U.S. Highlights

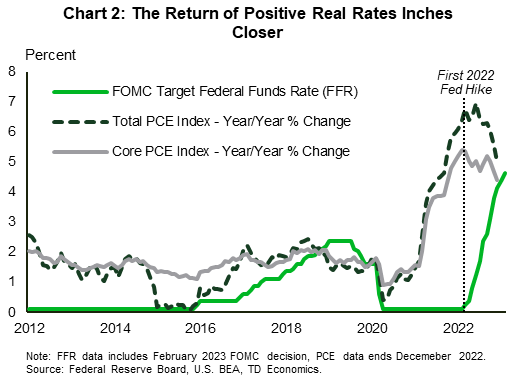

- The Federal Reserve hiked the fed funds rate 25 basis-points, a step down from six consecutive hikes of 50 or 75 bps.

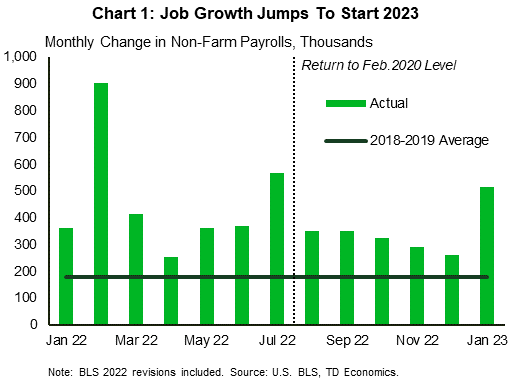

- Non-farm payrolls accelerated in January for the first time in five months, adding 517k jobs and nearly tripling market expectations.

- The ISM Manufacturing Index dropped to its lowest level since May 2020, with new orders declining at an accelerating rate, while the ISM Services Index returned to strong growth after contracting in December.

Canadian Highlights

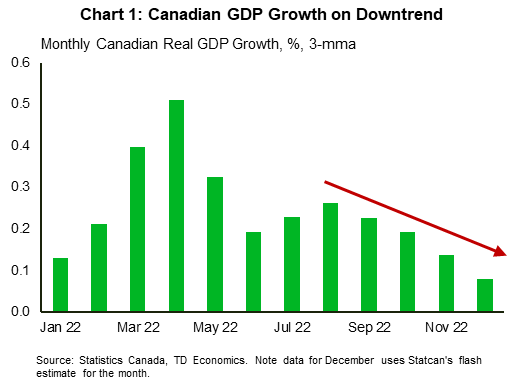

- GDP advanced at a subpar 0.1% m/m pace in November, with output gains somewhat narrowly based across industries. Even worse, Statcan’s flash estimate for December points to no growth that month.

- Growth is clearly slowing in Canada. Still, the industry-based figures are flagging a 1.6% annualized GDP gain in Q4, nearly bang on the Bank of Canada’s latest forecast.

- There is a bit more action for Canada next week, with the January Labour Force Survey and the first release of the Bank of Canada minutes from their latest policy deliberation.

U.S. – Until the Job Is Done

With the first month of 2023 in the books, the start of February was marked by the much anticipated (but widely expected) rate decision delivered by the Federal Reserve on Wednesday. Coupled with a sizeable upside surprise in the January employment data on Friday, markets certainly had a lot to think about this week. The S&P 500 rose 2.6% for the week, while the ten-year Treasury yield was little changed at 3.5% as of the time of writing.

Labor markets began 2023 with a bang, breaking a five-month deceleration trend and adding 517k jobs (Chart 1). This brought the unemployment rate down by 0.1 percentage points (ppts) to a 53-year low of 3.4%. In addition, revisions to 2022 data added 311k jobs to last year’s tally. The labor force participation rate in January ticked up by 0.1 ppts to 62.4%. Average hourly earnings rose by 0.3% month-on-month (m/m) and hours worked increased by 0.9% m/m. On aggregate, this was an exceptionally strong jobs report, which when combined with the sustained downward trend in initial jobless claims and the increase in December job openings, will give the Federal Reserve plenty to contemplate over the coming weeks.

In contrast to the strong labor market data, the ISM Manufacturing Purchasing Managers’ Index (PMI) slipped further into contractionary territory in January, dropping 1 percentage point to 47.4 – its lowest level since May 2020. Economic activity in the sector contracted for the third consecutive month, as new orders continued to decline at an accelerating rate. This contrasts with the ISM Services PMI which showed the industry return to strong growth in January after briefly contracting in December, with new orders jumping up by 15.2 percentage points. While there have been positive developments in the manufacturing sector, such as reduced delivery times and lower price pressures, the robustness of the strength in the services sector will be a concern for the Federal Reserve as it seeks to put a lid on services price growth.

