Last week’s FOMC meeting delivered a 25bp rate hike and a clear signal that balance sheet normalisation will begin in Q2. The surprise for us was the Committee’s decision to narrow their focus for policy to the inflation outlook, having previously taken a balanced view across inflation and activity.

This decision comes at a time of heightened global uncertainty and, for the US, declining real wages and tightening financial conditions. But the FOMC is confident in the strength of the US economy, believing it will be able to weather these headwinds and maintain full employment.

When central banks provide such explicit public guidance as we have recently seen from the Chairman and other members of the FOMC with respect to meetings in the very near term we listen and learn. That approach does not necessarily follow for longer term guidance where our economic forecasts may differ from those being used by the central bank.

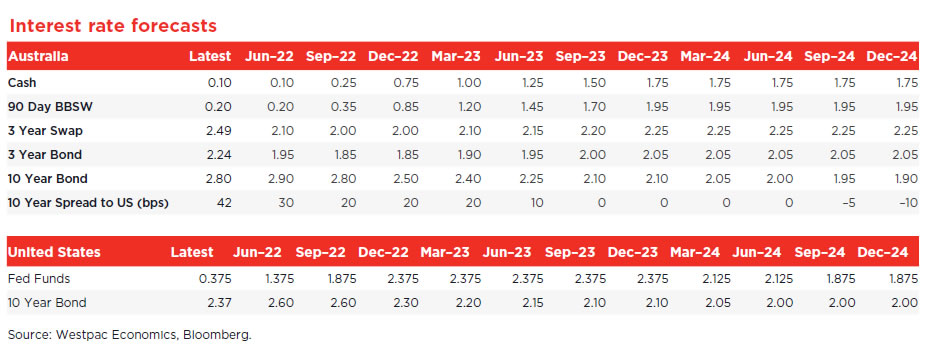

Therefore, recognising that clear intent, we have brought forward our rate hike profile to accommodate a move at every meeting this year. It starts with 50bp moves at both the May and June meetings, to be followed by a series of 25bp hikes in July, September, November and December. The federal funds rate reaches 2.375% by year end.

Our previous prior was that the combination of five hikes in 2022 and two more by June 2023 in combination with a determined approach to shrinking the balance sheet would weigh significantly on the US economy. The new accelerated profile will result in a more immediate slowing in growth and inflation, hence our expectation that the cycle will be completed by December 2022 when the slowdown will have become abundantly apparent.

Once inflation is back under control, we expect the FOMC to cut twice back to 1.875%, through 2024 to help growth sustain a near trend pace into the medium term.

Why do we expect the peak federal funds rate to be materially below the current guidance of the FOMC (2.8%) and the view of the market (2.7%)?

From a policy perspective, we are expecting that the determined commitment to reduce the size of the balance sheet combined with a series of rate increases will have a nonlinear impact on financial conditions, as we saw in 2017/2018.

We also expect more vulnerability from the labour market than is the FOMC’s base case.

Employment growth has been very strong throughout this recovery resulting in a very tight labour market (currently 1.7 openings for every available worker) and the unemployment rate is printed 3.8% in February. Yet, because of low participation, the share of the population employed is only 0.5ppts above its level in November 2015, when the 2015–2018 hiking cycle commenced. This matters, because the share of the population employed dictates the base earnings capacity of the household sector and consequently their spending.

In addition to the number employed, the other important aspect is the pace of wages growth. While the Employment Cost Index was abnormally strong over the year to December at 4.5%yr, this gain was swamped by CPI inflation of 7.1%yr, leaving real wages 2.6% lower than a year earlier. If we take monthly earnings from the establishment survey as a guide for wage growth in Q1 2022, it is clear real wages continue to decline, with CPI inflation running at more than twice the annualised growth rate of average hourly earnings.

As the FOMC’s focus remains on inflation in coming months, higher interest rates across the curve will continue to dial up the pressure on US households which are under the relentless pressure of contracting real wages.

GDP growth will hold above trend in 2022. But growth is then expected to slow from 2.1% annualised in the six months to December 2022 to 1.7% in first-half 2023 and 1.4% in the second.

Although the aggregate household balance sheet shows a high level of savings, these savings are reported to be overwhelmingly held by high income earners, limiting the buffer for tightening financial conditions and falling real wages. The unemployment rate is also expected to edge up to 4.5% by end- 2023 as participation continues to normalise and growth slows.

Inflation momentum is almost certain to ease.

We expect six-month annualised CPI inflation to hold above 5% to June 2022, falling to 2.9% in December 2022 before slowing further to 2.4% in June 2023 and 2.2% in December 2023.

Energy prices are expected to decline modestly from in 2022 H2 while supply-chain disruptions to other goods prices will dissipate as risks related to COVID-19 and the invasion of Ukraine recede.

That easing in supply pressures will be complemented by the slowdown in demand to ease inflation momentum.

Our forecasts still incorporate price growth for goods (exenergy) remaining materially above the pace seen prior to the pandemic. Growth in food prices is also forecast to remain elevated well into 2023 given the potential for significant secondary price rises over time. And shelter costs are projected to continue increasing at a rate in the top half of their historic range reflecting limited excess capacity.

Even if these pressures result in slightly higher inflation in 2023 than our current forecast, we expect the FOMC, committed to its recently adopted average inflation policy, will be comfortable to hold rates steady and concentrate on balance sheet repair that will take years.

What are the implications for 10-year bond rate?

We retain our guideline that the 10-year bond rate will peak around 6 months before the peak in the federal funds rate and at a slightly higher level.

We have therefore lifted and brought forward the peak for the 10-year bond to 2.60% by June (from 2.3% by December), still reaching its peak 6 months before the peak in federal funds rate (2.375%). It is only expected to hold at this level until September before declining to 2.30% by December 2022 and 2.20% by March 2023, a slight inversion of the curve relative to cash. We expect the curve to invert further through 2023 as the market recognises growth has slowed below trend and inflation is no longer a concern.

Two rate cuts during 2024 for a federal funds rate of 1.875% will settle expectations for both the economy and the curve.

If we are wrong and the federal funds rate reaches current market pricing, a sharp curve inversion will surely precede a much more significant slowdown in the US economy.

This adjustment has implications for the RBA.

We have not changed our core views that the RBA tightening cycle will begin in August with the cash rate peaking at 1.75%. Even though we are still on board with the RBA Governor’s intentions to run policy according to Australian conditions rather than following FOMC policy the more determined actions of the FOMC are likely to slightly accelerate the RBA’s tightening profile.

Our current forecast is for the RBA to raise the cash rate by 15 basis points in August; to be followed by 25 basis points in October; and 25 in February; May; August; and December in 2023; with the final 25 in February 2024.

We now expect the RBA to bring forward the third hike from February, 2023 to December 2022, and follow the same pattern throughout 2023 with the cycle ending in November 2023 rather than February 2024.

This would mean that the RBA would end 2022 having restored the 65 basis points of emergency cuts which it implemented during Covid.

Relative to market expectations our forecasts for the cycles of both FOMC and RBA are significantly more modest, relying on two things – more progress in settling inflation and tempering demand than is expected by the market and the complementary tightening of financial conditions that will be delivered by both central banks as they shrink their balance sheets – FOMC through its QT policies and RBA with the repayment of the $180 billion TFF in September 2023 and June 2024.

With the RBA expected to be narrowing the wide interest rate differential with the FOMC during 2023 and prospects of cuts in the federal funds rate in 2024 a more settled risk environment in 2023 still supports our forecast for the AUD to reach USD0.80 in 2023.

{kind=link}