EUR/USD: When Will the Pair Return to 1.1000?

Summarizing the second half of June, the result in the EUR and USD confrontation can be said to be neutral. On Friday, June 30, EUR/USD ended up where it traded on both the 15th and 23rd of June.

On Thursday, June 29, some quite strong macroeconomic data came out of the US. The Bureau of Economic Analysis revised its GDP figures for the first quarter upwards to 2.0% year on year (YoY) (forecast was 1.3%). As for the labour market, the number of initial jobless claims for the week dropped by almost 30K, reaching the lowest level since the end of May – 239K.

Recall that the Federal Open Market Committee (FOMC) of the US Federal Reserve decided at its June 14 meeting to take a pause in the process of monetary tightening and left the interest rate unchanged at 5.25%. After this, market participants were left to speculate on the regulator’s next moves. The released data reinforced confidence in the stability of the country’s economy and raised expectations for further dollar interest rate hikes. According to the CME FedWatch Tool, the probability of a rate hike of 25 basis points (bps) at the Fed’s July meeting rose to 87%, and the probability that the total rate hike by the end of 2023 will be 50 bps is nearing 40%. As a result, in the middle of Friday, June 30, EUR/USD recorded a local low at 1.0835.

Speaking at an economic forum in Sintra (Portugal) on Wednesday, June 28, Federal Reserve Chairman Jerome Powell stated that further interest rate increases would be driven by a strong labour market and persistently high inflation. However, the core personal consumption expenditures (PCE) data published on June 30 indicated that inflation, although slowly, is declining. Forecasts suggested that the PCE index for June would remain at the previous level of 4.7%, but in reality, it fell to 4.6%. This somewhat dampened the bullish sentiment on the dollar, with the DXY index heading lower and EUR/USD returning to the central zone of the two-week sideways corridor, ending the five-day period at 1.0910.

As for the state of the economy on the other side of the Atlantic, following high preliminary inflation data from Spain and Germany, markets expected the Harmonised Index of Consumer Prices (HICP) in the Eurozone to rise by 0.7% in June, significantly exceeding the 0.2% a month earlier. However, the actual value, although higher than in May, was only slightly so, at 0.3%. Moreover, the preliminary Consumer Price Index (CPI) published on Friday, June 30th, showed a decrease in Eurozone inflation from 6.1% to 5.5% YoY (forecast was 5.6%).

Recall that after hawkish statements from ECB leaders made in mid-June, the markets had already priced in two euro rate hikes, in July and September, each by 25 basis points. Therefore, the fresh European inflation data had little effect on investor sentiment.

Friday, June 30, marked not only the end of the quarter but also the first half of the year. In this regard, representatives from several banks decided to make predictions for the second half of 2023 and the start of 2024. Economists at Credit Agricole see risks of a decrease in EUR/USD from current levels in the near term and predict its gradual recovery starting from Q4 2023. In their opinion, over the next 6-12 months, the pair could rise to 1.1100.

Strategists at Wells Fargo expect the dollar to be fairly stable or even slightly stronger for the rest of 2023. However, they predict a noticeable weakening over the course of the following year. “Given our expectations for a later and shallow recession in the U.S. and a later easing of Fed policy,” Wells Fargo analysts write, “we anticipate a later and more gradual depreciation of the U.S. dollar. […] We predict that by the end of 2023, the trade-weighted U.S. dollar rate will change little compared to the current level, and by 2024 it will have declined by 4.5%.”

Economists at Goldman Sachs also updated their EUR/USD forecasts. They too now indicate a smaller drop in the coming months and a more prolonged recovery of the euro by the end of 2023 and the first half of 2024. They predict the pair rate to be at 1.0700 in three months, 1.1000 in six months, and 1.1200 in twelve months.

As for the near-term prospects, at the time of writing this review on the evening of June 30, 50% of analysts voted for the pair’s decline, 25% for its rise, and the remaining 25% took a neutral position. Among oscillators on D1, 35% are on the side of the bulls (green), 25% are on the side of the bears (red), and 40% are painted in neutral grey. Among the trend indicators, 90% are coloured green, and only 10% are red. The nearest support for the pair is located around 1.0895-1.0900, followed by 1.0865, 1.0790-1.0815, 1.0745, 1.0670 and, finally, the May 31 low of 1.0635. The bulls will encounter resistance in the area of 1.0925-1.0940, followed by 1.0985, 1.1010, 1.1045, 1.1090-1.1110.

