EUR/USD: Parity 1:1 Achieved

What we’ve been talking about over the last few months has come true: the EUR/USD hit 1.0000 on Tuesday, July 12. The local bottom was fixed on Thursday July 14 at 0.9951. The last time the pair was so low was in December 2002. Note that the dollar strengthened not only against the euro, but also against other leading world currencies. The DXY index is also in the zone of 20-year highs, having approached the height of 108.99 on July 14.

The greenback’s rally was spurred on by recent US inflation data. The consumer price index (CPI) reached 9.1% in June, exceeding the forecast of 8.8%. Note that this was observed only 12 times in 110 years, and the last time inflation rose above 9% was in 1981. This record (rather an anti-record) strengthened market expectations regarding the pace of tightening monetary policy (QT) by the US Central Bank. If earlier it was assumed that the rate would be increased by 50-75 basis points at the next meeting of the FOMC (Federal Open Market Committee) on July 27, there is talk now that federal funds costs may increase immediately by 100 bp. The probability of such a move is estimated by analysts at 82%, and the probability that the rate will be raised by a total of 175 basis points at the two upcoming meetings is 75%, according to CME Group FedWatch.

Atlanta Federal Reserve Bank (FRB) President Rafael Bostic dismissed the possibility, adding that inflation could rise even further by the end of the year, requiring the Fed to act even more decisively. According to experts, the desire of the US Central Bank to stop inflation at any cost may lead to the fact that the rate will eventually reach 4.00% (it is 1.75% at the moment). And this will be done even though the country’s economy may fall into the deepest recession.

What is good for the dollar is bad for the stock market. Flight from risky assets intensified amid market fears about a prolonged economic downturn. S&P500, Dow Jones and Nasdaq fell down, while DXY flew up. Data on retail sales in the US, which were released on Friday evening, July 15, slowed down the flight. With a previous reading of -0.1% and a forecast of 0.8%, this figure reached 1.0% in June, which pushed the EUR/USD pair up and finished at 1.0082.

It should be noted that the tightening of the Fed’s monetary policy creates problems not only for the US economy, but also for the entire global economy. The share of the US dollar in international reserves was 59% at the end of 2020, and the share in international settlements as of February 2022 reached 39%. Thus, the dollar is both the main reserve currency and the main means of payment in the world. With its strengthening, the burden increases primarily on emerging market economies that have received large loans from the IMF. Debt service difficulties have already led to a default in Sri Lanka, problems await El Salvador, Tunisia, Egypt, Pakistan, and Ghana.

The popularity of the dollar as a defensive asset will continue to grow with the approach of a recession and thanks to the policy of the US Federal Reserve. At the time of writing the review, on the evening of July 15, this forecast is supported by 60% of experts. Further correction to the north is expected by 30%, and 10% of analysts have given a neutral forecast. The oscillator readings on D1 give a completely unambiguous signal: all 100% are colored red. There are 85% of those among the trend indicators, the remaining 15% have taken the opposite position.

The closest strong support for the EUR/USD pair is the 1.0040-1.0050 zone, followed by the 1.0000 level. After it is broken, the bears will target the July 14 low at 0.9950, even lower is the strong 2002 support/resistance zone. 0.9900-0.9930. The nearest serious target of the bulls is a return to the zone 1.0350-1.0450, then there are zones 1.0450-1.0600 and 1.0625-1.0770. There are several levels on the way to 1.0350, which the pair broke very easily during the fall, so it is still difficult to determine which of them can become a serious obstacle when moving up.

The highlight of the coming week will undoubtedly be the ECB meeting on Thursday July 21. It is expected that the regulator will raise the interest rate from 0.0% to 0.25%. Such a move could support the euro a little, although it looks rather timid against the backdrop of the Fed’s hawkish policy. Of undoubted interest are the subsequent press conference and comments of the ECB management, which should give the market an idea about the future plans of this regulator.

