- In this paper, we give a short overview of the key questions in China in 2022 and what we expect.

- Overall, we look for the Chinese economy to recover moderately, crackdowns to ease but not end and that China’s zero-tolerance policy on Covid is here to stay for most of 2022.

- We expect limited impact on the economic agenda of the 20th CPC National Congress, which is mostly a political event. We look for tensions around Taiwan to remain high but see a small probability of a military confrontation anytime soon.

- Based on this, we look for Chinese stock markets to move higher in 2022 and for the CNY to weaken moderately.

#1: Will China’s economy recover?

Short answer: Yes – we lift our growth forecast from 4.5% to 5.0% in 2022

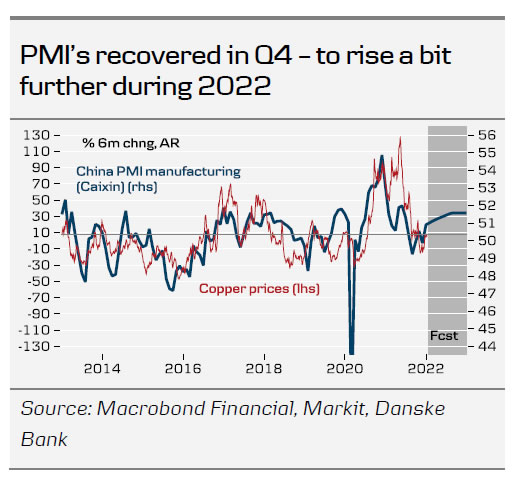

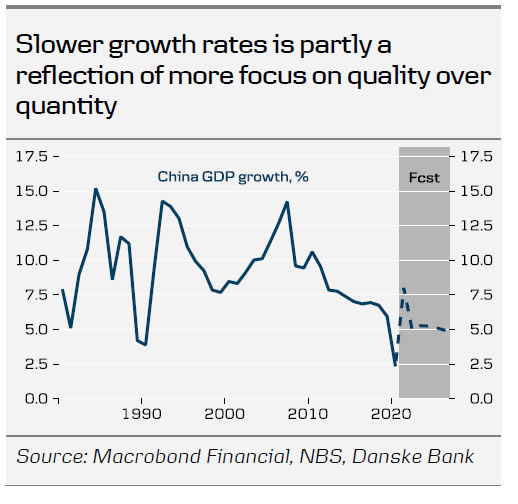

As we argued in Research China – Stimulus picks up ahead of CPC Congress in ’22, 21 December 2021, a key policy goal this year is stability. Following a year of economic downturn and property crisis, Chinese polices aims at stabilisation and is already taking measures to steer the economy back towards the middle of the road. Given the latest improvement in data which came a quarter earlier than we expected, we revise up our GDP forecast for 2022 to 5% from 4.5%. Infrastructure projects are pushed forward and steps have been taken to stabilize the property markets via easing of mortgage lending, increasing bank loans to developers and loosening the ‘three red lines’ regulation that puts caps on developers’ debt levels. The latter will facilitate that troubled developers can raise liquidity by selling projects to more healthy developers. While the economy is set to recover, it is likely to be a moderate one. Headwinds continue from Covid outbreaks, which will likely become more frequent due to Omicron. And Chinese policy makers still very much focus on long term sustainability and financial risks. So stimulus will be measured.

#2: Will the crackdowns continue in 2022?

