Following the sudden collapse of the Silicon Valley Bank (SVB) in the US, investors have become increasingly concerned about the health of the banking system as borrowing costs continue to rise. While they have dramatically scaled back their bets with regards to the Fed’s future course of action, they are also doubting whether the ECB should proceed as aggressively as it signaled at its latest policy meeting. Is the telegraphed 50bps hike indeed a done deal? And if it is, will officials present a different agenda for the coming months? How will the outcome affect the euro?

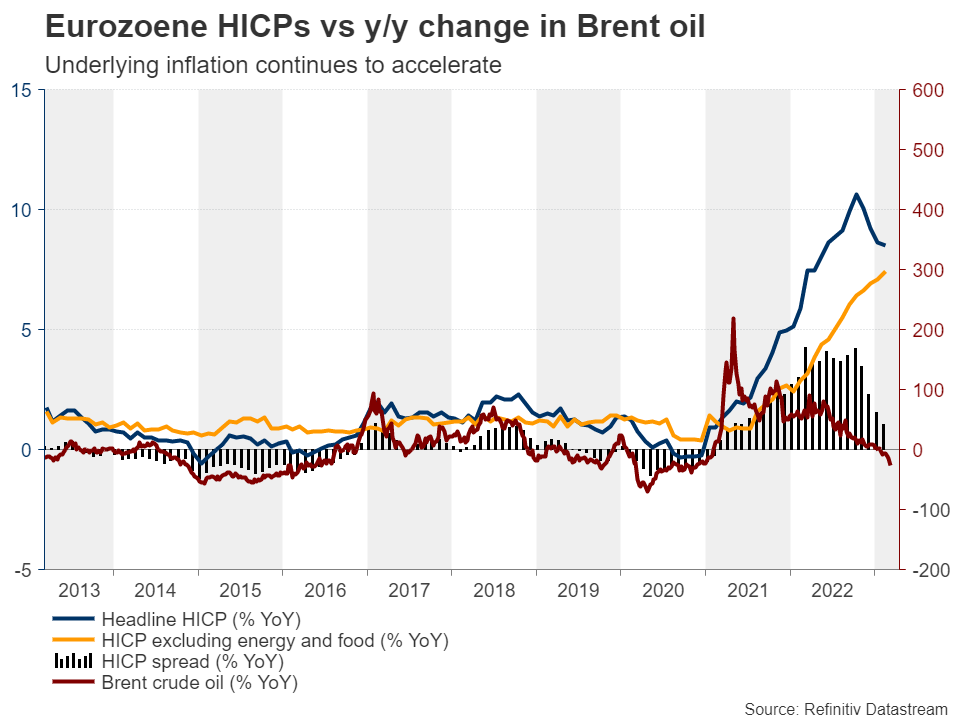

Underlying inflation remains uncomfortably high

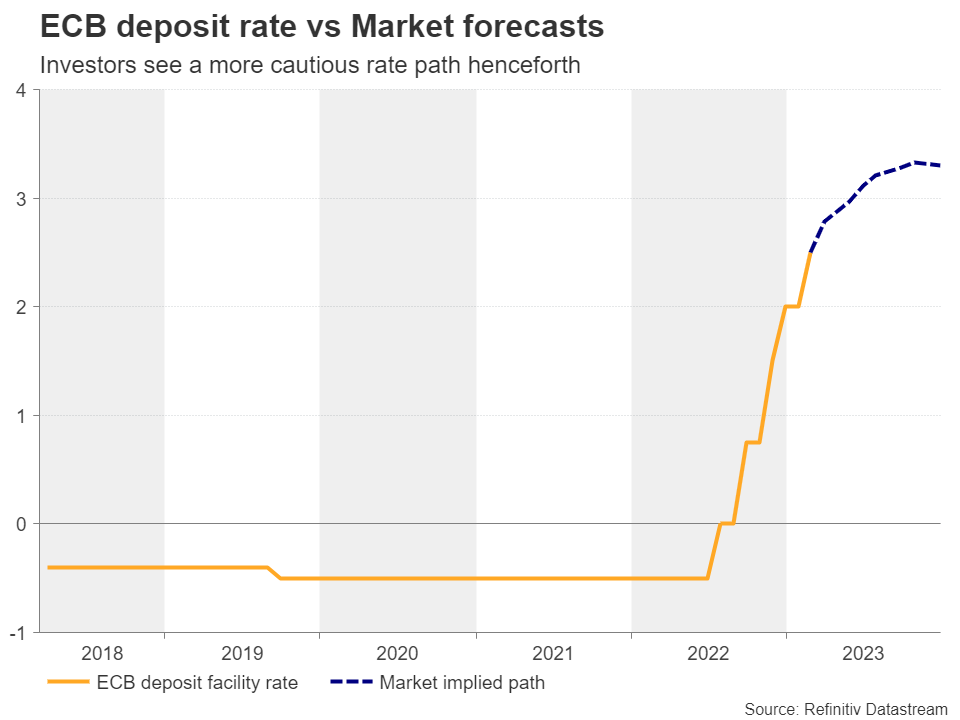

When they last met, ECB policymakers agreed to raise interest rates by 50bps as was widely anticipated, with President Lagarde explicitly saying that they intend to raise them by another 50bps at their next gathering and then evaluate the future path on a meeting-by-meeting basis. She acknowledged that supply bottlenecks are gradually easing, but she also warned that the delayed effects are still pushing up goods price inflation.