Upcoming events to note include the release of the Manufacturing Purchasing Managers’ Index (PMI) for Germany and the US on Monday, July 3. The minutes from the latest FOMC meeting will be published on Wednesday, July 5. The following day, on Thursday, July 6, data on retail sales volumes in the Eurozone will be available. On the same day, the ADP employment report and the PMI for the US service sector will also be published.

Closing out the work week, another batch of data from the US labour market will be released on Friday, July 7, including the unemployment rate and the important nonfarm payroll (NFP) figure. ECB President Christine Lagarde will also deliver a speech on the same day.

Furthermore, traders should be aware that Tuesday, July 4 is a public holiday in the US, as the country observes Independence Day. As a result, the markets will close earlier the day before due to the holiday.

GBP/USD: How Mr. Powell “Defeated” Mr. Bailey

In the previous review, we noted how strongly the words of officials affect quotes. This week was another confirmation of this. On Wednesday, June 28, GBP/USD showed an impressive drop. The cause were the speeches of the Federal Reserve Chair Jerome Powell and Bank of England’s Governor Andrew Bailey in Sintra. Mr. Bailey promised that his Central Bank would “do whatever it takes to get inflation to target level”. This implies at least two more rate hikes. However, Mr. Powell did not rule out further tightening of the Fed’s monetary policy, even though inflation in the US is much lower than in the United Kingdom. As a result of these two speeches, Jerome Powell and the US currency won, and GBP/USD dropped sharply.

The next day, strong US macro statistics added strength to the dollar. If it were not for the data on the Personal Consumption Expenditures (PCE) in the US published at the end of the week, the pound would have suffered quite a bit. But thanks to the PCE, in just a few hours it managed to recover almost all the losses and put the final chord at the mark of 1.2696.

In the mentioned speech in Sintra, Andrew Bailey also stated that “the UK economy has proven much more resilient” than the Central Bank expected. We would like to believe the head of the BoE. However, the data published by the Office for National Statistics (ONS) on June 30 raise certain concerns. Thus, the country’s GDP grew in Q1 2023 by 0.1% in quarterly terms and 0.2% in annual terms. And if the first indicator remained at the previous level, then the second showed a significant decline: it turned out to be 0.5% lower than the data for Q4 2022.

According to Credit Suisse economists, the situation facing the Bank of England should be defined as genuinely exceptional. But the slowdown in British GDP does not seem to worry the BoE leadership too much, which is focused on combating high inflation.

Following the May and June meetings, the BoE raised the interest rate by 25 basis points and 50 basis points to 5.00%. Many analysts believe that the regulator may bring it up to 5.50% already at the two upcoming meetings, and then to 6.25%, despite the threat of economic recession. Such steps in the foreseeable future will support the pound. At Credit Suisse, for example, they believe that even though the pound has significantly strengthened since September 2022, GBP/USD still has the potential to grow to 1.3000.

From a technical analysis perspective, the indications of oscillators on D1 appear quite uncertain – a third point to the north, a third to the south, and a third to the east. The picture is clearer for trend indicators – 90% recommend buying, 10% selling. If the pair moves south, it will encounter support levels and zones at 1.2625, 1.2570, 1.2480-1.2510, 1.2330-1.2350, 1.2275, 1.2200-1.2210. In case of the pair’s rise, it will meet resistance at levels of 1.2755, 1.2800-1.2815, 1.2850, 1.2940, 1.3000, 1.3050, and 1.3185-1.3210.

As for the events of the coming week, the focus will be on the publication of the PMI in the UK manufacturing sector on Monday, July 3. On Tuesday, July 4, the Bank of England’s report will be published, which may shed light on the future course of monetary policy. And at the end of the week, on Friday, July 7, the data on the US labour market, including the level of unemployment and such an important indicator as the number of new jobs outside the agricultural sector (NFP), will be released.

In the events for the upcoming week, one can note Monday, July 3, when the Manufacturing Purchasing Managers’ Index (PMI) for the United Kingdom will be published.

