The upcoming week will quieten down a bit after what was a busy time for central banks and geopolitical events. But there’s still plenty of activity ahead as the latest flash PMI readings are due and the Swiss National Bank will keep the monetary policy theme running, not to mention how the war in Ukraine will unfold amid slow progress in the negotiations for a ceasefire.

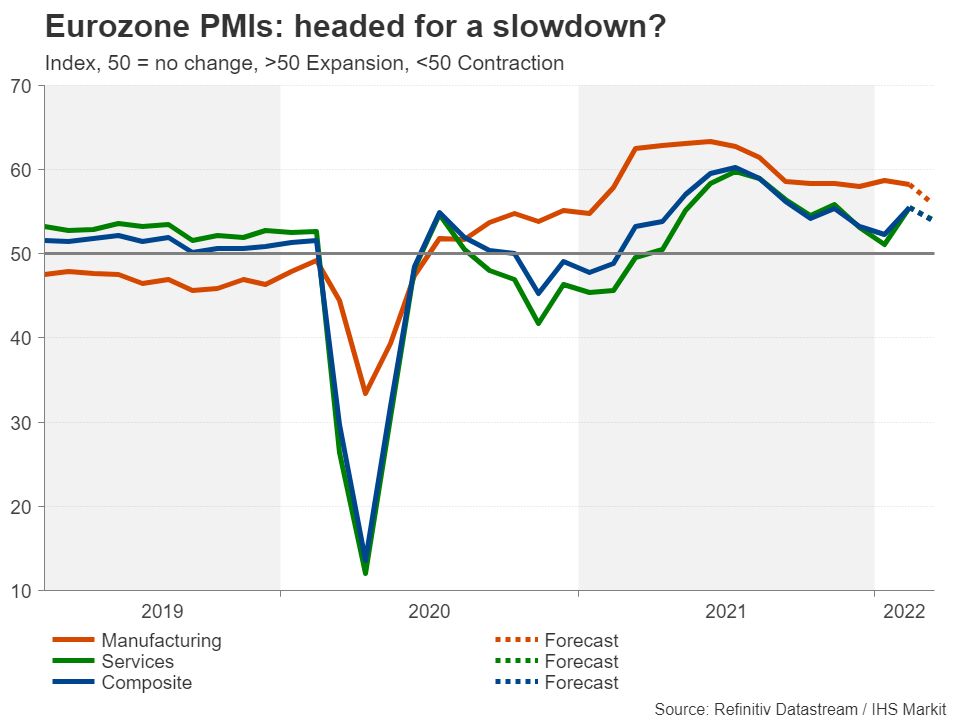

Will Eurozone PMIs flag a slowdown?

The fallout from the Ukraine conflict has had far-reaching consequences on global markets and on the economic outlook as the world has slipped into a new crisis just as it was emerging from another one. But the most startling impact has been on inflation, as the sanctions against commodity-rich Russia have inflamed already boiling price pressures.

With everything from energy, agricultural and metal commodities shooting higher since Russia invaded Ukraine, the squeeze on businesses and consumers has tightened even more, sparking fears of a recession. Europe is at a greater risk from suffering another downturn as it has become too dependent on Russian oil and gas for meeting its energy needs over the years.

European exporters will additionally have to bear the consequences of the tough Western sanctions, and combined with soaring input costs, business confidence has already started to dip. This puts all the more focus on Thursday’s flash PMI numbers for the euro area for March as investors will want to see whether the geopolitical turmoil on the European Union’s doorstep is denting economic activity. The Ifo business climate gauge on Friday will also be watched.

The European Central Bank just announced it is going to wind down its asset purchase programme at some point during the summer but did not commit to a timeline for raising rates. If the PMI data is weaker than anticipated, rate hike bets might be pared back and the euro could skid again, having only just bounced back from 22-month lows against the US dollar.

