing public health crisis continues to weigh on the economy, and risks to the economic outlook remain.” In both the June and the July statements, the Committee said “the path of the economy will depend significantly on the course of the virus. Progress on vaccinations will likely continue to reduce the effects of the public health crisis on the economy, but risks to the economic outlook remain.” Softening of this risk assessment further—maybe along the lines of calling the risks “more balanced”—would indicate that the Committee is feeling more optimistic about the economic outlook and that an imminent tapering of asset purchases may be appropriate.

We readily admit that the Committee could use these changes to the statement, or potentially others, to signal that tapering is drawing closer. But in our view, the disappointing print on non-farm payrolls in August slowed the “progress” that the economy has made toward the FOMC’s goal of “maximum” employment, and the recent surge in COVID cases clearly adds uncertainty to the economic outlook. In short, we believe that the Committee will refrain from making substantive changes to the wording that it uses in the September 22 statement. If economic data improves sufficiently in coming weeks, including the September labor market report that is slated for release on October 8, then Fed officials could use public comments throughout October to signal that tapering will commence in November.

Potential Changes to the Summary of Economic Projections

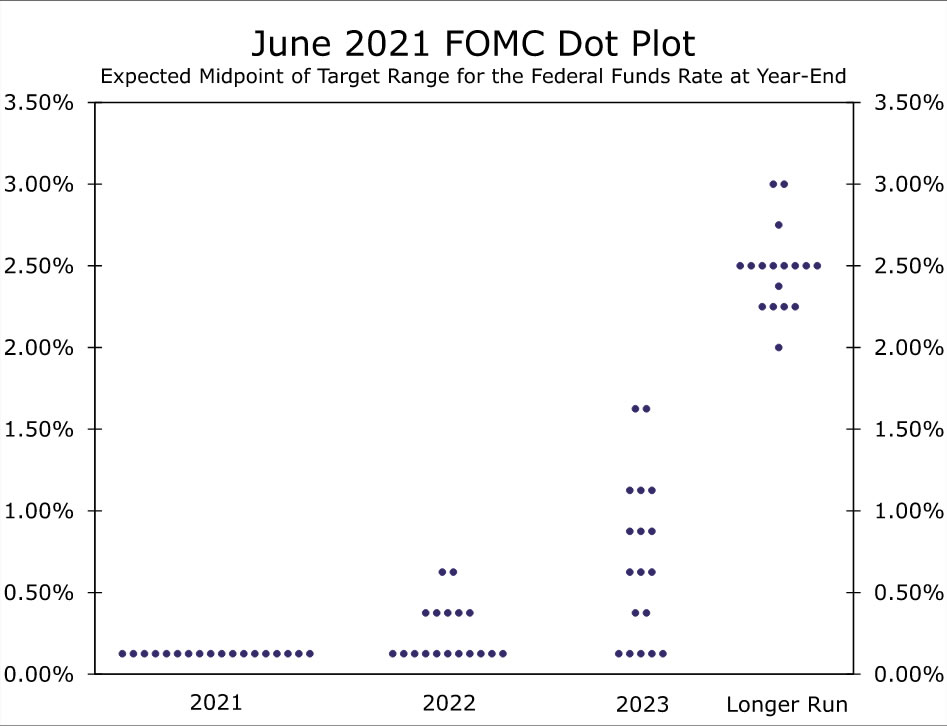

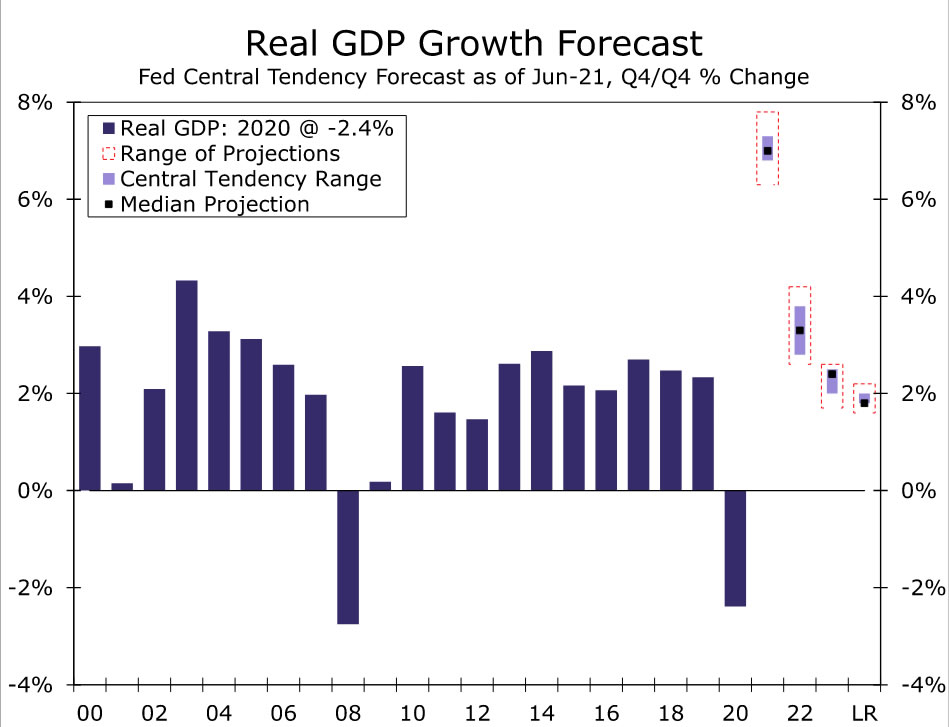

There is also the issue of rate hikes. Of course, nobody is looking for the FOMC to hike rates in the near term, let alone at this meeting. But the meeting may convey some information that should help market participants form expectations about the timing and pace of eventual monetary tightening. In that regard, the Summary of Economic Projections (SEP), which details the Committee’s macroeconomic forecasts and which is provided on a quarterly basis, is scheduled to be published at the conclusion of this meeting. The “dot plot”, which was released after the June 16 meeting, showed that seven of the 18 committee members thought that the target range for the federal funds rate would be higher than its current setting of 0.00% to 0.25% by the end of next year (Figure 5). Thirteen members thought the range would be higher at the end of 2023. Furthermore, the median forecast among the 18 individual projections in June saw real GDP rising 7.0% in 2021 (Q4-2021 relative to Q4-2020) followed by 3.3% in 2022 (Figure 6)

