It’s been a stellar year for commodities as geopolitical turmoil and the pandemic have sparked a global supply crunch in industrial, energy and agricultural commodities. But whilst higher industrial commodity prices are a headache for manufacturers and the astronomical jump in food prices is worrisome, it is energy prices that are causing the most pain, especially for policymakers. However, there finally seems to be some reprieve as oil prices have pulled back substantially from this month’s peaks, threatening the upward formation that started in December. So is this just another dramatic correction, or is the tide finally turning for the oil rally?

Geopolitical tensions have been good for oil prices

There can be no question that the war in Ukraine and subsequent sanctions on Russian energy exports have been a boon for oil. The market was already tight enough as it is. OPEC has been easing its supply curbs extremely gradually, while the recovery in demand from economies around the world re-opening has exceeded expectations. With many OPEC members struggling to meet the higher output quotas due to various production constraints, the ban on Russian oil by Western nations couldn’t have come at a worst time.

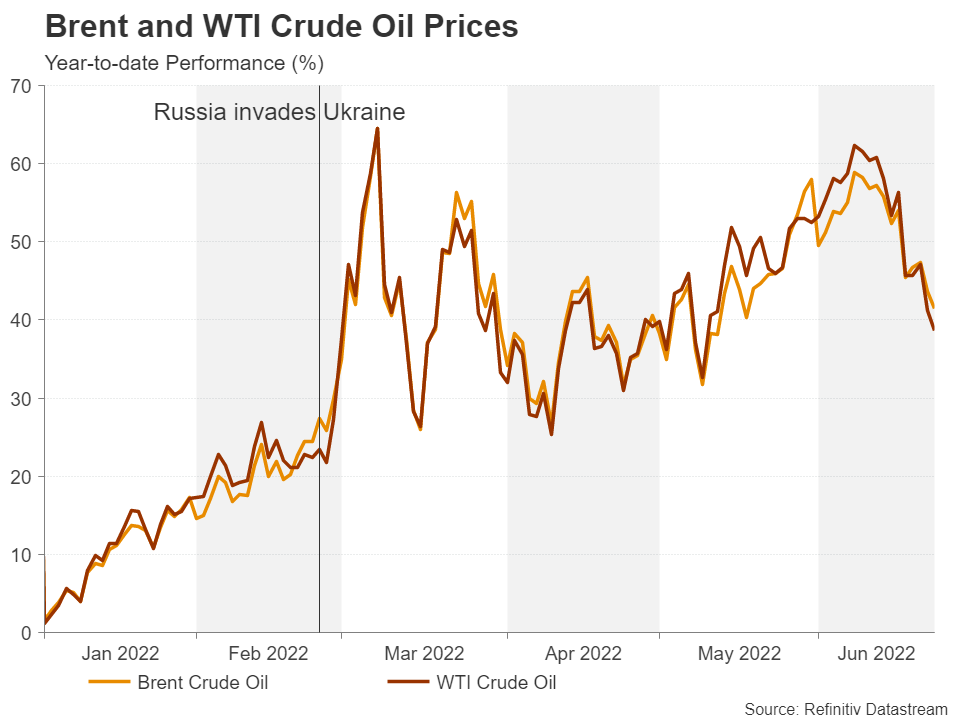

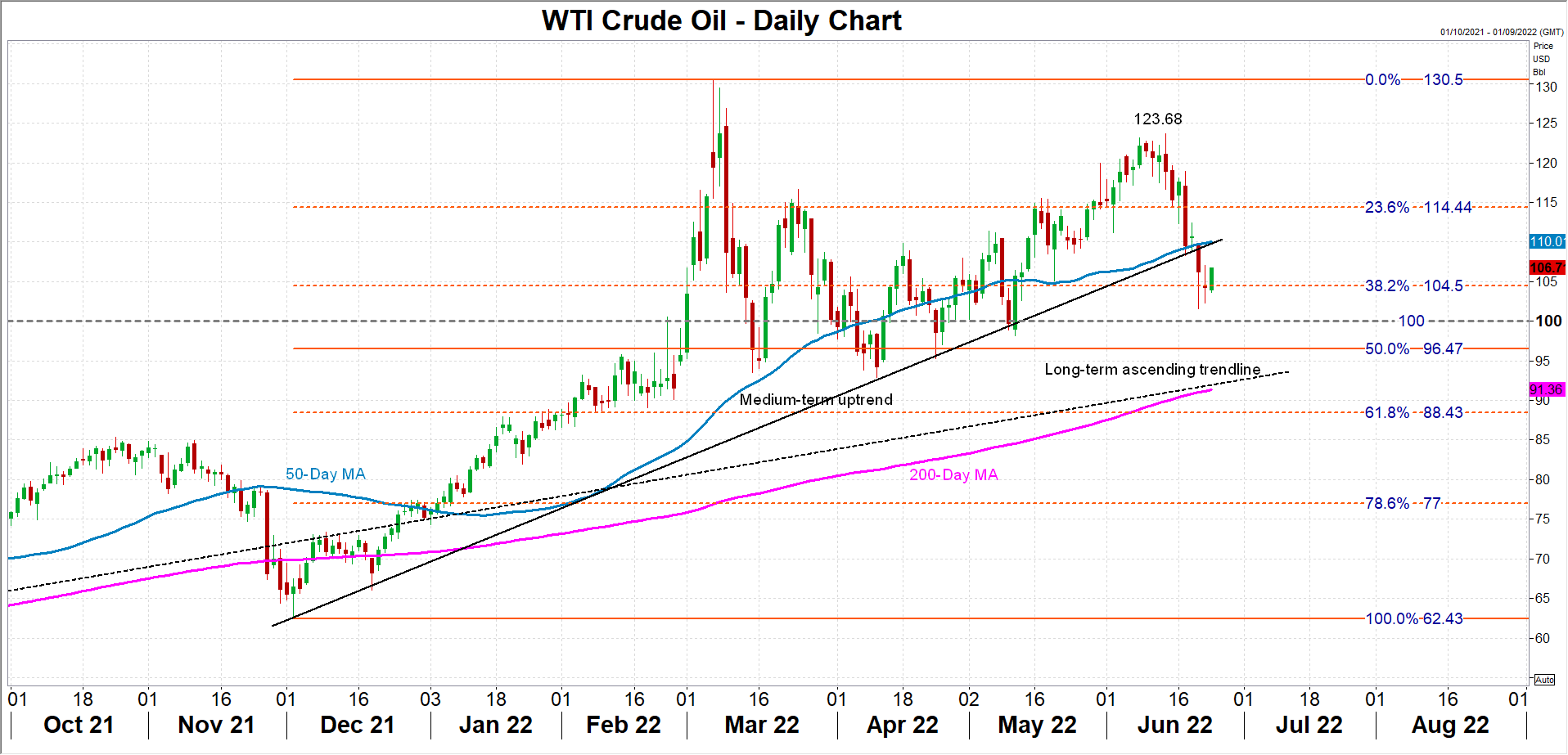

Oil prices have rallied by an incredible 40% so far in 2022, even after the recent dip. The gains stood at more than 75% at one point in March at the height of the Ukraine crisis. But this was followed by a sharp correction before prices began to head higher again. Up until now, the ascending trendline taken from the December low has successfully defended the rally, acting as a strong support, particularly in April and May when it was tested several times. And this is what’s different about the latest selloff.

A bearish signal?

WTI futures have broken below this crucial trendline, casting doubt about the rally’s prospects, at least in the short term. The broader uptrend that goes all the way back to the April 2020 crash is still intact. The question is, how far south will the current slide go?

After weeks of rising concern about oil shortages and supply likely getting even tighter, the outlook has unexpectedly started to deteriorate. Fears that central banks will tip their economies into a recession as they strive to get inflation under control are intensifying.

Demand outlook has become foggier

Inflation is skyrocketing everywhere and continues to surprise on the upside, defying predictions that it would have peaked by now. The surge in oil prices is mostly to blame for this, although the ongoing supply-chain disruptions are also a big factor.

With consumers feeling the squeeze not just from higher fuel prices but increasingly from price hikes across a broad range of goods and services, the International Energy Agency’s forecast that demand for oil would exceed pre-pandemic levels in 2023 might have been a little on the optimistic side. Should economies in Europe and North America end up in a recession before the year-end, the hit to demand would likely be even more significant.

All the talk of a recession alone is proving to be quite a drag on oil prices. But another headwind – a potentially bigger one – for the commodity is investors re-evaluating how tight the market really is. Although a raft of countries have imposed either restrictions or an outright ban on Russian crude, several large importers of energy are still buying from Russia.