Short answer: Yes, but probably less so than in 2021

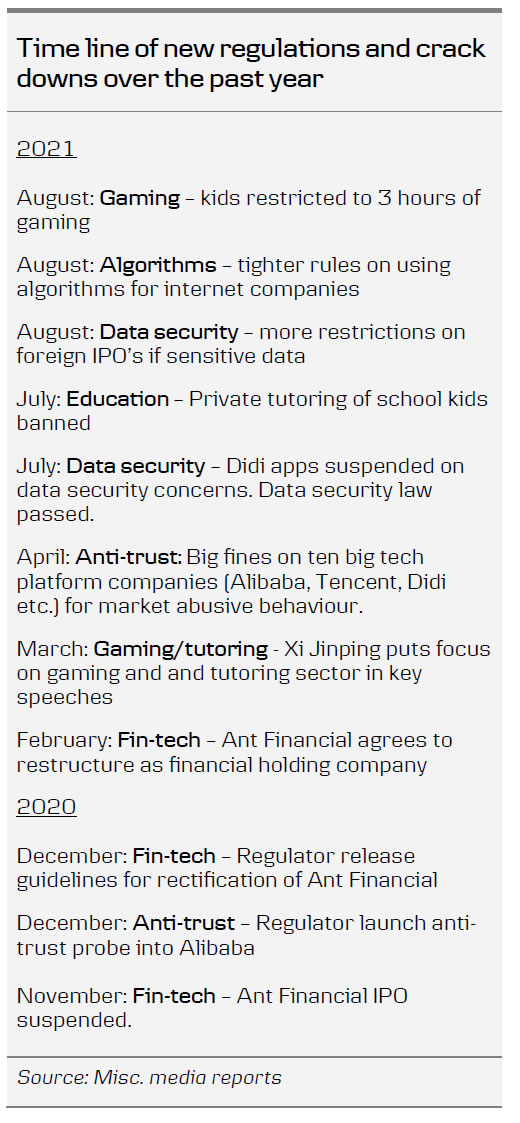

2021 was characterized by a blitz of crackdowns and new regulations: big tech internet companies received significant fines for abuse of market power, fin-tech faced much tighter regulation, a 3-hour ruls on kids’ gaming was implemented, private tutoring of school kids was banned and ride hailing company Didi faced suspension of apps for listing in the US without proper guarantee of data security. The crackdowns led to a big hit to foreign investor sentiment and in combination with the economic slowdown was a key reason for China’s significant underperformance in the offshore Hong Kong stock market.

While we expect regulations to continue in 2022, we look for the storm to calm down somewhat. The reason it is unlikely to go away is that China has already signalled it is set to continue. The rules are implemented for a variety of reasons that all have the goal of making the economy more efficient and improve the social balance. The crackdown on big tech, for example, is seen as an anti-monopoly market reform creating a more level playing field for smaller players. When it comes to gaming and education the motivation is social balance, protection of kids mental health and to some extent an aim to lower the cost of having a child in order to facilitate people getting more kids. Regarding Didi it is a matter of national security to protect sensitive data on hundreds of millions Chinese customers from ending up on foreign (not least American) hands.

The reason we expect it to slow down after all, is firstly that stability is a key objective in 2022. And rolling out too much new regulation in a short time has created uncertainty and instability in Chinese markets – which in turn raises Chinese companies financing costs. Secondly, the companies themselves are also better prepared to adapt to an environment where they know behaviour that can be seen as market abuse or breach of data security, will not be tolerated.

#3: Will the zero-tolerance COVID policy end?

Short answer: Probably not on this side of the CPC Congress

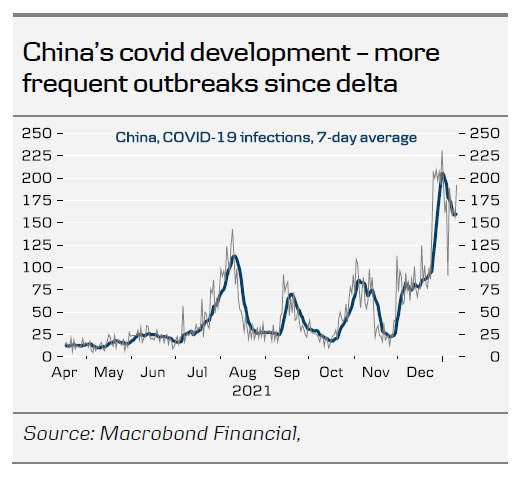

While China’s zero-tolerance COVID policy is becoming more challenging with the arrival of Omicron, there is no sign that this will change China’s policy on this issue. China sees its’ handling of the pandemic as far more efficient than most Western countries and that it has saved millions of lives while limiting too severe negative impact on the economy. If China had a proportional amount of deaths as the US, it would have led to more than 3 million deaths in China due to its’ 1.4 billion large population. While the official number of 4,636 deaths most likely underestimates the true amount, it is likely that China has indeed saved millions of lives.

