Summary

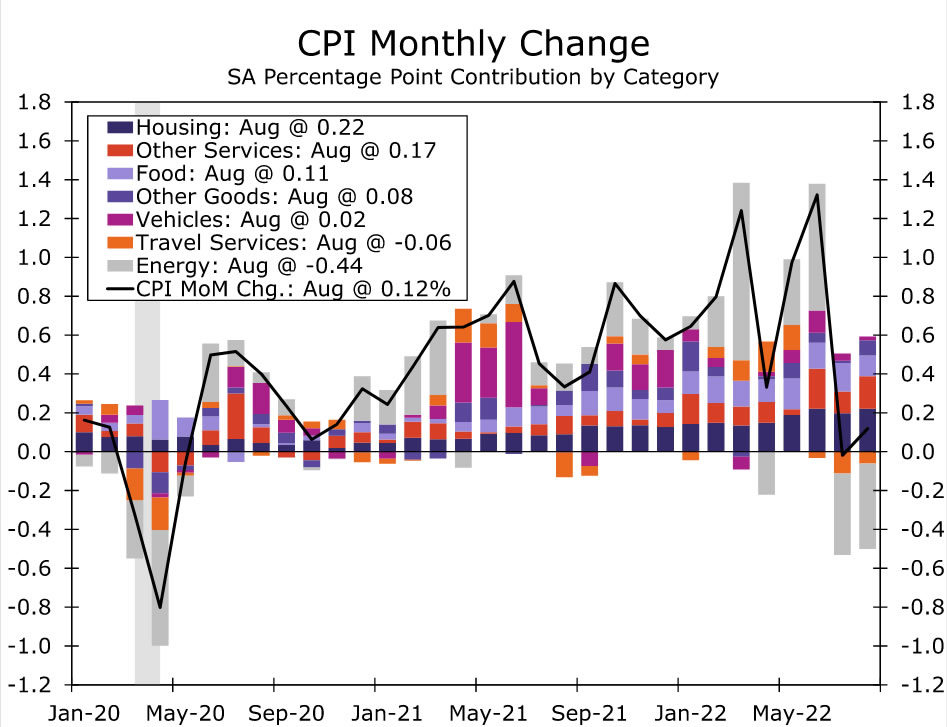

The Consumer Price Index increased 0.1% in August, but the modest gain for the headline index masked what was a disappointing report. Gasoline prices fell 10.6% in the month, helping to keep overall inflation in check, but beyond energy goods there were not many encouraging takeaways. Excluding food and energy prices, core inflation increased 0.6%, well above the Bloomberg consensus of 0.3%. Core goods inflation remained strong and broad-based despite indications that supply chains are functioning more smoothly and inventory stockpiles are building. Core services inflation also remained hot, increasing 0.6% in August.

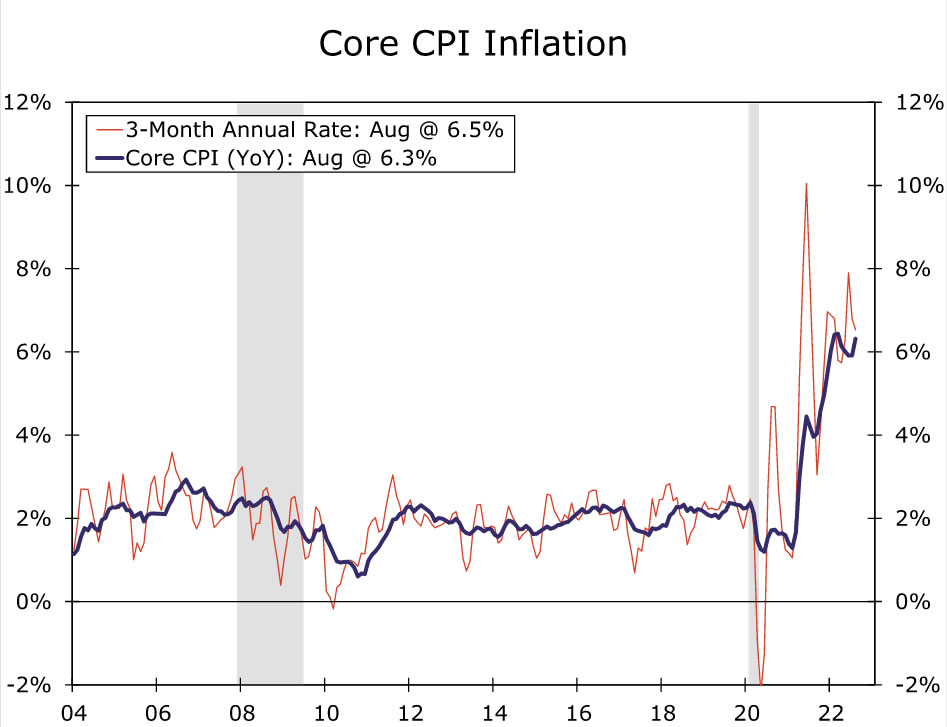

Of course, declining gasoline prices and moderating food price inflation are welcome developments. But through the noise, inflation remains a long way off from 2% over a sustained period of time. Over the past three months, the core CPI has advanced at a 6.5% annualized pace, more than triple the Fed’s 2% inflation target and above the 6.3% increase seen over the past 12 months. A 50 bps rate hike at next week’s FOMC meeting now seems like a distant pipe dream, with a 75 bps rate hike now all but assured.