Russian sanctions might not be working

Countries such as India and China are importing more oil from Russia than ever before, and Moscow has been rerouting its shipments to further afield in the face of embargos from its European neighbours. This adds an entirely different dimension to the thinking that millions of barrels of Russian oil would be taken off the market by Western sanctions. The picture that is emerging is that several Asian nations are switching to discounted Russian oil and buying less from Middle East producers, which in turn are now selling more to Europe, substituting the imports from Russia.

If recession risks continue to weigh on sentiment and more investors come to the realisation that the oil sanctions have only had a modest impact on global supply, the latest downside correction could go a lot deeper.

Is there more downside on the way?

WTI futures are hovering around the 38.2% Fibonacci retracement of the December-March uptrend at the moment. Another tumble would see the $100 a barrel mark being breached and the price would then test the defensive barrier formed by the 200-day moving average and the longer-term ascending trendline. If this support is broken too, the bullish structure would be eroded and the outlook would almost certainly turn neutral.

But oil has made a comeback before when it’s violated trend lines. The current upward stretch took off from the lows reached after the price fell beneath below the long-term uptrend line in late November. In the event of a rebound, the price is likely to stumble near $110 where the 50-day moving average is converging with the medium-term ascending line. Successfully overcoming this resistance would clear the path towards the June top of $123.68 and reinforce the positive outlook.

Recession worries vs supply constraints

There are several factors that could shift the oil narrative back to being about supply tightness. The White House is piling pressure on US producers to do more to boost output and President Joe Biden will be travelling to Saudi Arabia next month to convince his counterpart to do the same. If these efforts prove to be in vain, and moreover, fears of a recession do not materialize, the prospect for oil would be very bullish.

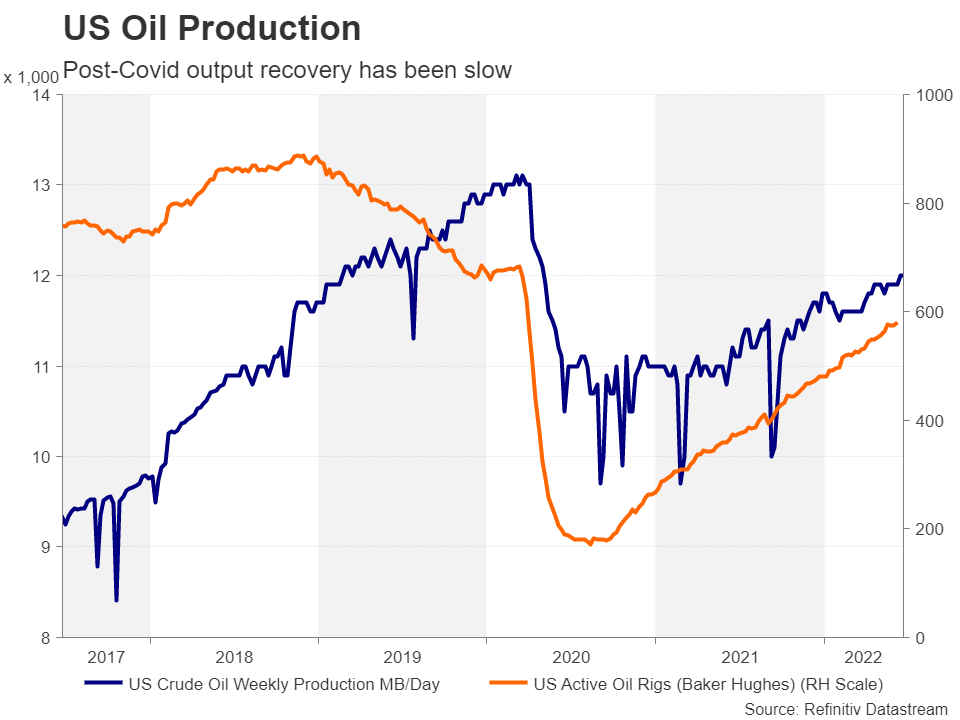

But as things stand, the negative risks are slightly greater. Slowly but surely, global oil production is returning to pre-pandemic levels, even with the sanctions on Russia and the absence of an Iranian nuclear deal, and near-term demand is being disrupted by China’s zero-Covid policy as well as the travel chaos in the airline industry due to staff shortages.

It’s worth pointing out that the situation in Ukraine remains highly volatile and a fresh crisis could easily trigger another jump in energy prices. But unless recession jitters start to recede over the coming weeks or months, it will be difficult for oil prices to hold onto their post-Covid upward trajectory and the chances of a new consolidative phase would increase.

{kind=link}