An article in Chinese state media China Daily on 10 January was titled ‘Zero-Covid policy keeps pandemic under control’. It quotes head of China’s National Health Commission Liang Wannian saying that “This approach is the best option and the guiding principle of China’s disease control work. We must resolutely adhere to the policy and protect the health and safety of the population as the top priority.” While China has implemented more frequent and often harsh local restrictions, they tend to last shorter than restrictions implemented in Europe and are less widespread but focused on the specific areas where? the virus pops up.

So when will China end the zero-tolerance policy and shift to the ‘living with Covid’ as in most other countries? China’s respiratory disease expert Zhong Nanshan said in November that zero tolerance costs a lot but letting the virus spread would cost more. He outlined some criteria for when China could end its zero-tolerance policy: Basically the death rate and hospitalisation rate from Covid need to come down. This can be achieved by effective vaccines and a high vaccination rate. And a milder version of Covid. China has a high vaccination rate but its vaccines are less efficient and they need to be adjusted to Omicron. The fact that Omicron seems milder will help achieve this criteria. But it is too early to make that conclusion for China and they will demand clear evidence before they let it spread. In many parts of China the health system is weaker than in the big cities and hospitals could be overwhelmed if contagion is significant, which in turn could threaten social stability. China’s population is also getting old and it implies a bigger risk group.

Hence, despite rising economic costs of the zero-tolerance policy due to Omicron, we believe China will stick with it at least until the other side of the CPC Congress in Q4, where hundreds of the top of the Communist Party is gathered in Beijing. By then China will also have experience from other countries to draw on to evaluate effects of a shift to a ‘living with covid’ strategy.

#4: How will the 20th CPC National Congress impact the economic agenda?

Short answer: Not much

The Congress is instead likely to cement the policies and economic goals that has already been outlined over the past five years in what was labelled Xi Jinping Thought on Socialism with Chinese Characteristics in a New Era. China’s so-called New Development Philosophyhighlights a move from quantity to quality – from ‘growth at all cost’ during the first three decades of China’s ‘reform and opening-up’ period to ‘sustainable growth – economically, socially and ecologically.’

It puts much more focus on the long term goals and less on short term growth targets. China is far from having achieved many of these goals but the strategy and plans reflect the priorities of Beijing. The key pillars in the economic agenda are:

- More economic efficiency: One element of this is improved functioning of markets through for example anti-monopoly regulation, fighting vested interests and corruption, creating a better business environment – not least for SME’s, improving governance of state owned enterprises and a better allocation of capital through better functioning financial markets. Protection of intellectual property rights and ‘rule of law’ is increasingly prioritized to create a transparent business environment where rights are protected. Capital is also increasingly directed towards high-tech manufacturing, R&D and ‘smart infrastructure’ (5G, cloud tech etc.) and less so to construction and traditional infrastructure such as roads and bridges. Innovation is a cornerstone in China’s development strategy. Education and nurturing talent also play a key role in this. Finally short term stimulus measures aim increasingly to serve long-term needs as well such as ‘smart infrastructure’ projects and reduction of costs for businesses.

- Macroeconomic stability: A stable economic environment facilitates business investments but China is less fixated on a specific growth target and now sets targets that are easier to reach in order to avoid wasteful investments by local governments just to reach the target. China allows short term downturns but aims to keep a selection of indicators, such as employment and income growth, within a certain range.

- Dual circulation and improved self-sufficiency: The tech war with the US and to some extent the Covid crisis have made it clear, that China is vulnerable in certain parts of the supply chain. The dual circulation strategy aims to strengthen the weak links in supply chains and have a higher degree of self-sufficiency on key components and materials, such as technology, energy and food. At the same time China wants to develop a stronger domestic market while keeping the door open for foreign production in China. In that sense, China can become more independent of the world but at the same time keep the world dependent on China.

- Social balance: In China’s view the economic development is only sustainable if it also comes with social balance. The polarisation and high inequality in the US are seen as a lack of focus on social balance. The increased emphasis on ‘common

prosperity’ suggests that in the new era, China will increasingly work on a more inclusive economic development compared to the previous decades. Education, social policies, regional strategies to decrease imbalances across the country, more affordable housing, a property tax and higher taxation on the rich and big corporations are likely tools that will get an even stronger weight. China has signalled it will be a gradual process, though, and not a sudden shift. - Ecological balance: Finally, sustainable development implies a much stronger focus on the environment and climate. China has strengthened environmental laws and the enforcement of them and the climate goal of achieving carbon neutrality in 2060 was formulated by Xi Jinping in 2020.

