With the market counting down the days to the first week of May, next week’s data releases will probably give us the strongest indication about the forthcoming ECB decision. Inflation and GDP figures set the scene for an exciting week especially as euro/dollar is trying to remain in the vicinity of 1.10.

CPI is the key for the May ECB meeting

At the March meeting the ECB announced its new data-dependent strategy. It essentially moved from the “hike-as-fast-as-possible” doctrine to a more mainstream central bank strategy. With the next meeting coming on May 4, next week’s data is extremely crucial. ECB member and Dutch central bank chief Knot was quite explicit in his comment earlier this week that April inflation will determine the size of the May hike. While Knot is a known hawk, it appears that the hawks could potentially push for a stronger rate hike than the current market-anticipated move of 25bps.

While one could justify this inherent hawkishness on the fact that the ECB has the Bundesbank mentality imprinted in its DNA, it is worth considering that the inflation situation in the nearby UK might be also affecting the ECB’s stance. The more hawkish members are determined to avoid high inflation becoming an everyday concern affecting long-term consumer perceptions.

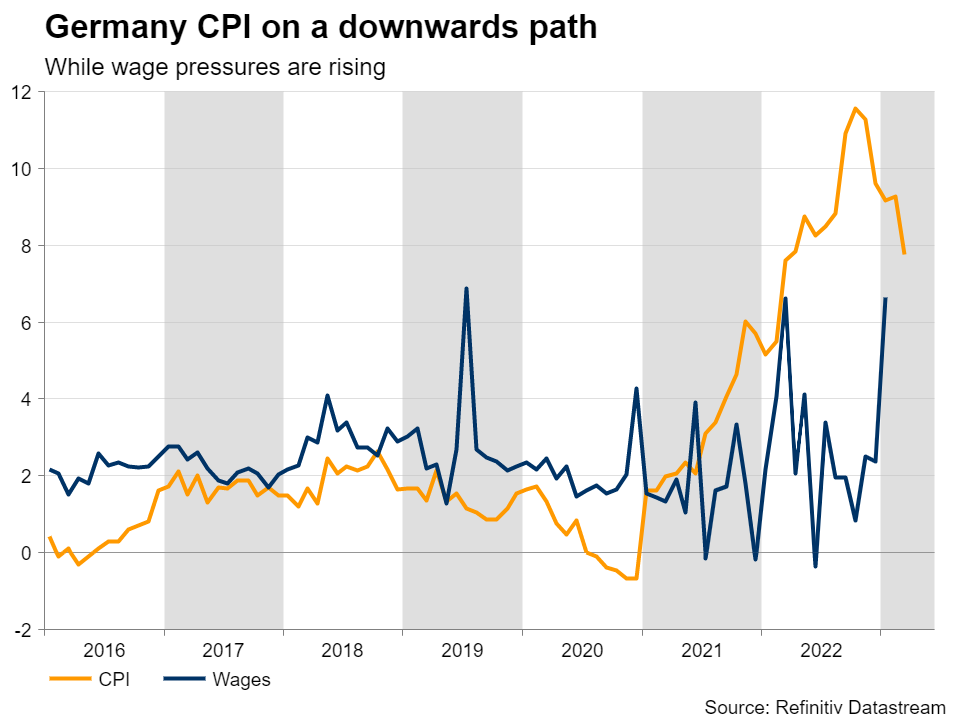

Another drop in the German CPI?

On Friday, April 28 we will get the usual release of the CPI figures for the key German states with the preliminary national print coming after midday. This is the key number by far for market sentiment. During 2022, inflation releases produced the strongest post-announcement volatility. The German CPI has been on a gentle downward trend, with the April figure expected to record another small dip to 7.2% year-on-year change. This is clearly elevated and not an easy reading for the hawks, but they can take some solace from the latest German PPI number showing a significant deceleration in the year-on-year print. On the other hand, a strong show at the German CPI would clearly open the floodgates with the immediate response being an increased possibility of a 50 bps move at the May meeting.

GDP figures might prove an unpleasant reading

Friday will commence with the preliminary GDP figures from the biggest euro area countries and the eurozone aggregate for the first quarter of 2023. Market eyes will understandably be on the German print with the consensus pointing to another negative quarter-on-quarter figure, but an improvement compared to the fourth quarter of 2022 print of -0.4% quarterly change. A second consecutive negative GDP quarter will allow for pompous headlines that Germany is officially in recession.

Semantics aside, the magnitude of the slowdown will be the key topic of discussion at the ECB halls. The IMF penciled in a -0.1% annual figure for 2023 in its April Outlook update, a view shared by the German IFO institution, and hence a weaker print at Friday’s figure will potentially open Pandora’s box with more pessimistic views spreading quickly in the newswires.

Strong start of the week with the IFO survey

The week, though, will start on an equally high note as the German IFO survey for April will be published on Monday morning. One cannot fail to notice the impressive improvement in this survey since October 2022, but it is also true that the outright level of the Expectations component remains very low compared to its long-term average. The average of the IFO survey for the first quarter of 2023 is pointing to a downside risk in the current GDP forecast.

Similarly, the market is expecting a drop in the April IFO figures, which will not be a good discussion point for ECB hawks pushing for a 50 bps rate move in two weeks, especially as Friday’s Manufacturing PMI release surprised on the downside.

Euro/pound in waiting mode

Euro/pound has been on an upward path since March 2022 lows, but it has obviously not been a one-way street. The recent range-trading activity has caused a build-up of key resistance and support points around the 0.8800 level. In addition, a right-angled triangle is trying to dictate market reaction.

With the momentum indicators confirming this delicate balance, next week’s data will most likely give the necessary push to market participants to make the first move. Euro bulls appear to have an easier path higher, at least until the 0.8902 area. On the other hand, euro bears will face considerable support at the 0.8794-0.8815 area defined by multiple SMAs and historical peaks.

{kind=link}