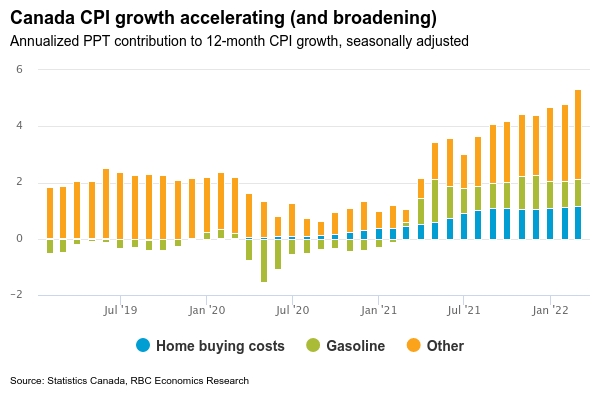

Next week’s Canadian CPI report is expected to show a further acceleration to 6% in March. That would top the 5.7% February reading that was already the highest since 1991. Soaring gasoline prices are expected to account for almost a quarter of the increase—and half of the price rise from February as energy surged higher on the Russian invasion of Ukraine. Home buying costs (realtor and broker fees, etc) have accounted for another 20% of the increase. With housing markets still running hot, these are also expected to have moved higher again in March.

Price pressures are continuing to broaden out. The war in Ukraine has added to global supply chain disruptions and input price growth. And consumer demand has risen sharply alongside the strongest labour market in decades—with those consumers continuing to hold exceptionally large savings accumulated during the pandemic. Compared to pre-pandemic levels, about two-thirds of the CPI basket is now growing at a rate above the Bank of Canada’s 2% inflation target.

The BoC’s newly-minted forecast shows inflation averaging 5.3% in 2022—more than 1 percentage point higher than its previous forecast in January. With labour markets also looking exceptionally strong, there’s no reason for interest rates to still be at emergency low levels. The BoC already hiked the overnight rate by 75 basis points over the last month and a half—including the 50 bp hike on March 13th. We look for another 100 bps worth of increases to bring the rate to 2.0% by October.

Week ahead data watch:

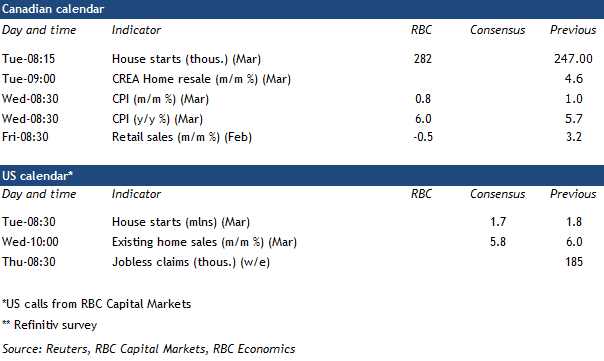

- The preliminary estimate of February Canadian retail sales was down 0.5% after a solid 3.2% gain in January. With consumers showing strong demand for goods during the pandemic, and prices higher, retail sales will still be more than 12% above pre-COVID levels.

- We expect Canadian housing starts to rise to 282k on very strong recent permit issuance in February.

- Canadian home resale markets likely remained exceptionally tight in March. Local real estate board data showed heated activity in the month, and though prices continued to grow and inventories very low there are early signs of moderation in some larger markets.

{kind=link}