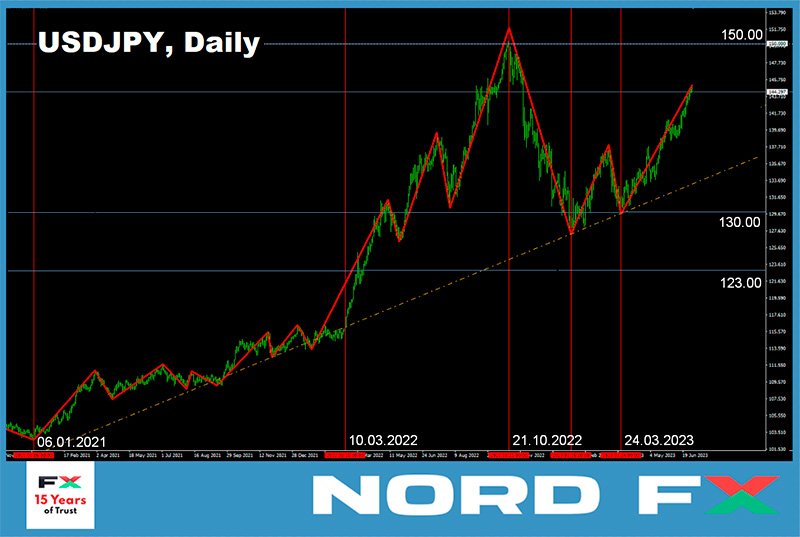

USD/JPY: The “Ticket to the Moon” Turned Out to be Multi-Use

As soon as we mentioned the potential interventions to support the yen in our last review, almost everyone started discussing this topic, including analysts and even officials from the Japanese Government. Of course, our speculations were not the trigger; it was the exchange rate of the Japanese currency. Last week, USD/JPY continued its “flight to the moon,” setting another record at the height of 145.06. Interestingly, it was at the 145.00 mark that the Bank of Japan (BoJ) conducted its first intervention in many years.

It has been said a thousand times that increasing divergence in monetary policy between the Bank of Japan and other major central banks is a recipe for further yen weakening. Thus, last week, following the release of US GDP and unemployment claims data, the yield on 10-year US treasury bonds jumped to 3.84%, and two-year bonds to 4.88%, the highest level since March. Therefore, the spread between US and Japanese bonds continues to widen, reflecting the growing divergence in the monetary policy of the Fed and the BoJ and pushing USD/JPY to astronomical heights. Understandably, in such a situation, the question arose about the ability of the Japanese regulator to artificially support its national currency.

Hirokazu Matsuno, the Chief Cabinet Secretary of Japan, stated on Friday, June 30 that the authorities are “closely monitoring currency movements with a high sense of urgency and immediacy.” “It’s important that the exchange rate moves steadily, reflecting fundamental economic indicators. Recently, sharp unilateral movements have been observed. [We] will take appropriate measures in response to excessive currency movements,” promised the high-ranking official.

However, several experts doubt that the Japanese Government and Central Bank have the strength and capability not just to strengthen the yen once, but to maintain it in such a state over an extended period of time. It’s enough to recall that less than eight months have passed since the last intervention in November 2023, and here again, USD/JPY is storming the height of 145.00. Since all currency reserves are finite, say Commerzbank specialists, solving this problem will be infinitely difficult, and “all that remains is to hope that officials from the [finance] ministry realize this and do not overestimate their capabilities.”.

The monetary policy pursued by the Japanese Government and Central Bank in recent years clearly indicates that their focus is not solely on the yen exchange rate, but on economic indicators. However, it is important to note that one of these indicators is inflation. In this regard, we have seen an acceleration in the Consumer Price Index (CPI) to 3.1% YoY, compared to 3.0% the previous month and 2.7% in February. While these values are significantly lower than those observed in the US, Eurozone, or the UK, no one can guarantee that inflation will not continue to rise further. If the BoJ does not intend to tighten its ultra-easy policy and raise interest rates, the only tool left to maintain the exchange rate is currency interventions. The only remaining question is when they will begin – now or when the rate reaches 150.00, as it did in the autumn of 2022.

Many experts still hold hope that the Bank of Japan will eventually decide to tighten its policy. These hopes allow economists at Danske Bank to forecast a USD/JPY rate below 130.00 within a 6–12-month horizon. Similar predictions are made by strategists at BNP Paribas, who target 130.00 by the end of this year and 123.00 by the end of 2024. However, Wells Fargo’s forecast appears more modest, with their specialists expecting the pair to only decrease to 133.00 by the end of 2024. Nonetheless, reaching that level would still be considered a significant achievement for the Japanese currency, as it concluded the past week at 144.29 after the publication of US PCE data.

