After almost touching a record high last month, gold prices have corrected lower, trampled under the weight of rising yields and a resurgent US dollar as markets priced in a higher-for-longer scenario for Fed rates. These forces could keep bullion under pressure for now, although in the bigger picture, the trend of sovereign buying by central banks and nerves around a recession might be enough to propel gold to new heights.

Behind the rally

Gold prices have staged a stunning recovery after bottoming out last year, rising more than 21% since November. Several elements fueled this powerful rally, including safe-haven demand after the collapse of several US regional banks, direct gold purchases by central banks, and hopes that the Fed’s tightening cycle is approaching its conclusion.

But the rally lost some steam lately. After getting rejected for a third time from the record high of $2,072, gold prices have declined by around 6% to settle in a narrow sideways range. The market has been trapped between $1,935 and $1,975 over the last month, waiting for a catalyst to break out.

This retreat and the ensuing consolidation phase reflect the latest developments in global markets. With fears about an imminent recession fading away, investors have recalibrated the Fed’s interest rate trajectory, pricing in higher rates for a longer period of time. This reassessment also helped to breathe some life back into the US dollar.

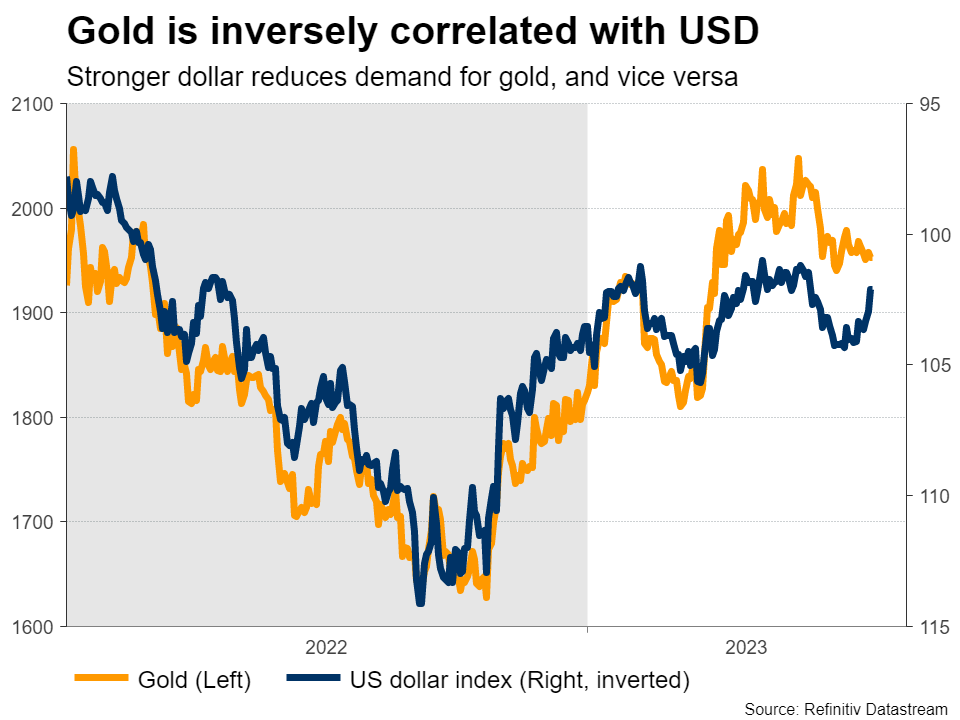

Interest rate expectations and movements in the dollar are critical for gold. The precious metal does not pay any interest to hold, so it becomes less attractive as yields rise and investors can earn higher returns in bonds.

Similarly, since gold is generally priced in US dollars, a stronger greenback makes it more expensive for foreign investors to buy the metal. The opposite effects are also true – gold becomes more attractive as yields fall and the dollar depreciates.

