Now that it is generally accepted that the RBA tightening cycle will begin in June, with a series of consecutive hikes, interest is firmly targeted at the likely peak in rates in the cycle. The steady 4% unemployment rate that has just been reported for March will take some pressure off the markets’ push for a hike in May.

We revised our profile last week to bring forward the timing of the peak to June 2023 (from November) and lift it from 1.75% to 2.0%.

That is a long way from the 3.4% currently priced into the market and the “theoretical” 3.5% associated with 1% real and 2.5% inflation that is often favoured by central banks.

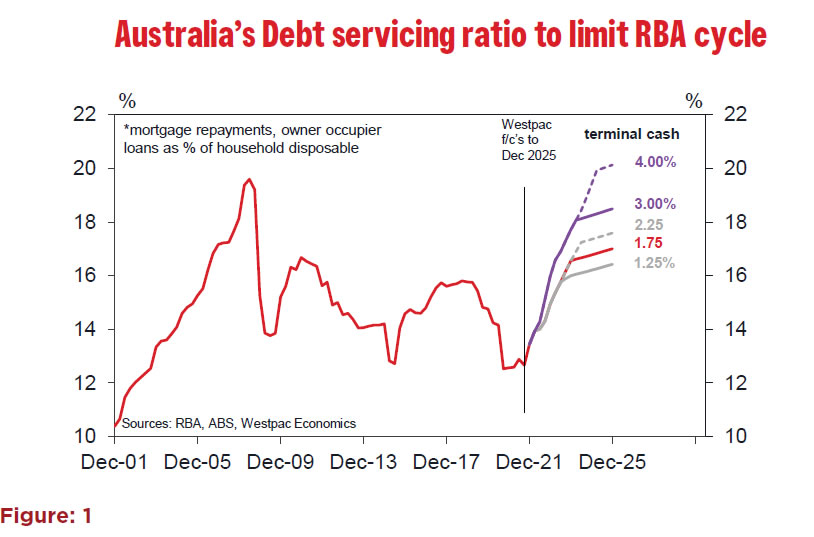

The lower nominal terminal rate which we, and others, favour relies upon the household sector being quite sensitive to rising rates due to their high levels of household debt.

We estimate that a terminal rate of 2% would see that debt servicing ratio settle above the ratios of the two previous cycles. Note that the “cycle” in 2017/18 was not driven by a rising RBA cash rate rather the banks’ responses to macro prudential tightening policies. (Figure 1).

There are significant uncertainties with this methodology.

- Are we taking adequate account of the evolving mix between fi xed and fl oating mortgages in this cycle?

- Is an “average” concept the right approach when change can be triggered by the marginal players?

- Perhaps every cycle is diff erent and it is more reliable to use the “compass” of an equilibrium “real rate” unless you are modelling the feedback eff ects from policy changes to the overall economy, including households, using some form of macro econometric model.

- How will the undeniable build up in the buff ers associated with the household savings rate averaging 17% in 2020 and 2021 aff ect the sensitivity of the household sector to higher rates?

These are all formidable questions.

Last week the Reserve Bank released its latest Financial Stability Review.

The Review included a detailed analysis of the Bank’s Securitisation data base. This data base covers detailed data on all securitisations of mortgages that have been implemented by banks and non banks. It does not cover the vast majority of mortgages which the banks do not choose to securitise and hold directly on their balance sheets.

Nevertheless, it is the most comprehensive publicly available record of the profile of mortgages in the Australian market.

Some important facts that we learn from the data base are that:

- The current stock of mortgages is 60% variable rate and 40% fixed rate. The fixed rate share has doubled since the pandemic when the RBA pushed 3 year bond rates down to 0.1% through its Yield Curve Control policy- allowing banks to offer 2–3 fixed rate mortgages at around 2%.

- Two thirds of fixed rate mortgages will need to be rolled over by end 2023.

- Mortgage borrowers have been accumulating their share of the lift in excess savings in their mortgage offset accounts; with the lift in mortgage offset balances being 2.5% of disposable income over 2020 and 2021 compared to around 1% in earlier years. As a result, the median excess payment buffer is 21 months – up from 10 months prior to the pandemic.

- Mortgage borrowers have also been increasing their repayments above the minimum level. We saw 65 basis points of RBA rate cuts in 2020 and savings increased over 2020 and 2021.

- Rising house prices and increased repayments mean that only 5% of loans have an LVR (loan to valuation ratio) of more than 75% compared to nearly 25% at the beginning of 2020.

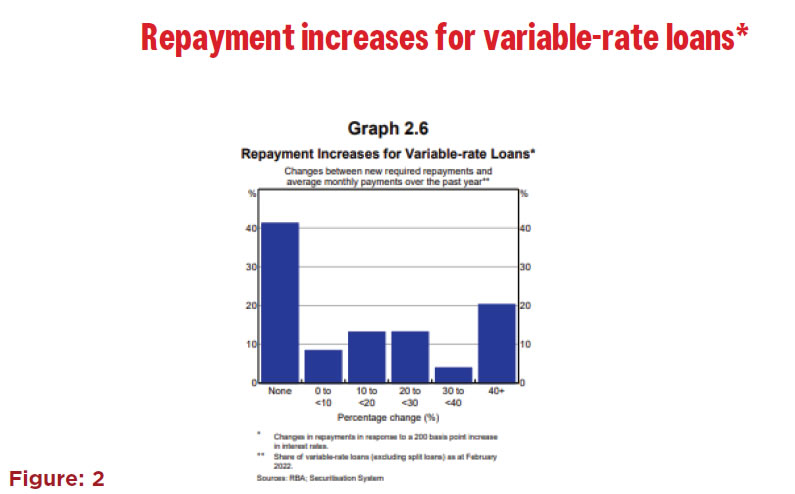

The data base lends itself to scenario analysis. The chosen scenario was a 200 basis point increase in the variable mortgage rate.