At the time of writing the review, 60% of analysts, like a week ago, anticipate that the yen will recoup at least some of its losses and push the pair to the south, while the remaining 40% of experts point to the east. However, there are no supporters of the pair’s growth this time. It is worth noting that there were only a minimal number of supporters the previous week, with only 10%. Nevertheless, USD/JPY continues its journey to the stars. Ultimately, while experts ponder, the market decides. Regarding this matter, there are no doubts from either trend indicators or oscillators: all 100% on D1 point upwards. However, a quarter of the oscillators actively signal overbought conditions for the pair.

The nearest support level is located in the 143.74 zone, followed by 142.95-143.20, 142.20, 141.40, then 140.90-141.00, 140.60, 138.75-139.05, 138.30, and 137.50. The closest resistance is at 144.55, and then bulls will need to overcome barriers at 145.00-145.30, 146.85-147.15, and 148.85, before reaching the October 2022 high of 151.95.

No significant economic information related to the Japanese economy is expected to be released in the upcoming week. However, unless the Bank of Japan announces currency interventions, which they do not typically preannounce.

CRYPTOCURRENCIES: Institutional Bitcoin Frenzy Gains Momentum

What has been talked about and dreamed of for so long seems to be happening: global financial giants are finally believing in the bright future of Bitcoin. Back in 2021, Matt Hougan, Chief Investment Officer at Bitwise, mentioned that futures-based cryptocurrency ETFs were not suitable for long-term investors due to high associated costs. He stated that once spot-based bitcoin exchange-traded funds (ETFs) emerged, institutional investors would start pouring significant investments. Recently, in an interview with Bloomberg, Hougan announced the dawn of a new era, saying, “Now we have BlackRock raising the flag and stating that BTC has value, that it’s an asset in which institutional investors want to invest. I believe we are entering a new era of cryptocurrencies, which I call the ‘mainstream era,’ and I expect a multi-year bull trend that is just beginning.”.

A spot BTC ETF is a fund whose shares are traded on an exchange and track the market or spot price of BTC. The main idea behind such ETFs is to provide institutional investors with access to bitcoin trading without physically owning it, through a regulated and financially familiar product.

Currently, eight major financial institutions have submitted applications to the U.S. Securities and Exchange Commission (SEC) to enter the cryptocurrency market through spot-based ETFs. Alongside investment giant BlackRock, these include global asset managers such as Invesco and Fidelity. Global banks such as JPMorgan, Morgan Stanley, Goldman Sachs, Bank of New York Mellon, Bank of America, Deutsche Bank, HSBC, and Credit Agricole have also joined the bitcoin fever.

It is worth noting that the SEC has previously rejected all similar applications. However, the current situation may be different. SEC Chairman Gary Gensler has confirmed that the SEC considers bitcoin a commodity, opening up broad prospects for the leading cryptocurrency. Cameron Winklevoss, one of the founders of the cryptocurrency exchange Gemini, has confirmed that institutional investors are ready to start buying BTC, expecting the approval of spot-based BTC funds. “Bitcoin was the obvious and most profitable investment of the past decade. But it will remain the same in this decade,” said Winklevoss. This sentiment is shared by Hugh Hendry, the manager of Eclectica Asset Management hedge fund, who believes that BTC could triple its market capitalization in the medium term.

When it comes to altcoins, the situation is somewhat more challenging. Max Keiser, a popular bitcoin maximalist and now an advisor to the President of El Salvador, believes that Gary Gensler has enough technical and political tools at his disposal to classify XRP and ETH as securities, which would ultimately kill these altcoins. “The Securities and Exchange Commission is working for the banking cartel, engaging in racketeering in the interest of financial structures,” Keiser wrote in his blog.

It is worth noting that the SEC has filed lawsuits against Binance and Coinbase, accusing the platforms of selling unregistered securities. In the court documents, the Commission identified Solana (SOL), Cardano (ADA), Polygon (MATIC), Coti (COTI), Algorand (ALGO), Filecoin (FIL), Cosmos (ATOM), Sandbox (SAND), Axie Infinity (AXS), and Decentraland (MANA) as securities. Several cryptocurrency platforms have already taken this SEC statement as guidance and, to avoid potential claims, have delisted these altcoins.