Other events include the publication on Tuesday, July 19 of the Consumer Price Index (CPI) and the report on bank lending in the Eurozone. Data on the labor market and manufacturing activity in the US will be released on Thursday, July 21, and the value of the PMI (Purchasing Managers Index) in the manufacturing sector in Germany will become known the next day. In addition, we advise you to pay attention to the decision of the People’s Bank of China on the interest rate on July 20. This decision is especially interesting, since China’s GDP in the Q2 2022. decreased by 2.6% against the forecast of a decrease by 1.5%, which indicates the approach of the country’s economy to a recession.

GBP/USD: The Battle for 1.2000 Is Lost, But It’s Not Over Yet

The GBP/USD pair, unlike the EUR/USD, has not yet broken a multi-year record, but is already close to it. The local bottom was fixed at 1.1759 last week, and the last chord of the five-day period was set at 1.1865. Below are two serious targets: 1.1409, the collapse point caused by the start of the COVID-19 pandemic in March 2020, and the December 1984 low of 1.0757. We think it’s too early to talk about the parity of the pound with the dollar 1:1.

The macro data released on Wednesday July 13 turned out to be unexpectedly green. Thus, the UK GDP (yoy) with a forecast of 2.7% in reality amounted to 3.5%, while the June GDP, with the previous value of -0.2% and the forecast of 0.1%, rose to 0.5%. Despite this positive, the factors of pressure on the country’s economy have not gone away. Among them are problems related to Brexit and the customs conflict between Britain and Northern Ireland. Inflation remains the highest in 40 years, and it is possible that it could exceed 11% by November, pushing the economy into a deep recession. We must add the government crisis that caused the resignation of Prime Minister Boris Johnson to all this, as well as the difficulties associated with sanctions against Russia due to its armed invasion of Ukraine.

Despite statements from BoE officials that they are ready to accept a faster pace of monetary tightening, in reality the regulator is acting more cautiously than the market expected. The current interest rate is 1.25%, which is lower than the corresponding Fed rate (1.75%), and the next BOE meeting will take place only on August 04, 2022. And this cannot but exert downward pressure on the GBP/USD pair.

At the moment, 50% of experts believe that the British currency will continue to lose ground, 25% on the contrary expect a rebound upwards, and 25% have taken a neutral position. The readings of the indicators on D1 are as follows. Among the trend indicators on D1, the power ratio is 100:0% in favor of the reds. Among the oscillators, the advantage of the bears is slightly less: 90% indicate a fall, the remaining 10% have turned their eyes to the north.

The nearest support is at 1.1800, followed by the July 14 low of 1.1759. Further, 1.1650, 1.1535 and March 2020 lows in the 1.1400-1.1450 zone. The immediate task of the bulls is to rise to the 1.1875-1.1915 zone, and then a new stage of the battle for 1.2000, which they ingloriously lost last week. In case of victory, the pair will meet resistance in the zones and at the levels of 1.2100, 1.2160-1.2175, 1.2200-1.2235, 1.2300-1.2325 and 1.2400-1.2430.

As for the macroeconomic calendar for the United Kingdom, we advise you to pay attention to Tuesday July 19, when data from the UK labor market arrives. The speech of the head of the Bank of England Andrew Bailey is scheduled on the same day. The value of the Consumer Price Index (CPI) will become known on Wednesday, July 20, and a whole package of data regarding the state of the British economy will be received on Friday. It will include retail sales data for June, as well as data on business activity (PMI) both in individual sectors and in the country as a whole.

USD/JPY: The Storm After the Calm

We called the previous review “The Calm Before the Storm” as USD/JPY did not renew its 24-year high for the first time in five weeks and took a breather. But since a storm was promised, it must break out. A new high at 139.38 was recorded on July 14, and the pair met the end of the trading session at 138.50.

The reason for the new weakening of the yen is the same: the difference between the hawkish monetary policy of the US Federal Reserve and the ultra-dove one of the Bank of Japan (BOJ). By the way, the next meeting of the Japanese Central Bank is to be held next week, on Thursday, July 21, at which it is likely to once again leave the interest rate unchanged at the negative level of -0.1%.