Slower Inflation, but Still Disappointing

The Consumer Price Index increased just 0.1% in August, but the tepid gain was stronger than the Bloomberg consensus expectation for a -0.1% decline in consumer prices. August’s small increase in prices helped lower the year-over-year rate of price growth to 8.3%—a welcome but still insufficient step in relieving excruciatingly high inflation for Americans.

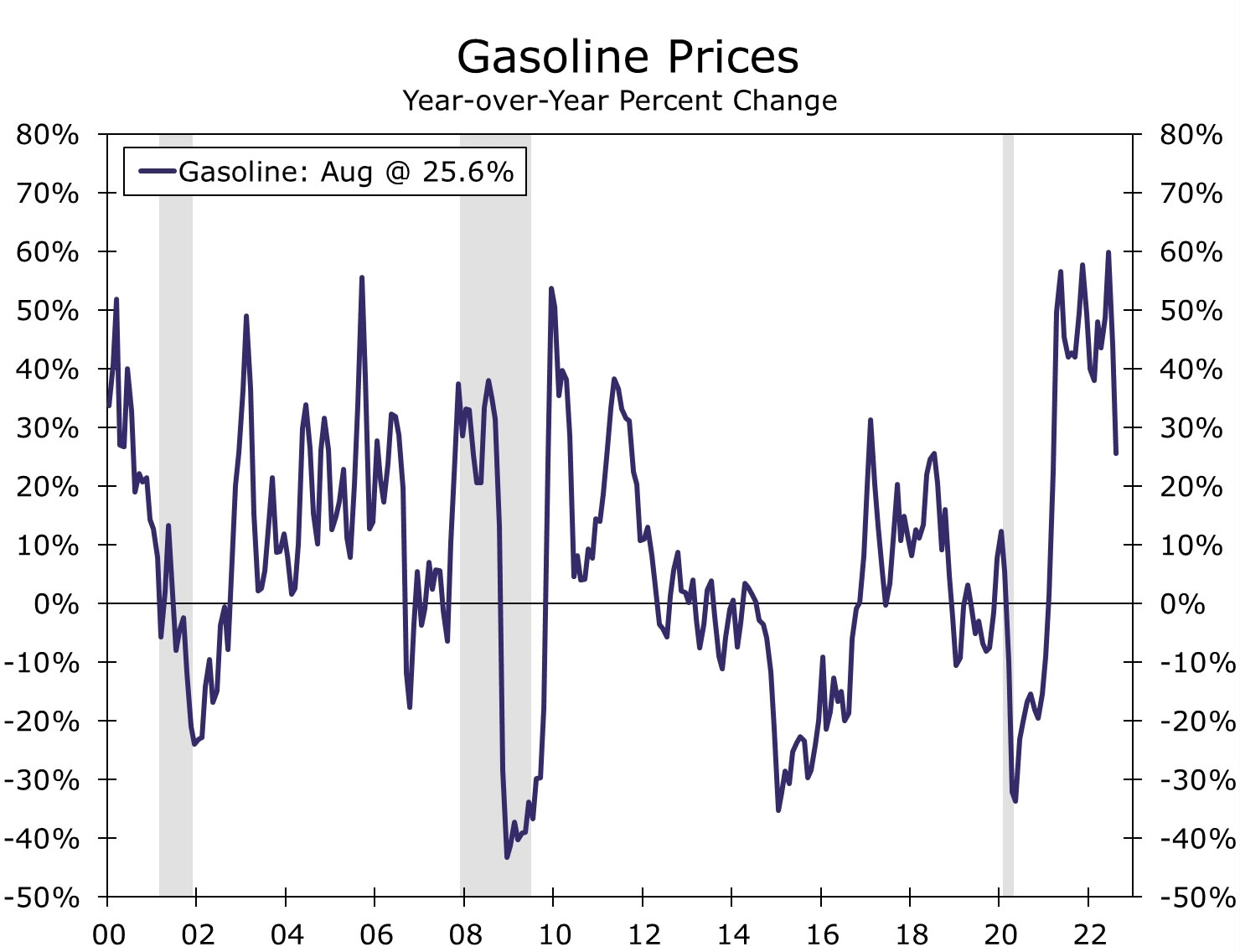

As expected, energy goods were a major driver of August’s softer print. Gasoline prices fell 10.6% in August and are now “only” up 25.6% year-over-year. Energy services rose 2.1% on the back of higher electricity and utility gas prices. Food inflation eased slightly, increasing 0.8% in August and marking the slowest pace of price growth for food this year. That said, a 0.8% monthly increase in food prices will hardly be considered a victory by consumers. Prices at the grocery store check out counter are now up 13.5% year-over-year, the biggest increase since February 1979.

