U.S. Highlights

The labor market cooled modestly in December, with 223k new jobs added and the unemployment rate ticking back down to 3.5%.

The House of Representatives failed to elect a Speaker of the House on the first ballot for the first time in 100 years, delaying the start of the new legislative session in the lower chamber of Congress.

FOMC minutes from the December meeting underlined the hawkish stance of the committee and warned of the dangers of a pre-mature easing of financial conditions.

Canadian Highlights

- Oil prices slid heavily this week, greased by demand concerns as the world’s second largest consumer, China, struggles through its worst battle with COVID yet.

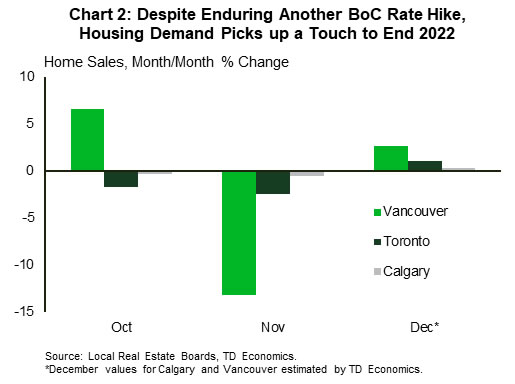

- The impact on housing demand from the newly implemented foreign buying tax should be modest. This week also revealed that, even with BoC rate hikes, housing demand picked up in key markets last December.

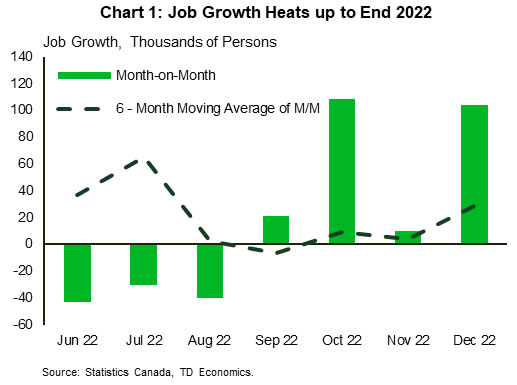

- It was a joyous December for job seekers, as employment surged by 104k in the month. The barn-burner report likely swings the pendulum in favour of further action by the BoC.

U.S. – Plenty of Jobs, Except in Congress

The start of the new year kicked off with several important December data releases, including an update on the labor market and FOMC meeting minutes. In addition, the new Congressional session got off to a rocky start, with the House of Representatives unable to elect a Speaker of the House. Equity markets fluctuated on the week with the S&P 500 down 0.4% while yields declined sharply, with the 10 Year Treasury at 3.58% as of the time of writing.

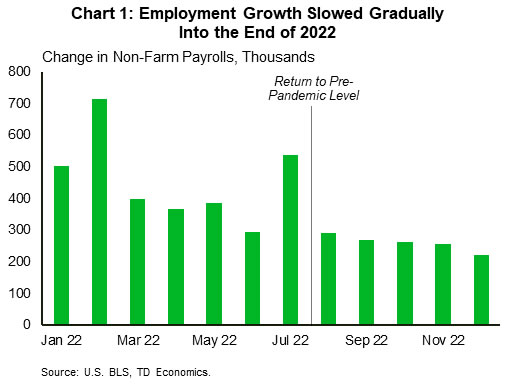

The exceptional strength seen in the jobs market over the past two years slowed into the end of 2022, with December adding 223k new jobs and bringing the annual total to 4.5 million (Chart 1). The labor market remained tight with the unemployment rate declining back to 3.5% as the labor force rose by 0.3% and the participation rate ticked up by 0.1 percentage-points. Average hourly earnings growth decelerated to 0.3% month-on-month, inciting an initial rally in equity markets as participants looked for evidence which might lead to a reprieve from the current aggressive round of rate hikes. The report also showed a notable uptick in the number of multiple job holders reflecting the weight of inflation and rate hikes on households as they seek additional support through secondary incomes.

Earlier in the week, manufacturing data showed signs of further slowing, with the ISM manufacturing purchasing managers’ index (PMI) slipping further into contractionary territory in December (Chart 2). After two years of growth the industry has begun to give back some of its gains, in large part due to the direct and indirect effects of higher rates. We also saw this play a part in the ISM Services PMI which declined sharply and showed the sector contracting in December for the first time in 30 months. Within the services index, declines were led by new orders which dropped sharply by over 10.8 percentage-points relative to November. On a more positive note, the manufacturing report showed a continued decline in supply price pressures and improving delivery times, which will be welcome news for the Federal Reserve.

FOMC meeting minutes released on Wednesday unsurprisingly echoed earlier sentiments expressed by Chair Powell at his December 14th press conference. Members pushed back against the loosening of financial conditions seen in recent months on the back of softer inflation reports, noting that “an unwarranted easing in financial conditions…would complicate the committee’s effort to restore price stability”. The minutes reiterated that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path”, and this was further emphasized by the fact that no committee members foresee cutting rates this year.

Minneapolis Fed President (and 2023 FOMC member) Neel Kashkari also released an essay on Wednesday in which he noted the need to raise rates by another 100bps this year, which helped to briefly push the odds of a 50bps hike in February close to 50%, though they have since declined back to roughly 25%. Next week we will get December CPI data which will help clarify whether the recent downturn in inflation persisted into the end of the year.

Canada – You’re Hired

The first week of the new year turned out to be a tough one for oil markets. Indeed, the WTI benchmark was down about $5/barrel (as of writing), greased by demand concerns as the world’s second largest consumer, China, struggles through its worst battle with COVID yet. For their part, bond yields are tracking lower on the week, even with this morning’s barn-burner of a jobs report.

Hiring blew away expectations to end 2022, as a meaty 104k positions were added in December (Chart 1). Adding to the strong tone of the report was the fact that gains were concentrated in full-time, private sector positions. In addition, hiring spanned several industries and provinces. The unemployment rate also dipped to 5%, near an all-time low. Less eye-popping was the pedestrian 0.1% month-on-month gain in hours worked. Wage growth also decelerated in year-on-year terms but remained hot at 5.1%.

In its December interest rate announcement, the Bank of Canada communicated that it would be considering whether the policy rate needs to move higher, after hiking rates at a very rapid pace in 2022. The jobs report certainly swings the pendulum towards further action on rates. Our current forecast calls for the Bank of Canada to hike their policy rate by 25 basis points at its upcoming meeting in late January.

Developments in Canadian housing markets also made headlines this week, with several prognosticators stepping forward to deliver their views on housing for 2023. Our take is that another subdued year for activity is in the cards, although housing should find its bottom. Conditions are already soft in most markets across Canada, and some further near-term impact should come from the new two-year ban on foreign homebuying that came into effect on January 1st. However, we think the impact on demand won’t be overly significant for a few key reasons. First, existing foreign buying taxes in Ontario and B.C. have already drained much of this demand from these markets. In addition, there are several exemptions to the ban, including for foreign students and temporary workers who have been in Canada for some time.

This week also offered a glimpse on how key housing markets performed in December. As it turns out, the story was more “ho, ho, ho” than “bah, humbug”, at least from an economic growth perspective. Indeed, after several months of weakness, home sales increased month-on-month in Toronto, Calgary, and Vancouver (Chart 2). Average prices, meanwhile, were flat in Toronto for the 3rd straight month. Importantly, new supply in all three markets declined. More broadly, there have been no signs so far that the high interest rate backdrop has resulted in forced selling, although that remains a key risk. All told, Canadian housing markets entered this year on a better-than-anticipated footing, although the backdrop is still quite weak.

{kind=link}