If we usually talk about the fight between bulls and bears, then regarding the future of the yen, the fight is between… analysts and BOJ. The former, for the most part, are waiting for the Central Bank to finally change its policy, and therefore stubbornly vote for the strengthening of the yen. The latter, no less stubbornly, leaves this policy unchanged, and the USD/JPY pair stubbornly moves up.

This time, only 40% of experts speak about the pair’s movement to the height of 142.00. The remaining 60% hope for a downward trend reversal. There are no such disagreements in the readings of indicators on D1: all 100% of trend indicators and oscillators are looking north, although 20% of the latter are in the overbought zone. Supports are located at the levels and in the zones 137.65, 137.00, 136.60 135.50-135.70, 134.00, 133.50 and 133.00. The bulls’ targets are 140.00 and 142.00. And if the pair’s growth rates remain the same as in recent months, it will be able to reach the 150.00 zone in late August – early September

Apart from the meeting of the Japanese Central Bank and the subsequent press conference of its management, there are no other significant events expected in Japan this week.

CRYPTOCURRENCIES: The Beginning of the End of the Bear Phase

The previous review drew attention to an anomaly when both the dollar and the US stock indices – S&P500, Dow Jones and Nasdaq were growing at the same time. Things fell into place last week: the US currency continued to grow, and the indices fell down. It should be noted to bitcoin’s credit that, despite another wave of investor flight from risks, it managed to stay in the $20,000 zone. Now, how long will it last?

CEO of Rockefeller International, who previously held the post of chief strategist at Morgan Stanley, Ruchir Sharma, recalled that a bearish trend usually lasts about a year in the stock market, and stock exchanges indices are falling by 35%. At the moment, the market has decreased by only 20%. So we can expect a further drop in demand for risky assets including bitcoin in the next six months.

“I would not say that we are already at the bottom,” Sharma said, adding that bitcoin will return to growth and reach new highs after the end of the bear cycle. The financier recalled the situation with Amazon in the early 2000s, during the dot-com bubble, when the retailer’s share price collapsed by 90%. However, stocks then bounced back, and rose another 300 times over the next 20 years.

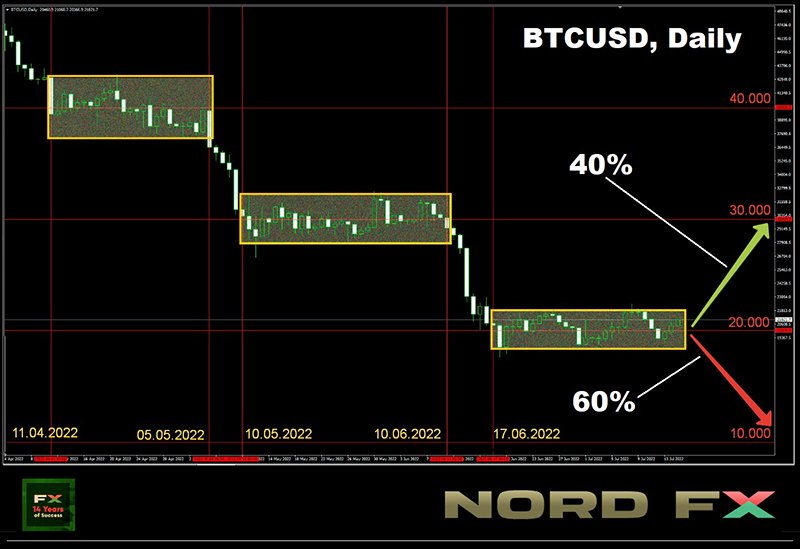

If you look at the BTC/USD chart, it’s easy to see that the flagship currency has been clinging to round levels lately. So, bulls and bears fought for $40,000 from April 11 to May 5. The front line was at $30,000 from May 10 to June 10. The battle has been taking place in the $20,000 zone since mid-June. At the moment, 60% of investors surveyed by Bloomberg consider another decline in the price of bitcoin more likely, this time to $10,000. The remaining 40% are waiting for a recovery to $30,000. The study involved 950 respondents. Compared to institutions, there were more skeptics among retail investors. Almost every fourth called the first cryptocurrency “garbage” (18% of professional market participants).

