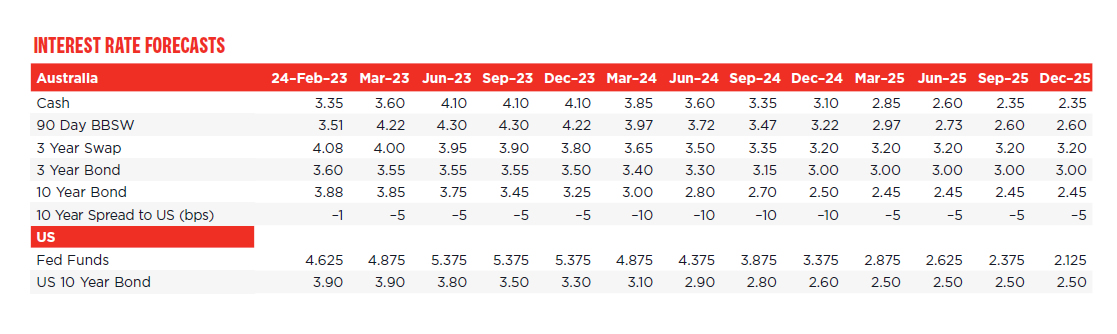

We have lifted our forecast terminal RBA cash rate from 3.85% to 4.1%.

We have also lifted our forecast for the federal funds rate with a peak in June of 5.25–5.5%, from 4.75–5% in March.

Since October we have consistently held the view that the cash rate would peak in May at 3.85%.

We still see the date of the peak as May 2023 but now see that peak as slightly higher.

The previous view envisaged a 25 basis point hike in March followed by a pause in April with the final hike of 25 basis points in May.

Over the course of the last few months of 2022 the Board consistently referred to the possibility of pausing and, as recently as December, considered a pause as one of three policy options.

However, the Board has adopted a more hawkish approach since the release of the December quarter inflation report which showed: underlying inflation at 6.9% compared to the official forecast of 6.5%; goods inflation up in the quarter; and services inflation particularly strong.

The February Minutes noted that: “members agreed that further increases in interest rates are likely to be needed over the months ahead”. This was stronger guidance than “The Board expects to increase interest rates further over the period ahead, but is not on a pre-set path”, which we saw in December. In particular, “not on a pre-set path” had allowed scope for a near term pause.

We also saw the February Board Minutes where the Board did not even consider a pause.

During the Governor’s two appearances in Canberra last week, he outlined his support for a steady approach to policy. Abruptly pausing in April, only to resume with a hike in May (as implied by our previous forecast) would not be consistent with this steady approach.

Another way to maintain the 3.85% terminal rate and eliminate the pause in April would have been to bring forward the May hike to April.

But recall that the May meeting will have the advantage of a full update of March quarter inflation including the trimmed mean underlying measure, which is not calculated in the monthly inflation indicator. We expect annual trimmed mean inflation to print 6.6% for the March quarter, down from 6.9% in December. We estimate the Reserve Bank is probably expecting around 6.7%.

This slowdown will not be sufficient for the Bank to significantly change its inflation forecasts, which are refreshed for the May meeting.

The current forecast does not envisage that inflation will be back at the 2–3% target band until June 2025.

In December, the Board Minutes noted a key reason why a pause was not appropriate: “The Bank’s most recent forecasts had indicated that, even with further increases in the cash rate as incorporated in the November forecasts, inflation was expected to take several years to return to the target range.”

With this condition unlikely to change by May it seems that a pause would again not be considered appropriate.

By the time of the June meeting, we expect that there will be credible evidence that demand is slowing; labour markets are easing; and risks of a wage/price spiral have receded.

We expect that to be confirmed by the March quarter Wage Price Index Report which is forecast to print a soft 0.8%qtr gain indicating that wage pressures are not accelerating (as we have just seen with the December Report which showed growth slowing from 1.1%qtr in September to 0.8%qtr).

At 4.1%, the cash rate will be in deeply contractionary territory and a pause will be appropriate.

The decision to pause will be with a reasonable view that the tightening cycle has peaked. Westpac concurs and expects that the next move in rates beyond mid-2023 will be the beginning of an easing cycle in the March quarter 2024.

But there are risks to this scenario and they appear to land mainly on the upside.

The downside risks – an earlier easing than March next year – seem low.

While we expect the economy to stagnate in the second half of 2023 there will not be sufficient progress in bringing inflation into line with the target before the end of 2023 to accommodate earlier rate cuts.

We expect inflation in Australia to still be around 4% by end 2023, falling to 3.0% by end 2024, allowing a policy response to a stagnating economy by the first quarter of 2024.

The outlook

The risks to our near-term rate outlook are pitched to the upside.

We have recently written about the RBA tightening cycle lagging the Federal Reserve’s.

This was because wages growth had peaked in the US and goods inflation had been slowing considerably.

In Australia we are yet to see across-the-board weakness in goods inflation while wage inflation is still lifting on an annual basis, although now appears to be slowing somewhat on a quarterly basis.

The surprise easing in the quarterly pace of wage inflation means we are now predicting a wage inflation peak of 4.0%, down from 4.5%.

The forecast extension of the US tightening cycle is in response to a further late-cycle tightening in the labour market; some evidence of resilience in demand; a slowing in the pace of overall disinflation while services inflation remains stubbornly high.

The Reserve Bank will be aware that these developments in the US may provide potential warning signals for Australia.

Our new forecasts now have Australia’s tightening cycle peaking around six weeks before the US cycle.

In Australia we also have a number of ‘COVID legacies’ that may hold up demand in the first half of 2023: the $300 billion in accumulated household excess savings; the lift in national incomes coming from the boost in the terms of trade (partly due to the reopening of China); solid household wage income growth directly stemming from tight labour markets; and the boost in demand from surging net migration (we estimate net migration reached 400,000 in 2022 and will remain strong at 350,000 in 2023).

Were these factors to offset the drags from high interest rates and collapsing real wages in the first half of 2023 the RBA might have to respond with a further move at its August meeting, since inflation is already forecast to hold up at uncomfortably high levels (the RBA expects trimmed mean inflation of 6.2% by the June quarter).

Finally, we were surprised to see the observation in the February Board Minutes that: “the cash rate was lower than in many other comparable economies”; complemented by: “there was little evidence to suggest that the overall impact of monetary policy on activity and inflation in Australia was materially different than elsewhere.” Taken on face value these comments place our two terminal rate forecasts of 4.1% and 5.25%–5.5% as quite anomalous.

Conclusion

The RBA seems locked in to further hikes in the cash rate in both March and April. The revised forecasts and March quarter inflation report are likely to require a further hike in May.

With the concerns about a wage-price spiral easing following the December quarter Wage Price Index report; demand slowing; and the cash rate deeply contractionary, at 4.1%, the case for a pause in June is credible.

Further out the next move is likely to be a rate cut beginning in the March quarter 2024.

But risks to this scenario are to the upside – COVID legacy factors that could boost demand and slow the disinflation process; the extension of the US tightening cycle; and recent recognition that Australia’s cash rate is below other countries will keep markets alert to those upside rate risks.

{kind=link}