U.S. Highlights

- U.S. real GDP growth slowed to 1.1% quarter-over-quarter (q/q) annualized in 2023 Q1, from 2.6% q/q in the previous quarter. A measure of underlying domestic demand accelerated to 2.9% q/q, supported by a strong gain in consumer spending, although the monthly pattern revealed that the spending gain was entirely concentrated in January.

- New home sales grew by 9.6% month-on-month in March. While this series is volatile, it has been trending up since the end of last year.

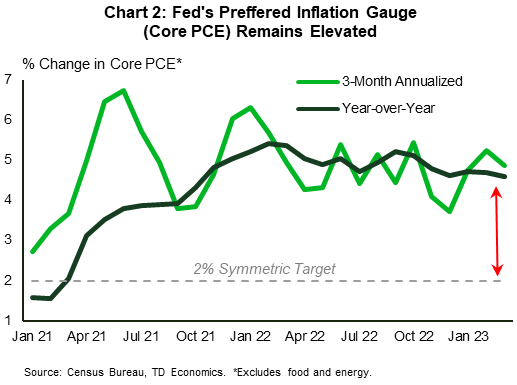

- Core PCE inflation remained elevated in March, easing modestly to 4.6% year-on-year from 4.7% in February.

Canadian Highlights

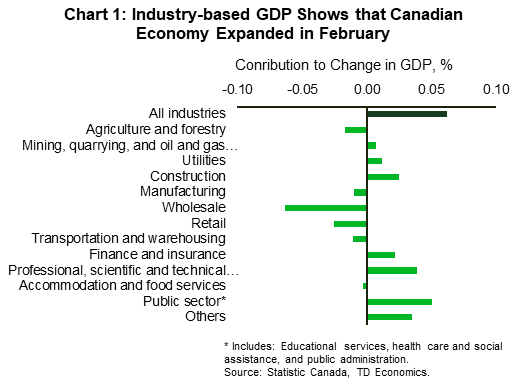

- February’s GDP print came in weaker than Statistics Canada’s estimate. Accounting for a decline in the flash estimate for March, first quarter GDP growth is tracking at an annualized rate of 2.5%.

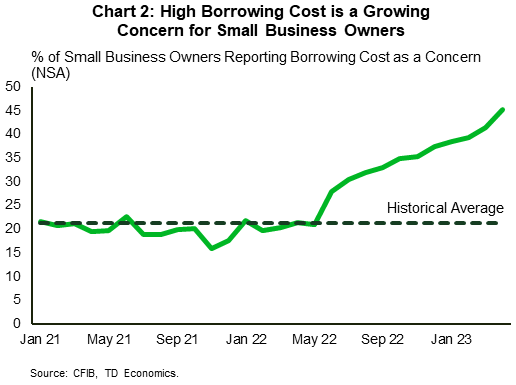

- Looking ahead, growth is expected to slow as higher rates continue to work their way through the economy. April’s release of the CFIB small business barometer showed that rising costs of borrowing are a growing concern for entrepreneurs.

- This week was also marked by a continuation of the federal public workers strike. We expect the strike to weigh on GDP growth in the near term, with offsetting growth in subsequent periods, resulting in an overall neutral impact.

U.S. – Core Inflation Remains Elevated, Fed to Hike Next Week

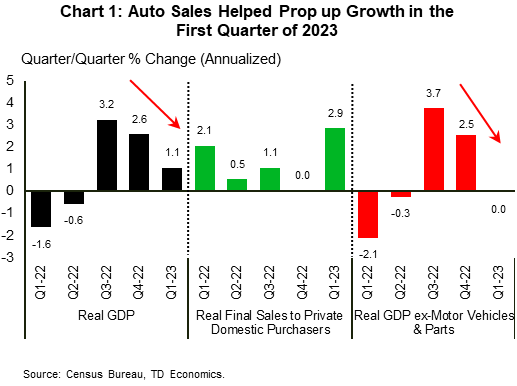

U.S. real GDP growth slowed to a 1.1% quarter-over-quarter (q/q) annualized pace in the first quarter of 2023, from 2.6% q/q at the end of 2022. While consensus expectations were looking for a better print, a slowdown in growth was always in the cards as a reversal of the prior quarter’s inventory built-up was expected. That reversal materialized. Government spending, meanwhile, provided an offset, delivering a 0.8 percentage point (pp) contribution to growth. With the combined impact of inventories and government spending adding volatility to the data, we typically look past these items and focus on ‘final sales to private domestic purchasers’ to get a clearer reading of underlying domestic demand. After several quarters of slow growth, this measure accelerated to 2.9% q/q, supported by a strong gain in consumer spending (+3.7%).