Galaxy Digital CEO Mike Novogratz said in an interview with CNBC that he does not believe in the possibility of reducing the price of the first cryptocurrency to $13,000. “There is a feeling that we are 90% over this deleveraging. […] The problem is that further growth requires more faith and new capital,” he said. According to Novogratz, the sideways trend of digital assets will last until the US Federal Reserve stops raising the base rate, which will take about 18 months.

Macroeconomics expert Lyn Alden made a similar point. She believes that although there are no clear bullish signals in the crypto market, the time for global capitulation has already passed. In her opinion, the worst part of the bearish trend ended along with the unstable first half of 2022. The macro strategist believes that bitcoin can recover as the massive BTC sell-off has stopped.

However, Alden warns that bitcoin could still go down one step. “Macroeconomically, there are still not many bullish catalysts at the moment, and I would not rule out further price movement down.” “We have seen that, for the most part, bitcoin is very strongly correlated with the growth of the money supply, especially in dollars. So, when we have had a huge increase in the money supply around the world over the past couple of years, bitcoin has also done very well,” explained Alden. 1Now the reverse is happening as the US Federal Reserve and other central banks try to tamp down inflation. This, accordingly, affects the price of the cryptocurrency. In other words, now that the flow of cheap liquidity has dried up and interest rates are rising, investors prefer not to get involved in risky assets.

Some experts prefer to call what is happening in the crypto market not a collapse, but simply another deep correction. In addition, referring to historical data, they declare entering the final phase of a bear market. So, at the end of 2018, the total drop was 84% from the previous historical maximum. The BTC/USD pair has currently fallen from the November 11, 2021 high by only 71%. Thus, if we follow this model, we can expect the completion of the correction in the region of $10,000-11,000, and the subsequent consolidation may last about a year or more.

According to Glassnode, market shrinkage has virtually eliminated the rest of the “market tourists” from the game, leaving only hodlers “at the front”. On average, unrealized losses of each of them are now 33%. This is not the worst indicator in history, which also suggests that the final bearish phase has just begun.

The start of the final phase is also signaled by the capitulation of the miners, which has a high correlation with the bottoming of bitcoin. Most of the public mining companies used to expand their production with loans. Now their earnings have dropped to 50%, forcing them to sell off their coin holdings to cover operating and borrowing costs. Glassnode estimates that miner inventories are now around 70,000 BTC worth about $1.3 billion. And in the event of a prolonged consolidation, they will also be forced to put them on sale, which will put additional pressure on the market.

Please note that in this case, we are talking only about the beginning, and not about the end of the final phase of the bearish trend. Thus, the surrender of miners in 2018-19 lasted four months, while the current cycle lasts a little more than a month.

As for Ethereum, the dynamics of the ETH/USD pair quotes almost repeats the dynamics of BTC/USD. Some experts do not exclude its temporary rise to $1,280, however, they believe that this will be another trap for the bulls. And the pair will return to the $1,000 zone after its triggering. The next target of the bears is $500.

Returning to the Bloomberg survey, most of the 950 investors surveyed expressed confidence in the strong position of bitcoin and ethereum over the next five years. In their opinion, developments in the crypto market will prompt regulators to tighten supervision over the industry. This can increase trust and lead to further popularization of digital assets. Ruchir Sharma of Rockefeller International also believes that top cryptocurrencies will become much more stable within three to five years, which will allow them to seriously push the US dollar.

As of this writing (Friday evening, July 15), bitcoin is trading in the $20,900 zone. The total capitalization of the crypto market is $0.945 trillion ($0.966 trillion a week ago). The Crypto Fear & Greed Index has dropped 5 points over the week from 20 to 15 points and is still in the Extreme Fear zone.

{kind=link}