Since then, preliminary CPI data showed that headline inflation in the Euro area slowed by less than expected in February to 8.5% y/y from 8.6% and that the core rate rose to 7.4% y/y from 7.1%. Headline inflation could continue to cool down as the year-over-year change in energy prices dives deeper in the negative territory, but the spotlight seems to be on underlying metrics, which have yet to show any signs of cooling.

Indeed, just last week, President Lagarde stressed that a 50bps increase is now “very very likely”, adding that underlying inflation could stay uncomfortably high even as the overall inflation rate drops in the coming months. This likely suggested that a 50bps hike in March may not be enough to bring inflation down, and combined with optimism that a previously feared recession may be sidestepped, allowed market participants to add more basis points to their hike bets for this year. At some point last week, they were seeing an aggregate of 165 basis points worth of additional rate hikes by December.

SVB crisis sparks speculation of a smaller hike

Having said all that though, the outlook on how the ECB may proceed henceforth was dramatically altered after a US lender, the Silicon Valley Bank (SVB), collapsed and spread panic among investors. Even after the prompt response of the Fed and US Treasury to announce contingency plans, market participants remained concerned and scaled back their hike bets with regards to every major central bank. Now, the ECB is expected to raise rates by only another 85bps by the end of the year, with investors split between 25 and 50bps on the size of Thursday’s hike.

A 50bps hike could support the euro

Ergo, a potential 50bps hike is not the market’s base case scenario now and should it materialize, the euro could gain. With France’s Finance and Economy Minister and Germany’s finance watchdog saying that the event does not pose any threat to Eurozone’s financial stability, a double hike may be more likely than the market pricing currently suggests.

Nonetheless, whether the currency can hold onto any decision-related gains may depend on hints and signals about the upcoming meetings, but also on the updated economic projections. Based on the latest economic data, the new macroeconomic projections may be subject to upward revisions, which might allow ECB President Lagarde to sound hawkish at the press conference, even as several of her colleagues believe that proceeding with smaller increments is wiser.

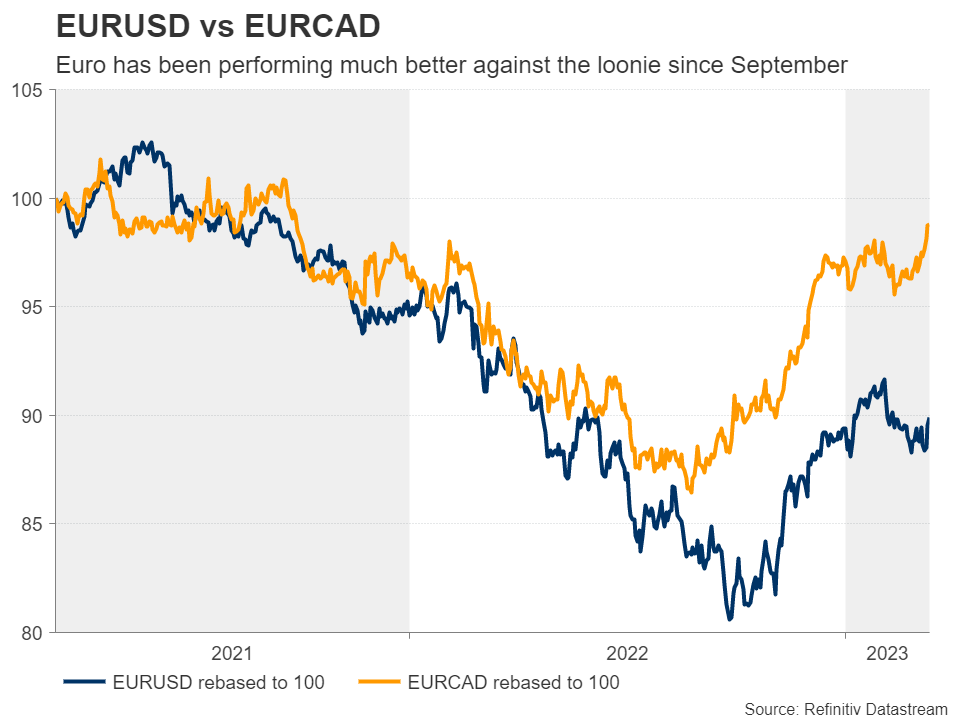

Euro/dollar may not be the best choice for exploiting any further euro gains as today’s US CPI figures could well reshape expectations about the Fed’s plans. A safer counterpart may be the Canadian dollar, whose central bank refrained from pressing the hike button at its last meeting and hinted that it could stay sidelined for the months to come.