Under that scenario 40% of borrowers would face no increase in average monthly payments over the past year; 20% would see a lift up to 20%; 25% would see an increase up to 40%; and 20% would see an increase above 40%. (Figure 2)

Impacts on the economy are likely to reflect the responses of those borrowers who are hardest hit by the rate increases – the scenario analysis points to 20% of borrowers facing a 40%+ increase in repayments.

This scenario applies an immediate increase in the variable mortgage rate of 200 basis points whereas our central case is that the increase will be introduced over the 12 months beginning in June this year.

With the repayments over the last year being inflated by the high savings rate the actual proportional increase in repayments over the “normal” schedule will be higher.

Repayments include both principal and interest whereas the rate change will only affect the interest payments so the proportional increase in payments will be significantly less than the proportional increase in the actual rate.

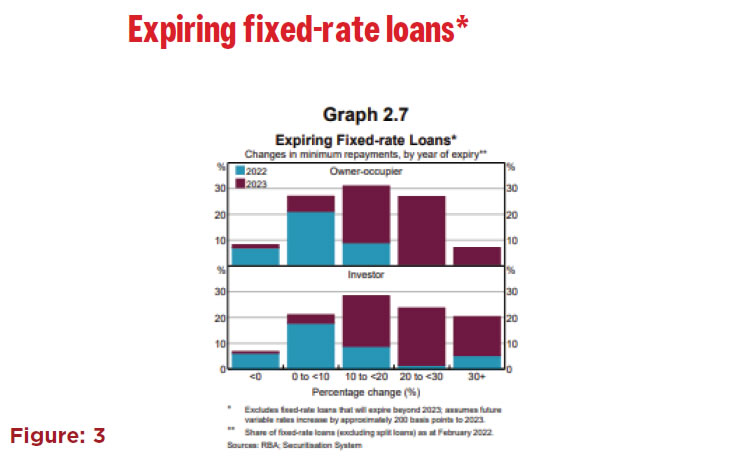

The scenario analysis results for fixed rate borrowers assumes that the borrowers move to floating rate at roll over date. (Figure 3)

For owner occupiers 65% would see a lift in repayments of less than 20% with around 50% for investors.

Of the remaining borrowers less than 10% (owner occupiers) would see an increase above 30% while 20% of investors would see the increase above 30%.

As discussed, the surge in fixed rate lending through 2020 and 2021 at an average of 2.4% during 2020 and 2021 saw fixed rate loans lift from 20% to 40% of the stock of loans.

Two thirds of fixed rate loans are set to mature by end 2023 and many of these would have been 2–3 year loans written at that 2.4% average during 2020 and 2021. Under the scenario analysis the loans roll over into floating rate loans at a loan rate of around 5.5% (reflecting the 2% lift in the standard variable rate).

With this in mind the results of the scenario analysis are surprisingly benign.

Perhaps the bulk of the 2.4% fixed rate loans mature after 2023. We are not expecting the RBA to be cutting rates in the 2024– 2025 period so the impact on the low cost fixed rate loans (which may represent the bulk of the one third of loans still to mature) would be delayed until 2024 and 2025.

As discussed in the introduction the data base does not cover the bulk of mortgages that are held directly on bank balance sheets. That observation that two thirds of fixed rate loans mature by end 2023 is important – a more front loaded profile of low rate borrowers transitioning to higher rates in 2023 would exacerbate the impact of higher rates in 2023. Only one major who has released that proportion of maturing fixed rates in their recent results and their number seems to line up quite closely with that two thirds estimate for the securitised portfolio.

Conclusion

This scenario analysis highlights the sensitivity of some borrowers to the 2% rate increase. But because it is a static analysis there is no consideration of the feedback effects on the wider economy to the borrowers.

The advantage of looking at earlier periods of rising rates is that the results capture those feedback loops.

The Review notes another RBA study which also simulates a 200 basis point increase in interest rates from current levels which would lower real housing prices by around 15% from current levels. With inflation running at the 2.5% RBA target over the simulation period that would imply a 10% reduction in nominal house prices over that two year period.

The scenario analysis is not built to assess the feedback effects of falling house prices on borrowers’ behaviour.

But the historical analysis will only provide limited insights into the big issue here which is how the accumulated buffers affect the behaviour of borrowers when rates are rising.

For example, concerns about falling house prices and rising rates might prompt borrowers to seek to preserve the buffers by cutting back on other expenditure.

And we do not know whether those buffers will be available to those borrowers in the vulnerable groups – 20% of variable rate borrowers will face a 40% lift in average repayments; the cohort of fixed rate borrowers who will move from a 2% fixed rate to 5.5% variable and the requirement to pay down principal and interest.

The RBA concludes “although the estimated increases in repayments are sizable for some borrowers it should be manageable for most.”

The ultimate terminal rate in this cycle will be determined by the availability of the buffers for those who need them most and the overall behaviour of those facing “sizeable” increases.

Because the static scenario analysis does not address so many of these issues we should treat it only as a helpful input into the discussion around the terminal rate rather than a definitive assessment.

We are comfortable to continue with the dynamic, historical approach which does at least take into account the feedback effects experienced in earlier cycles.

But with no historical precedents or any way of modelling the impact of the “buffers” there is considerable uncertainty about how the economy will evolve once the standard variable mortgage rate starts to rise.

{kind=link}