At face value, the acceleration in underlying domestic demand is good news. However, monthly spending data shows that the strength was concentrated in January, with growth flatlining over the next two months. Much of the quarter’s strength came from auto sales. Unit auto sales grew from 14.3 million (annualized) at the end of 2022, to 15.3 million in 2023 Q1, resulting in a 1.1 (pp) contribution to GDP. If we remove that impact, the rest of the economy recorded zero growth (Chart 1). While our forecast calls for motor vehicles sales to remain at a high level over the near-term, as pent-up demand is satiated by improved production (see here), this channel is unlikely to offer the same level of support in 2023 Q2.

Residential investment remained a growth detractor for the eight consecutive quarter, but its negative impact moderated noticeably as average declines of 26% q/q in the second half of 2022 eased to 4.2% q/q in 2023 Q1. We expect residential investment to be less of a drag this year, a message echoed by some moderate positive signals out of the housing market. New home sales, a volatile series, continue to trend up since the end of last year, rising 9.6% month-on-month in March. This is happening as tight supply conditions on the existing home market look to be driving some more action towards the new home market. That said, with housing affordability still exceptionally low, buyers are showing increased sensitivity to mortgage rates (though with the typical lag). An index tracking the number of contracts signed to purchase existing homes, a reliable indicator of closed sales, fell 5.2% in March amidst an uptrend in mortgage rates earlier in the month. The stress in regional banking is also likely to have contributed to the hesitation among buyers to sign housing contracts.

In weighing the Fed’s next interest rate decision, the latest PCE report showed that the Fed’s preferred inflation gauge remained elevated in March. While overall PCE slowed noticeably to 4.2% year-on-year (y/y), from 5.1% in the month prior, core PCE eased only modestly to 4.6% y/y (Chart 2). In our view, core PCE inflation has a long way to return to target (see here). As such, we expect the Fed to hike by 25 basis points next week and keep the policy rate at that high level through the end of the year.

Canada – Prepare for Landing

In anticipation of this week’s marquee release of industry-based GDP, Canadian financial markets were largely occupied with first quarter corporate earnings reports. The S&P/TSX Composite remained 0.6% weaker on the week at the time of writing, despite a sizeable end of week rebound.

Meanwhile, February’s GDP print came in at 0.1% month-on-month (m/m) – weaker than 0.2% m/m expected by the consensus and Statistics Canada’s own flash estimate of 0.3% m/m. With today’s reading and the flash estimate of -0.1% m/m for March, first quarter GDP is tracking at a rate of 2.5% quarter-on-quarter (q/q) annualized. This is a touch stronger than 2.3% q/q pace the BoC was expecting in its April Monetary Policy Report. Underneath the surface, the major contributor to growth came from residential building construction, which expanded by 0.3% on the month (Chart 1). The public sector, which includes health care and social assistance, public administration, and educational services, was 0.2% higher on the month, clocking in its impressive thirteenth consecutive month of growth.

Offsetting these gains was a decline in manufacturing, transportation & warehousing, as well as retail and wholesale trade. The contraction in trade alone shaved one tens of a percentage points off the headline number, which reiterates our expectation of slowing in household consumption expenditure. According to our internal spend data, services spending growth already shows early signs of moderation, which should help bring down consumption growth to around 1% in 2023 Q2, as higher financing costs continue to work their way through the economy.

That said, continued fiscal support and robust population growth could buttress demand beyond our current expectations. We estimate that combined new federal and provincial fiscal measures amount to 0.9% of Canadian GDP this year. Notably, government capital spending could boost business investment as private enterprises pull back on investment intentions due to rising costs of borrowing and tighter credit standards. According to April’s CFIB small business barometer, 44% of business owners report this as a concern – more than twice the historical average (Chart 2). Another area of concern is rising wage costs, with 68% of business owners identifying it as an impediment to their business and 44% expecting average wage growth to be higher than 3%.

Private enterprises are not the only ones facing wage pressures. This week was marked by a continuation of one of the largest job actions in Canadian history, with more than 100k federal employees on strike. Depending on its duration, we expect it to shave between 0.2 and 0.9 percentage points off monthly GDP growth. But this decline will be reversed in the subsequent periods, with the overall impact being neutral. All in all, “slow but positive growth” remains the most likely scenario for the Canadian economy. Still, we recommend remaining seated with your seat belt fastened as the economy prepares for a soft landing.

annualized pace in the first quarter of 2023, from 2.6% q/q at the end of 2022. While consensus expectations were looking for a better print, a slowdown in growth was always in the cards as a reversal of the prior quarter’s inventory built-up was expected. That reversal materialized. Government spending, meanwhile, provided an offset, delivering a 0.8 percentage point (pp) contribution to growth. With the combined impact of inventories and government spending adding volatility to the data, we typically look past these items and focus on ‘final sales to private domestic purchasers’ to get a clearer reading of underlying domestic demand. After several quarters of slow growth, this measure accelerated to 2.9% q/q, supported by a strong gain in consumer spending (+3.7%).){kind=link}