#5: Will tensions over Taiwan increase further?

Short answer: Probably not but high level of tensions is set to continue.

There is no doubt that tensions over Taiwan have increased in the past years and the ‘strategic equilibrium’ has been challenged. Frictions started to increase following two key political events: First, in 2016 Taiwan’s current president Tsai Ing-Wen came to power as leader of the pro-independence Democratic Progressive Party taking over from the more pro-Beijing KMT party. Second, the election of Donald Trump for US President in the same year, which marked a clear hardening of US policy on China including on the Taiwan issue.

When Tsai Ing-Wen made a phone call to the at the time President-elect Trump in November 2016 to congratulate him, it was clear that a shift was under way that would challenge the US ‘One-China’ policy, which had been in place since 1972 and implied no diplomatic relations with Taiwan since 1979. For the past five years tensions have only increased and reached a new peak in 2021 with more US support for Taiwan and an increase in semi-diplomatic relations. China has responded by increasing military drills in the area and a record number of flights into Taiwanese air space. From China’s perspective, Taiwan is Chinese taken from them by Japan in 1895

It has raised the question whether we are on course to a military confrontation. While risks have increased, most experts agree that a war within the next couple of years is unlikely, see for example this article from The Conversation. A war will come with significant risks for all three players. For China, it is likely to come with significant casualties and with many challenges to military success no matter which strategy they choose (surprise attack, full invasion or blockade). Add to this the risk of US intervention that could spiral out of control. Significant economic sanctions by the West and export bans of key technologies could cause severe disruption to the Chinese economy. For the US, intervention could also bring significant losses that American people might not be willing to sacrifice. As well as the similar risk as China faces of things spiralling out of control. And for Taiwan a war could, of course, be very costly with the risk of occupation and suppression and loss of many human lives.

China has been clear that Taiwan needs to come back to the mainland eventually, preferably peacefully but if necessary by force. But in a call with US President Biden, Xi Jinping said that “we have patience and will strive for the prospect of peaceful reunification with utmost sincerity and efforts“, see overview hereof Xi’s comments on Taiwan over the six monts. China is likely to respond with increasing military drills etc. whenever the US or Taiwan pushes closer to the ‘red lines’ to underline that China is serious about taking Taiwan if the ‘red lines’ are crossed. But at the same time, while the US and Taiwan are set to continue to confront China and push as close as possible to the ‘red lines’, they are unlikely to cross them due to the above mentioned reasons.

Despite the confrontations, the US has continued to officially state support of the ‘One China’ policy, although in practice it often take steps that seem at odds with it. It has also stuck to the so-called ‘strategic ambiguity’ where it sticks to the support for Taiwan to defend itself but without stating outright that the US would defend Taiwan directly in the case of war. This is a sign that while the US supports Taiwan, there is a limit to how much they wish to challenge Beijing.

So what are the ‘red lines’ that could trigger war? A clear declaration of independence from Taiwan with support from the US will likely be one of them (it is unlikely that Taiwan would make such a declaration without talking to the US first).

It cannot be ruled out that a possible new Republican government in 2024 in the US would go further than the Biden administration. But in our view it is unlikely we will see a war during the Biden administration. However, we should expect tensions to remain high and might even go higher in 2022.

Financial implications: Equities to recover, CNY to weaken

With China likely to recover this year and the crackdowns turning down a notch or two, we believe there is upside to Chinese stocks in 2022 – especially in the offshore market as this has taken the biggest hit in 2021.

For the CNY, we expect the combination of easing monetary policy by the PBoC and Fed hikes starting this spring is set to underpin a move higher in USD/CNY. Importantly, we also look for a decline in China’s trade surplus as exports will likely lose some steam while we look for imports to turn higher in line with the increase in domestic demand.

For global stock markets, the gradual recovery in China should provide some support but it will take place alongside headwinds from slower global growth, Fed tightening and less support from central bank liquidity.

Looking to commodity markets, a Chinese recovery driven by investments will increase commodity demand from China. However, it will be a moderate recovery and also come in a year where global manufacturing outside China is set to see slower momentum. So commodity prices should still see only moderate increases which will help reduce global inflation pressures from this angle (wage growth will work in the other direction, though).

{kind=link}