Meanwhile, the core index showed that price pressures remain strong and broad-based. Excluding food and energy, prices rose 0.6%, surpassing even our above-consensus estimate for a 0.4% increase. Lower commodity prices, signs of supply chains functioning more smoothly and greater inventory levels have done little to ease core goods inflation, which rose 0.5% in August. Despite declining auction prices, used vehicle prices are hanging in there, dipping just 0.1% in August, while new vehicle prices continue to rise at a pace unthinkable over the past two decades (up 0.8% last month). Prices for goods remain sticky beyond the particularly supply-constrained auto sector. Household goods, apparel, medical and recreational goods prices all rose in August.

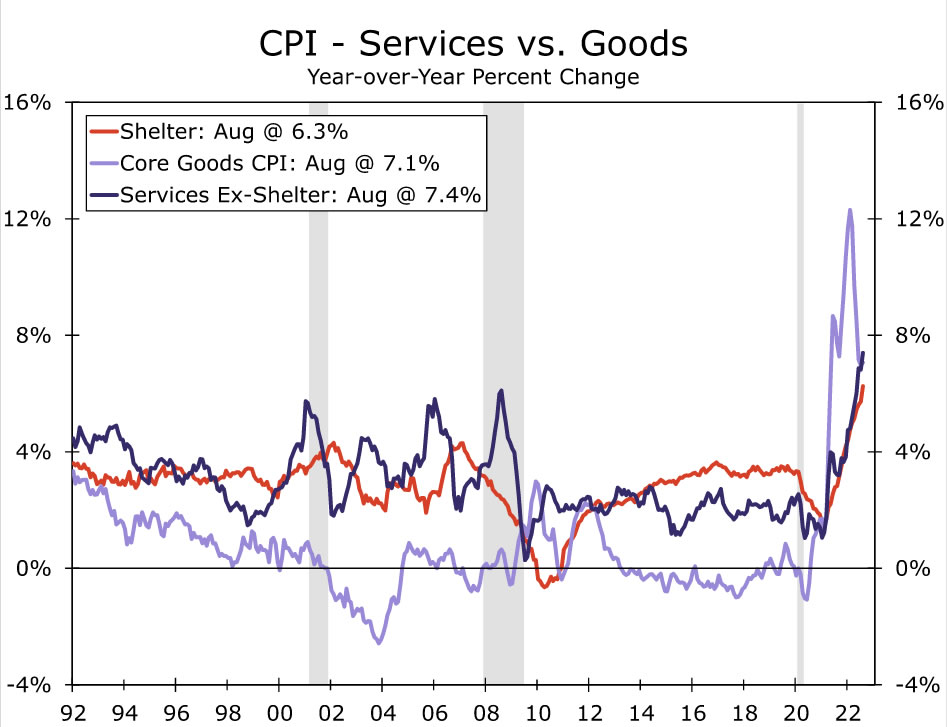

Relief on services inflation was always going to be a harder ask than for goods at this stage of the cycle, and here too price growth picked up in August. Notably, the 0.6% rise in core services was driven in large part by stronger shelter inflation. Both primary rent and owners’ equivalent rent rose 0.7%, with the latter posting the largest monthly gain since 1990 (0.71%). While private sector measures of rent growth suggest the corresponding CPI categories may be close to peaking on a monthly basis, the slow-moving nature of primary rent and OER in the CPI data suggest housing will continue to provide a sizable boost to core inflation in the coming months. At the same time, price growth for other services like medical care, insurance, tuition and personal care continue to press ahead at a strong rate, underscoring the inertia inflation continues to carry. One of the few spates of good news for services inflation came from a 4.6% drop in airfares last month, although that still leaves the cost of a plane ticket up 33% over the past year.

Another 75 bps Rate Hike Likely Coming Next Week

At this point, any slowdown in inflation is encouraging for the outlook. Declining gas prices and a modest slowing in food price inflation should help keep inflation expectations in check and boost consumer purchasing power. Some categories such as used auto prices continue to gradually normalize, while easing constraints across supply chains and softening in the housing/rental market look promising for further moderation ahead.

That said, there remains considerable ground to cover before getting inflation back to a pace that resembles the Fed’s target. Over the past three months, the core CPI has advanced at a 6.5% annualized pace, more than triple the 2% target. Moreover, a sustained return to 2% inflation remains even more distant at present. The tight labor market has kept compensation, the largest cost for most businesses, advancing well above 2% (even after accounting for productivity growth), while consumer and business inflation expectations remain high relative to the range of recent decades. We think the road to returning inflation to target is still a long one, and we continue to look for the FOMC to press ahead with another 75 bps point hike at its meeting next week.

{kind=link}