SNB not expected to alter policy path

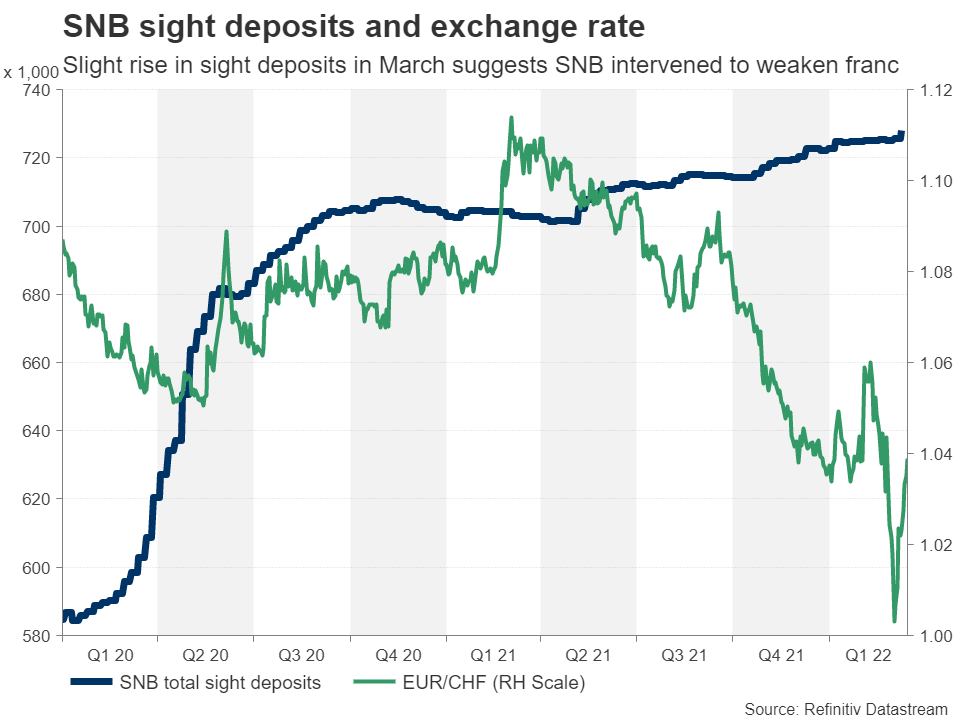

The euro’s downfall against the Swiss franc was also quite pronounced. Euro/franc briefly fell below parity on March 7 as the fighting in Ukraine intensified and as speculation mounted that the ECB would delay its stimulus exit. The Swiss National Bank likely intervened to push down the franc, but its sight deposits data suggests it only did so modestly.

Nevertheless, the SNB is expected to reiterate its pledge to intervene if necessary to keep the franc down when it meets on Thursday, as the currency has appreciated along with other safe havens like the dollar and yen during this turbulent period. The SNB recently revised up its forecasts for inflation for 2022, while downgrading its growth projection for the year.

However, inflation is still seen at only 1.9%, thus, it’s unlikely the SNB will signal any tightening as it keeps the policy rate on hold at -0.75%. Switzerland’s economy is not very exposed to Russia, nor does the country rely much on oil and gas imports for energy as it mostly uses hydro-electric and nuclear power. So any impact from the Russia-Ukraine war will probably be limited.

Still, investors are predicting that the SNB will have lifted rates out of negative territory by the first quarter of 2023. Though, in reality, that can only be possible if the ECB does the same. Until then, the SNB is expected to stick to exchange rate intervention to prevent any unwarranted spikes in the franc while geopolitical risks remain elevated.

Can Sunak halt the pound’s slide?

