Summary

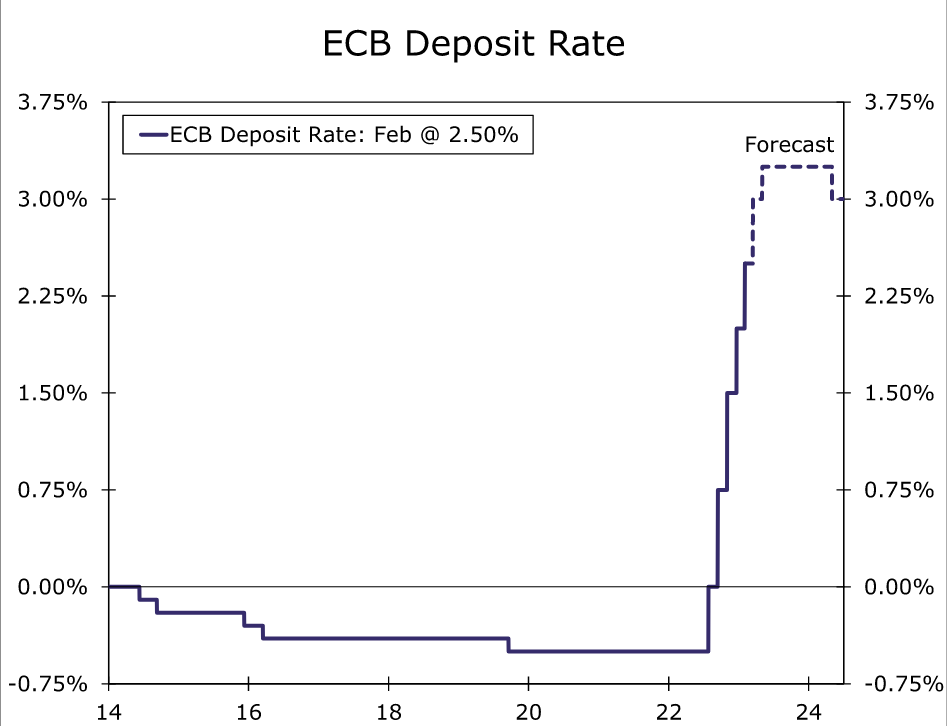

- The European Central Bank (ECB) delivered a 50 basis point increase in its Deposit Rate at today’s monetary policy announcement, and offered a relatively determined message to continue along its monetary tightening path. In particular, the ECB pre-committed to another 50 basis point increase in March, a somewhat unusual move, and said it would keep interest rates at restrictive levels for some time.

- Today’s announcement does not alter our outlook for the path of ECB monetary policy. We expect a further 50 basis point increase in the Deposit Rate in March and a final 25 basis point increase in May, which would see the ECB’s Deposit Rate peak at 3.25% for the current cycle.