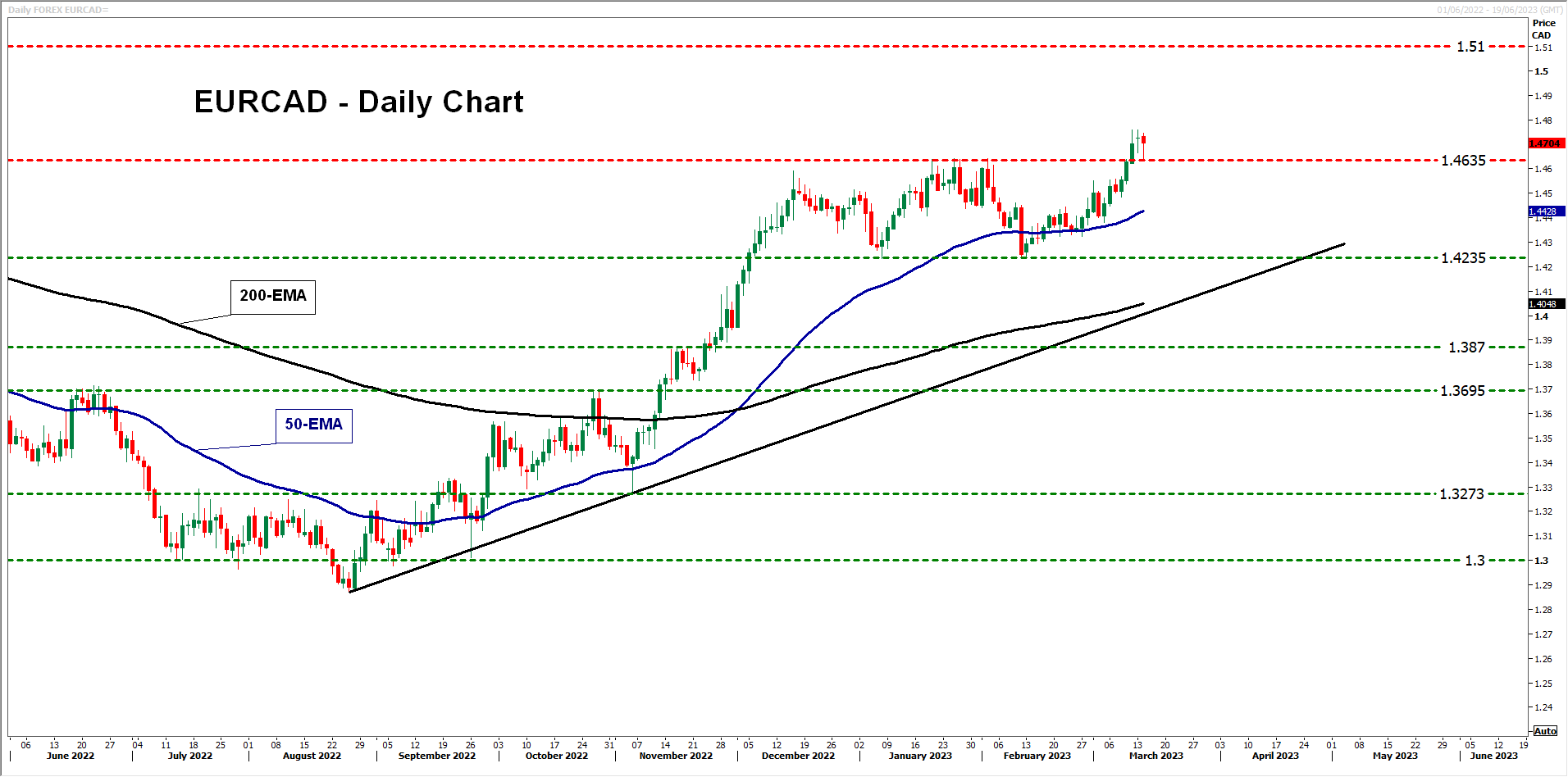

Euro/loonie tests levels last seen in 2021

Euro/loonie emerged above the key resistance zone of 1.4635 last week, testing territories last seen in September 2021. Although it is now pulling back, it remains above that key zone, and well above the uptrend line drawn from the low of August 25. This keeps the likelihood of a rebound firmly on the table and if indeed the bulls regain control, they may try to reach the 1.5100 zone, which acted as a ceiling between July 17 and September 20.

The downside risk arising from this ECB meeting is for policymakers to hint that they will opt for smaller hikes, even if they hike by 50bps now, due to financial stability concerns. Euro/loonie could dip back below the 1.4635 territory and travel all the way down to the 1.4235 barrier, which supported the pair on January 6 and February 13.

{kind=link}