February began with a partial return to conventional monetary policy in the U.S., with the Federal Reserve raising rates by a more usual 25bps for the first time since last March (Chart 2). FOMC Chair Powell noted that it was gratifying to see progress on disinflation, but that further policy tightening would be required to ensure price growth sustainably returns to the Fed’s 2% target. During the press conference, Powell also pushed back against the idea of assuming the Fed could mitigate the risk of a binding debt limit in June, stating that the only way forward was for Congress to raise the debt ceiling.

Markets expect another 25bps hike at the Fed’s next meeting in six weeks, at which time we will also receive an update on the Committee’s Summary of Economic Projections. The January employment report introduced fresh uncertainty to market expectations for the terminal rate, with May meeting expectations now evenly split between no change and a 25bps hike. Powell is in the hot seat in a Q&A next Tuesday, where he is likely to be pressed on his reading of the January jobs blowout. He is likely to confirm the hawkish bias of the press conference, and markets will be listening carefully for any hints of how high the Fed expects to raise rates now.

Canada – Growing Pains

Canadian financial markets took their cue from U.S. events this week, with both an FOMC interest rate decision and Friday’s blowout U.S. jobs report. During Chair Powell’s presser after the Fed’s interest rate decision, Canadian yields fell across the curve while equities popped higher – telltale signs of a dovish take on his comments by markets. However, yields reversed course on Friday in the wake of a super-hot January U.S. jobs report. Elsewhere, oil prices slid lower for the second straight week, greased by government data showing big inventory builds, growth concerns and, importantly, no change in production policy coming out of Wednesday’s OPEC+ meeting.

The monthly GDP report was the only main data released in Canada, which had several notable takeaways. Growth was on the softer-side last November, with the economy expanding by 0.1% month-on-month. Meanwhile, the breath of gains was not all that impressive, with output up in 11 of 20 industries and flat in three others. On a trend basis, economic growth is clearly slowing (Chart 1) and going by Statcan’s preliminary estimate for December, GDP was flat at the end of last year.

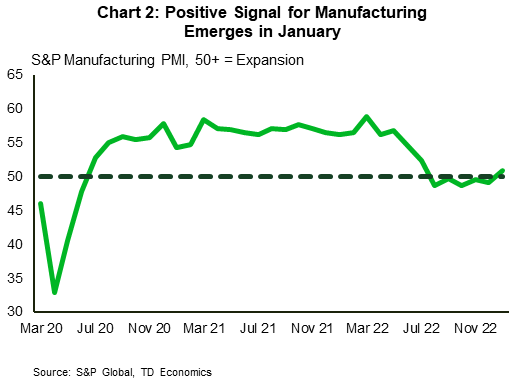

Even with December’s estimate, monthly GDP still implies 1.6% annualized economic growth in the fourth quarter. This is nearly bang-on the Bank of Canada’s latest forecast and provides precisely zero reason for second thoughts from the Bank around its recent pause. Of course, what industry-based GDP implies for a given quarter can differ from what expenditure-based GDP ultimately shows, and Chart 2 shows the Canadian manufacturing PMI from S&P Global, from March 2020 to January 2023. In January 2023, the PMI increased to 51, indicating expansion in the Canadian manufacturing sector, from 49.2 in December. Over 2022, the index averaged 53.4the latter is what the Bank of Canada uses when forecasting. However, we think the two measures lined up reasonably well in the fourth quarter. Interestingly, while U.S. economic growth may have lagged Canada’s in December, January’s sizzling jobs U.S. report suggests a stronger footing stateside last month. This, in turn, could spell positive news for Canada’s near-term growth prospects and would be consistent with the latest S&P Canadian manufacturing PMI, which moved into expansionary territory for the first time since July (Chart 2).

Next week is shaping up to be an interesting one for financial markets and the central bank. We’ll get a fresh reading on job markets with the January Labour Force Survey. Note that with the December report, Statcan published revisions showing employment levels that were higher than originially thought, even as far back as 2002. Meanwhile, hiring in 2022Q4 (while still robust) was lowered by 60k. For the January report, we’ll be looking at the full-time/part-time and public/private jobs skew as well as for indications of continued tightness. And, for the first time ever, the Bank of Canada will be releasing the minutes of their latest policy deliberation. We’ll be watching to see if the minutes provide any colour to their thinking on rates.

{kind=link}