Geopolitics and central banks

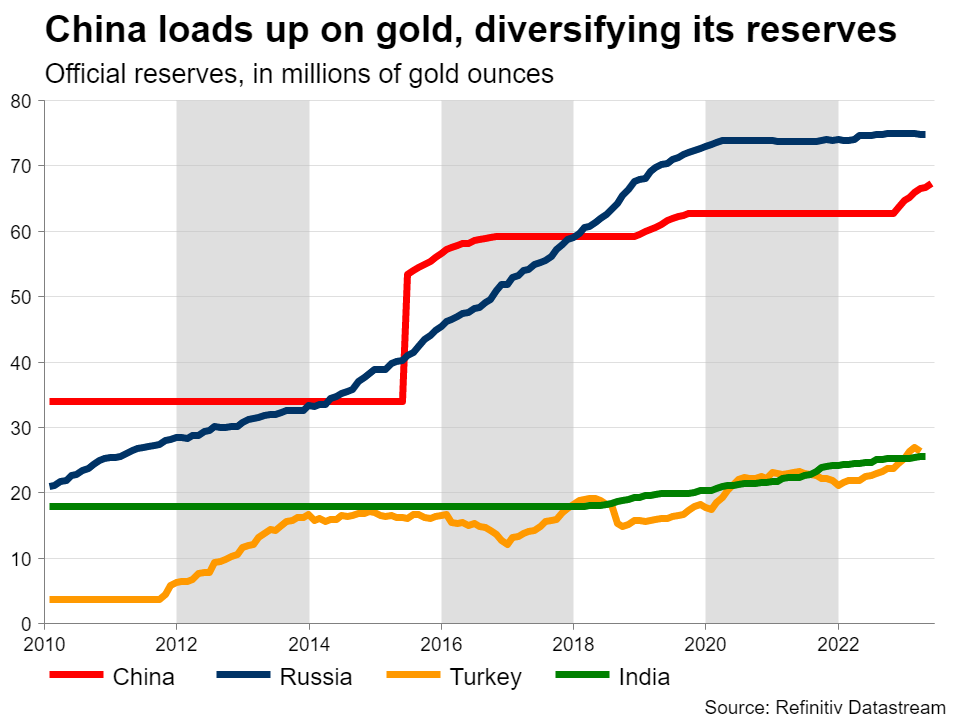

Beyond interest rates, the dollar, and safe-haven demand, the fourth variable that has emerged as a major driver of gold lately is the purchase of bullion by central banks to raise their reserves.

Geopolitics are behind this phenomenon. In the aftermath of the Ukraine invasion, the United States and Europe deployed crippling sanctions against Russia, which included the freezing of the FX reserves it held in dollars and euros. But its gold reserves that were held in Russia could not be frozen.

This helps to explain why China has been buying gold relentlessly over the past year. Beijing is trying to diversify its reserves, so it has been loading up on gold, which cannot be frozen if the geopolitical atmosphere turns colder. Other major sovereign buyers over the past year include Turkey and India.

Sovereign purchases are likely a game-changer for trading dynamics in gold. When there are such massive buyer whales lurking in the market, which are less sensitive to prices than other players because they also have political motives in mind, it almost establishes a soft floor under gold prices, preventing any massive selloffs.

New record highs? Maybe later on

Looking ahead, the central question for gold prices is whether a recession has been averted, or simply delayed. For now, the US economy remains fairly resilient. Economic growth is still solid and the labor market is in good shape, which suggests interest rates are likely to remain elevated for a longer period of time.

That’s a difficult environment for bullion, as it implies higher bond yields and a relatively strong US dollar. Hence, there is a clear risk that the recent consolidation phase in gold concludes with a break lower, in which case the focus would turn towards the $1,855 region that also encompasses the 200-day moving average.

For gold to resume its journey towards new record highs, it would likely require recession concerns to resurface. A weaker economic data pulse could see investors flirting with the idea of Fed rate cuts, pushing yields and the dollar lower.

With defensive demand also on the rise, such a scenario has the capacity to propel gold back towards the record high of $2,072 for a fourth time. That said, this is probably a longer-term story, perhaps around the end of this year or even beyond.

In other words, there isn’t much on the immediate horizon that can fuel upside in gold, as long as the Fed is keeping rates high and the economy is holding strong. This points to a sideways market over the next few months, with risks tilted to the downside.

Ultimately though, it is almost inevitable the economy will feel the burn of all the rapid-fire rate increases that have been rolled out over the past year. At that point, gold will most likely begin to shine once again.

{kind=link}