However, data on economic activity since June indicate that the economy has decelerated more quickly than many analysts had expected just three months ago. Furthermore, the downside risks to the economic outlook have risen since early summer. At the time of the last SEP in June, new COVID cases had receded considerably from their January highs and were averaging less than 15K/day, but new cases have subsequently skyrocketed. Re-imposition of restrictions that locked down the economy in spring 2020 do not seem to be likely. That said, high frequency data indicate that consumers have turned a bit more cautious recently with fewer visits to retail locations and restaurants as well as fewer airline flights.

In June, the average forecast among the Blue Chip panel of forecasters saw real GDP rising 6.7% this year and 4.4% in 2022. In August, the average for 2021 had been paired back to 6.2% (the average for 2022 remained unchanged at 4.4%). Therefore, it seems likely that FOMC officials may have made some downward revisions to their GDP growth forecasts as well. Everything else equal, expectations of slower economic growth could lead some committee members to rethink the appropriateness of hiking rates next year, leading to a downward shift in the dot plot.

But everything else may not be equal. Specifically, the median FOMC forecaster projected a 3.4% rate of PCE inflation this year and 2.1% in 2022. But the renewed spike in COVID cases has the potential to keep supply chains gummed up in coming months, which could cause inflation to recede at a slower pace than many committee members expected three months ago. In that event, the median inflation forecast could be bumped up, which could keep the dot plot from shifting lower. In short, the SEP that will be released on September 22 will convey important information about how Fed policymakers are thinking about the economic outlook and their monetary policy response.

{kind=link}