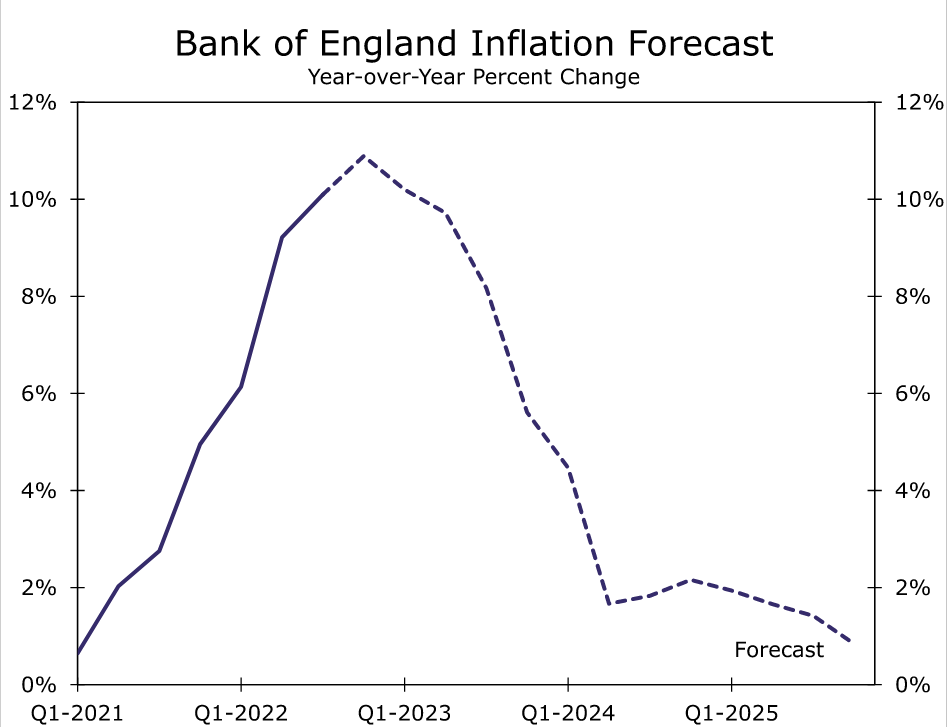

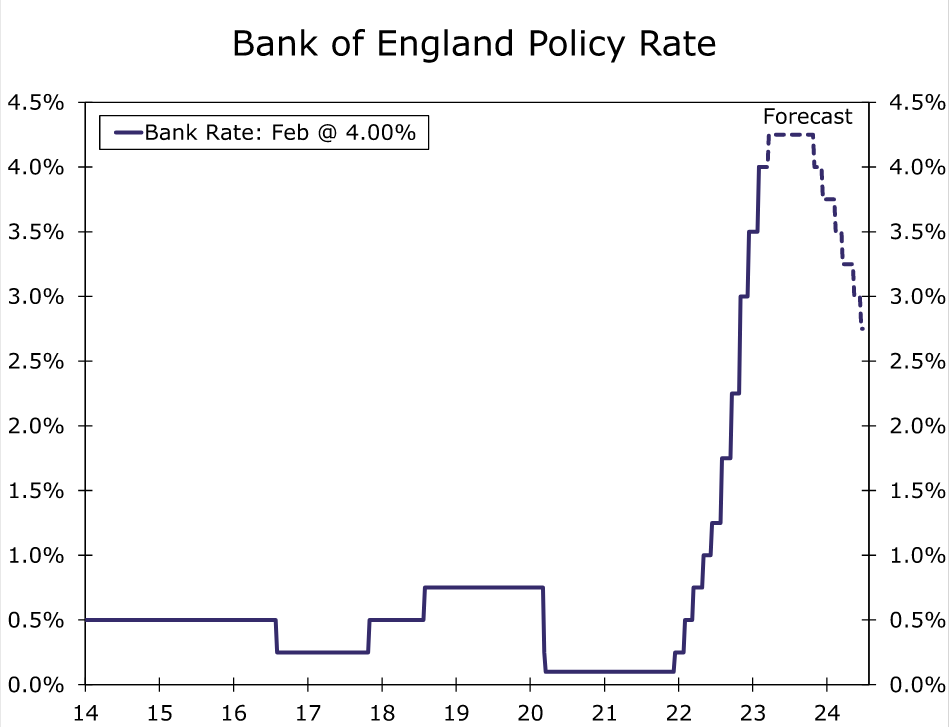

- The Bank of England (BoE) raised its policy rate 50 basis points to 4.00% at today’s announcement, while also delivering relatively balanced accompanying commentary. In fact, based on current market expectations for interest rates, the BoE expects CPI inflation to fall back below 2%. At the same time, the BoE noted considerable uncertainties around the outlook and said inflation risks were significantly to the upside.

- While the BoE could conceivably already be done, the upside inflation risks combined with a desire from BoE policymakers to ensure they “finish the job” in returning inflation sustainability back towards the 2% inflation target means we believe some modest further tightening is more likely than not. We expect a final 25 basis point rate increase at the March meeting, bringing the policy rate to a peak of 4.25%. We expect the policy rate to remain at that level through until late 2023, before the BoE embarks on rate cuts in Q4 this year.