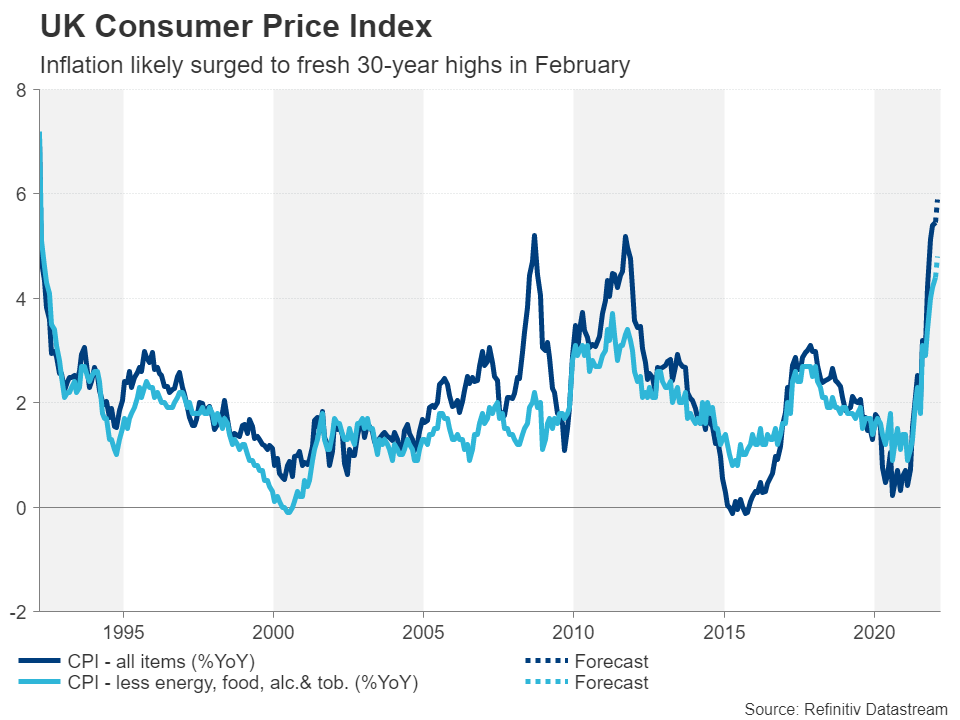

Flash PMI prints are also due out of the UK on Thursday and like for the euro area, they are forecast to tick lower in March. Retail sales figures for February out on Friday will be important too. Although the economic pain in Britain from the sanctions against Russia will probably be less than in the Eurozone, investors were already worried about how rising inflation and energy bills would affect household spending in a consumer-driven economy.

Those worries might explain why the pound hasn’t really benefited much from the Bank of England’s rate increases. The BoE hiked the Bank Rate for the third consecutive meeting this week as inflation keeps heading higher. Data out on Wednesday is expected to show the UK consumer price index jumped by 5.9% year-on-year in February.

But despite the spiralling prices, it seems that some policymakers have already started getting cold feet about further tightening amidst the Ukraine crisis, as there was a surprise dissent in the BoE vote.

Sterling is now at risk of revisiting the recent 16-month low just below $1.30 unless Chancellor Rishi Sunak comes up with a plan to help households and small businesses with the surge in fuel prices when he makes his Spring Budget Statement on Wednesday.

Sunak is under pressure to provide additional relief than the measures he had announced back in February and should he deliver, the pound could claw back some lost ground.

Ukraine headlines may dictate dollar’s direction

Unlike the BoE, the hawkish signals emanating from the Fed at its March meeting couldn’t have been louder. Yet, the dollar slipped after the decision, suggesting that rate hike expectations have been fully baked in by now. It’s hard to see how next week’s second-tier data might put the wind back in the dollar’s sails.

New home sales for February will be the first major release on Wednesday, followed by durable goods orders for the same month and the final Q4 GDP estimate on Thursday. The flash PMIs are out too on Thursday. Although these aren’t as closely watched in the US as the ISM PMIs, investors will nonetheless be keeping an eye on them for clues as to whether input and output price inflation are close to peaking and if growth momentum remained strong in the first half of March. Pending home sales will wrap things up on Friday.

In a crucial month for central bank meetings, monetary policy stole the limelight somewhat from the war headlines in the last couple of weeks. But with the ECB, Fed, BoE and BoJ decision now out of the way, geopolitics will likely take full helm again.

Should the efforts for a ceasefire between Russia and Ukraine falter, the dollar could resume its uptrend, pressuring its main rivals, the euro and pound.

The Japanese yen also stands to gain from any renewed risk aversion, having tumbled sharply since signs of progress from the peace talks first started to emerge as well as from the Bank of Japan not joining its global peers in withdrawing stimulus. Japanese PMIs due Thursday are unlikely to attract much attention for the yen.

{kind=link}