The statements above indicate that bitcoin is likely to maintain its market leadership in the foreseeable future. Mark Yusko, the founder and CEO of Morgan Creek Capital, believes that the bullish trend of BTC could continue until the next halving, which is expected to occur in April 2024. “I think the rally is just beginning. We have just entered what is known as the crypto summer season,” wrote the expert. However, he cautioned that after the speculative surge caused by the halving, there is typically an excessive reaction in the opposite direction, known as crypto winter.

According to an analyst known as InvestAnswers, in addition to the upcoming halving, the institutional adoption that has begun will help drive the growth of BTC by increasing demand for the asset and reducing its supply. The aforementioned investment giants collectively manage trillions of dollars in assets, while the market capitalization of Bitcoin is just over $0.5 trillion. Only a tiny fraction of this $0.5 trillion is actively traded on the market.

Peter Schiff, the president of Euro Pacific Capital and a staunch critic of Bitcoin, holds the opposite view. He believes that there is “nothing more low-quality than cryptocurrencies.” “Until recently, the rally in highly speculative assets excluded bitcoin. Now that it has finally joined the party, it is likely to end soon,” he stated. According to Schiff, such rallies typically come to an end when “the lowest-quality things” eventually join them, referring to digital assets.

Looking at the BTC/USD chart, there is a suspicion that Peter Schiff might be right. After soaring on the news of BlackRock’s and other institutional players’ interest, the pair has been trading sideways within a narrow range of $28,850 to $31,000 for the past week. According to analysts, besides concerns about SEC actions, bitcoin and the cryptocurrency market are currently being weighed down by miners. Breaking the $30,000 barrier prompted them to send a record volume of coins to exchanges ($128 million in just the past week). Crypto miners fear a price reversal from a significant level due to increased regulatory scrutiny in the industry. Additionally, the average cost of mining remains higher than the current prices of digital assets due to the doubling of computational difficulty over the past year and a half. As a result, miners are forced to sell their coin holdings to sustain production activities, cover ongoing expenses, and repay debts.

As of the time of writing the review, on Friday evening, June 30, BTC/USD is trading around $30,420. The total market capitalization of the crypto market has slightly decreased to $1.191 trillion ($1.196 trillion a week ago). The Crypto Fear & Greed Index is on the border between the Greed and Neutral zones, dropping from 65 to 56 points over the week.

New catalysts are needed for further upward movement. One of them could be the expiration of futures contracts for ethereum and bitcoin on Friday, June 30. According to AmberDate, over 150,000 BTC options with a total value of around $4.57 billion were settled on the Deribit Exchange. Additionally, $2.3 billion worth of contracts were settled for ETH. According to experts from CoinGape, this could trigger significant volatility in July and provide strong support for these assets. However, much will also depend on the macroeconomic data coming out of the United States.

As of the evening of June 30, ETH/USD is trading around $1,920. Several analysts believe that ethereum still has the potential for further bullish momentum. Popular expert Ali Martinez points out that ETH may encounter significant resistance near the $2,000-2,060 range, as over 832,000 addresses previously opened sales in this range. However, if ethereum surpasses this zone, it has a good chance of experiencing a sharp impulse towards $2,330. Furthermore, there is potential for further growth towards $2,750 in the long term.

And finally, a bit of history. Ten years ago, Davinci Jeremie posted a YouTube video strongly recommending his viewers to spend at least one dollar to purchase bitcoin and explained why BTC would grow in the coming years. At that time, Jeremy’s forecast angered or amused most people who did not want to listen to his recommendation. However, they now deeply regret it as they could have acquired over 1,000 BTC for the $1 they would have invested, which is worth $30 million today.

In a recent interview, Jeremy emphasized that it is still worthwhile to buy bitcoin. According to him, only 2 percent of the world’s population owns cryptocurrency, so it still has the potential to delight its investors with new records. “However, there is also one problem,” says Jeremy. “Everyone wants to own a whole bitcoin. No one wants to go to a store and say, ‘Can I get one trillionth of an apple?’ So, although bitcoin is divisible, this property is essentially its Achilles’ heel. The solution to this problem is to make the display of small fractions of BTC more user-friendly and understandable. For example, instead of writing amounts like 0.00001 BTC, they could be replaced by the equivalent amount of satoshis, which is the smallest indivisible unit of one Bitcoin valued at 0.00000001 BTC.”

{kind=link}