- After the hawkish ECB meeting today, we change our ECB call and now expect the ECB to hike its deposit facility rate in December this year, and again in March 2023, by 25bp each, which will bring the deposit facility rate to 0%. For now, our call is for a ‘two-and-done’. We expect Danmarks Nationalbank (DN) to follow the ECB and hike the deposit rate to -0.10%.

- There is still elevated uncertainty on this call, but given that Lagarde highlighted the uncertainty of the model framework in its staff projections, that inflation will remain elevated for longer than previously expected, and a tight labour market, we change our view to acknowledge the increased risk, which now becomes our baseline.

- Given the highly uncertain inflation outlook, the ECB left out the sentence from December, which said that inflation was projected to settle below 2% – which is a hawkish shift in our view.

- On several occasions during the press conference, Lagarde had to close the door for a rate hike in 2022, but she intentionally left the door open ensuring that she did not want to make pledges without conditionality.

- For the first time since 2014, the ECB added a risk assessment to the inflation outlook in its monetary policy decision, which are on the upside, in particular in the short-term.

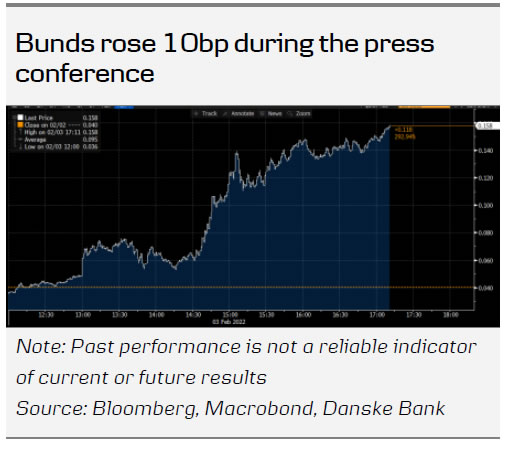

- Today’s meeting will also be remembered to show the largest difference to date between the ECB’s released decision and the press conference. The ECB’s decision released at 13:45 CET carried almost no changes, where the ‘at present or lower’ and sequencing was confirmed.

- Indications of TLTRO to be discussed in March or later.

Growth risk broadly balanced – elevated uncertainty with tight labour market

The growth risk outlook, which was assessed to be broadly balanced, carried the expected small nuances to the December decision. Domestic demand expected to fare well, in particular after the restrictions end, where the impact from Omicron was assessed to be less, while highlighting geopolitical uncertainties.

On the inflation front, Lagarde said that the majority was still energy driven, but food prices were highlighted due to seasonal factors (elevated transportation cost and fertilisers). There was unanimity in the governing council that the high inflation print was of concern. She also highlighted a larger share of price increases and uncertainty for how long the pandemic-related high inflation implications would remain. The most recent inflation figures were unanimously seen with concern.

Previously, we argued that the wage dynamic was the missing piece in the puzzle for us to change call for a rate hike. Lagarde clearly downplayed the importance of this by highlighting its lagged nature of the measure, but also that the participation rate is now at pre-Covid levels and unemployment rate below the start of the pandemic, and expected to tighten further.

Sequencing still holds – rate hike in December

We now expect the ECB to hike in December this year by 25bp for the first time since 2011. While Lagarde emphasised the flexibility and optionality of the calibration of instruments and its data dependency, she reiterated several times that sequencing is still valid. This means that the ECB will end its net asset purchases before hiking policy rates. Given the wording today from Lagarde, we believe the ECB will use this option in December, as we do not expect the ECB to accelerate the taper purchase pace (current guidance until October), sufficient to open for a September hike. However, there is a risk that the ECB will follow the Fed’s accelerated taper decisions, which would bring September in play.

As we have seen increased awareness about the negative side effects of the negative interest rate policy, we expect the ECB to go for ‘two-and-done’, bringing the deposit rate to zero in March 2023.

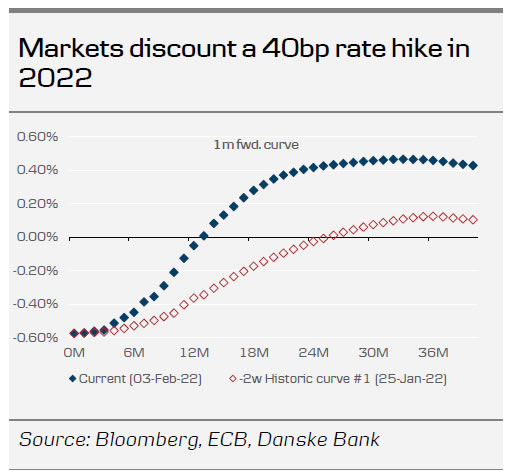

Despite our new ECB call, we still find the 2022 pricing aggressive. At the time of writing, markets are pricing in 42bp for December this year.

EUR rates fuelled EUR/USD move higher

EUR/USD increased around a figure on the ECB meeting, to around 1.14. The dominant driver was a repricing of where European interest rates should be: higher. The reaction itself – that EUR/USD follows yields during the brief time span of the ECB press conference – is quite common. However, spot is generally decoupled from yields over the 1-3m horizon, and we expect this to continue to be the case.

At present, the market’s focus is quite short-term. Indeed, as of last week, EUR/USD dropped substantially on the back of the hawkish Fed meeting and this week, we see the exact opposite on the back of the ECB meeting. Looking ahead, the upcoming US CPI print can easily turn market’s attention around again. Equally so if the bounce in global equities comes to a halt (USD positive). It is also quite common that the ECB speakers may ‘clarify’ the message in the following days – in either direction and with equal implications for EUR/USD spot.

Looking a bit further ahead, we continue to see EUR as overvalued vs. fundamentals, for the investment environment to change in a manner that is a drag on the EUR and for European data to underwhelm. We do not expect, nor see, that relative policy rates are a big driver in EUR/USD spot. In 12 months, we continue to forecast EUR/USD spot at 1.08.

Danmarks Nationalbank to follow the ECB

We expect Danmarks Nationalbank (DN) to follow the ECB and hike 25bp in December and March, respectively. We expect DN to hike both the repo and the deposit rate. After the two hikes, the repo rate would be 0.05% and the deposit rate -0.10%. EUR/DKK trades at the low end of the trading range and last year DN was forced to sell DKK in FX intervention to floor EUR/DKK around the 7.4360 level. We see a possibility that DN could hike 10-15bp less or cut in between ECB hikes if downwards pressure on EUR/DKK spot and need to sell DKK in FX intervention returns in Q4 this year or Q1 next year.

{kind=link}