ECB Stays the Course on Monetary Tightening

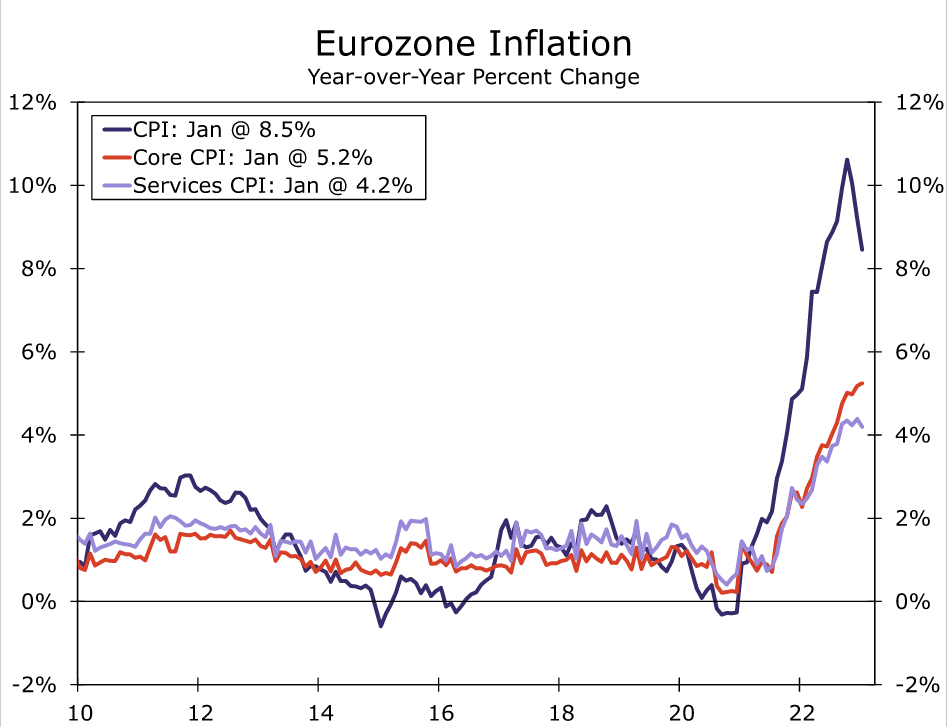

The European Central Bank (ECB) delivered a 50 basis point increase in its Deposit Rate at today’s monetary policy announcement, and offered a relatively determined message to continue along its monetary tightening path. In addition to today’s interest rate increase, the ECB said:

“In view of the underlying inflation pressures, the Governing Council intends to raise interest rates by another 50 basis points at its next monetary policy meeting in March, and it will then evaluate the subsequent path of its monetary policy. Keeping interest rates at restrictive levels will over time reduce inflation by dampening demand and will also guard against the risk of a persistent upward shift in inflation expectations. In any event, the Governing Council’s future policy rate decisions will continue to be data-dependent and follow a meeting-by-meeting approach.”

Meanwhile, with respect to its quantitative tightening plans, the ECB said it would reduce its Asset Purchase Program portfolio by €15 billion per month from March through June, with the subsequent pace of portfolio reduction to be determined over time. Partial reinvestment will be conducted in line with current practice. The quantitative tightening plans were in line with those signaled at the ECB’s December meeting.

We view the ECB’s announcement as notably, though not ultra-aggressively, hawkish. We view the pre-commitment to a 50 basis point rate hike in March as unusual and thus noteworthy. Overall, today’s announcement does not alter our outlook for the path of ECB monetary policy. We expect a further 50 basis point increase in the Deposit Rate in March and a final 25 basis point increase in May, which would see the ECB’s Deposit Rate peak at 3.25% for the current cycle.

Bank of England Gets Ready to Pivot

The Bank of England (BoE) raised its policy rate 50 basis points to 4.00% at today’s announcement, while also delivering relatively balanced accompanying commentary. The BoE noted that domestic inflation pressures have been firmer than expected and the labor market remains tight by historical standards, although there has started to be some loosening in labor market conditions. Meanwhile, the central bank also expects inflation to fall back sharply in the coming quarters, driven by softer energy prices. In fact, in its updated economic projections, which is based on a market-implied path for the policy rate that rises to around 4.5% in mid-2023 and falls back to just over 3.25% in three years time, CPI inflation declines below the 2% inflation in the medium-term. Indeed, even with a constant policy rate of 4.00%, the medium-term inflation forecast also fall belows 2%.

Taken at face value, an inflation forecast that drops below the 2% inflation target over time might signal that the BoE’s monetary tightening is done. However, BoE policymakers note:

“There are considerable uncertainties around this medium-term outlook, and the Committee continues to judge that the risks to inflation are skewed significantly to the upside.”

This is further elaborated upon in the minutes of the meeting, in which

“The Committee continued to judge that the risks to inflation were skewed significantly to the upside, primarily reflecting the possibility of greater persistence in domestic wage and price setting, and also upside risks to the wholesale energy price conditioning assumption. Qualitatively, an inflation forecast that took into account these upside risks was judged to be much closer to the 2% target at the policy horizon than the modal central projection.”

It is this medium-term outlook that likely led to some softening in the BoE policy guidance. The Bank of England said it will:

“Continue to monitor closely indications of persistent inflationary pressures, including the tightness of labor market conditions and the behavior of wage growth and services inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

The contingent nature of further rate increases, along with dropping references to the need to act forcefully, both suggest a less aggressive approach from the Bank of England moving forward. While the BoE could conceivably already be done, the upside inflation risks combined with a desire from BoE policymakers to ensure they “finish the job” in returning inflation sustainability back towards the 2% inflation target means we believe some modest further tightening is more likely than not. We expect a final 25 basis point rate increase at the March meeting, bringing the policy rate to a peak of 4.25%. We expect the policy rate to remain at that level through until late 2023, before the BoE embarks on rate cuts in Q4 of this year.

{kind=link}