U.S. Highlights

- Financial markets rallied this week following a string of promising data pointing to easing U.S. inflationary pressures.

- Inflation as measured by the Consumer Price Index fell to the slowest pace of growth since March 2021 in June. Core inflation also only increased modestly on the month. Input costs also trended lower last month, with the Producing Purchase Index falling to the lowest reading since August 2020.

- Though the data overwhelmingly point to easing inflationary pressures, the Federal Reserve is still expected to deliver another 25 basis-point hike later this month.

Canadian Highlights

- The Bank of Canada hiked the policy rate by another 25 basis points to 5.00%. The decision doubles down on the Bank’s commitment to wrestle inflation back to target.

- Future meetings are live for an interest rate hike, but we believe the Bank of Canada is likely done. Our forecasts point to further moderation in inflation, slowing growth, and a cooler labour market ahead.

- All eyes are on next week’s inflation data for June. We expect headline CPI to continue cooling, but stickiness to persist in core measures.

U.S. – Inflation Data Brings A Healthy Dose of Optimism

Sentiment across global financial markets firmed this week following a lower-than-expected reading on U.S. inflation. Recession fears have been top of mind for investors over the past year amidst the Federal Reserve’s most aggressive tightening cycle in several decades. But signs of cooling inflation provided a dose of optimism that policymakers might achieve a goldilocks scenario of returning price stability without tipping the economy into recession. At the time of writing, the S&P 500 is up 2.5% on the week, WTI has rallied by just over 4% to $76 per-barrel, while yields across the board traded lower by approximately 20bps. The 10-Year Treasury yield currently sits at 3.8%.

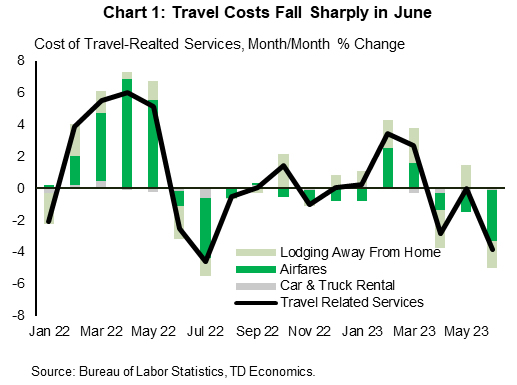

The Consumer Price Index (CPI) eased to a 3.0% pace y/y in June – the lowest reading since March 2021. But, perhaps more notable, core inflation rose by just 0.16% m/m – the slowest pace of growth in 28 months – and dipped to 4.8% y/y. A hefty decline in travel related services underpinned last month’s deceleration, as well as a continued deceleration in shelter costs (Chart 1). Used vehicle prices also fell by a modest 0.5% m/m, which came after outsized gains in each of the two-months prior.

Looking to the months ahead, there’s good reason to remain optimistic that further progress will be made on the inflation front. For starters, the much anticipated slowing in shelter costs now appears to be firmly intact, with both owners’ equivalent rent (OER) and rent of primary residence (RPR) having decelerated in recent months. More importantly, current market-based measures of rent continue to show rental costs slowing, which means further disinflationary pressure on OER and RPR as more leases roll over.

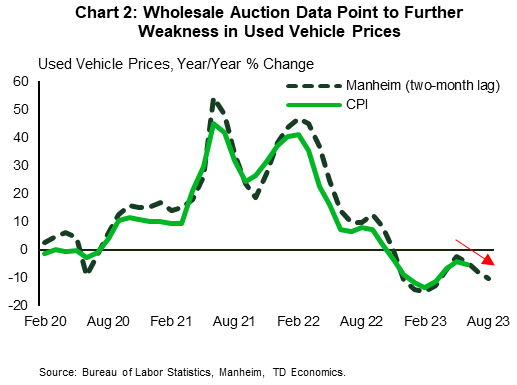

On the goods side, used vehicle prices are expected to be a source of downward pressure on inflation in the coming months. Wholesale auction data for used vehicle prices have tumbled in recent months, with the pass-through to the consumer measure typically taking 2-3 months. (Chart 2). Outside of this category, prices across all other goods have already been flat for three consecutive months and are likely to trend lower through the second half of this year alongside weaker consumer spending. Input costs are also trending favorably. The June reading on the Producer Price Index (PPI) showed that the 12-month change slowed to just 0.1% for final demand products – the lowest reading since August 2020.

Though the recent string of data overwhelming point to a continued easing in inflationary pressures, it is widely expected that Fed will deliver on another 25bps rate hike later this month. No matter which way you slice it, core inflation on a 12, 6, and 3-month annualized basis is still running at a multiple of the Fed’s 2% inflation target. And, with the labor market continuing to exude considerable resilience, policymakers will need to see more convincing evidence that the disinflationary process is firmly intact before calling it quits. Fed Chair Powell has repeatedly emphasized the risk of ‘stopping short’, so the FOMC is likely to maintain a tightening bias over the near-term as they continue to monitor incoming data and fine-tune the end point of its tightening cycle.

Canada – These Boots Were Made For Hiking

Canadian markets were centered on the Bank of Canada (BoC) interest rate decision this week, where the BoC opted to raise the overnight rate by 25 basis points (bps) to 5.00%, the highest level since April 2001. The move aligned with market expectations and matched our own forecast. Canadian yield moves were muted post-announcement. A soft CPI report stateside likely influenced the Canadian rates curve, with yields finishing down on the week. However, the Canadian dollar jumped to 76 cents U.S. and is holding this level into week-end.

As recently as six months ago, markets were pessimistic about the Canadian economy, and expected rate cuts this year. However, that line of thinking has all but evaporated as economic data continues to roll in stronger than expected. Not only have there been 50 bps of hikes since the BoC hopped off the sidelines, but this week’s policy decision certainly had a hawkish tilt as officials have kept the door open to further moves. Macklem & Co. are trying to restore public confidence in their commitment to achieving their two percent inflation target.

Inflation is decelerating, but at a pace slower than the BoC would like to see. According to the MPR, headline annual inflation is now forecast to linger around 3.0% for another year and overall price stickiness has forced the BoC to adjust their path back to 2.0%. Policy makers had previously thought this could be achieved by the end of 2024, but this has now been pushed until mid-2025. Core inflation is also running at a still-uncomfortable pace.

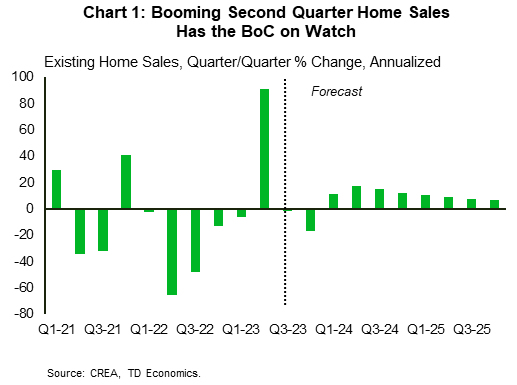

The BoC revised up its outlook for Canada’s GDP growth this year, citing more persistent excess demand, a tight labour market, strong population growth, and a surprise upturn in housing. On housing, recently released data saw Q2 sales surge on a quarter-on-quarter (q/q) basis (Chart 1). That said, we still think that home sales will decline, on average, in the second half of this year, with this week’s interest rate hike likely to have a near-term negative impact.

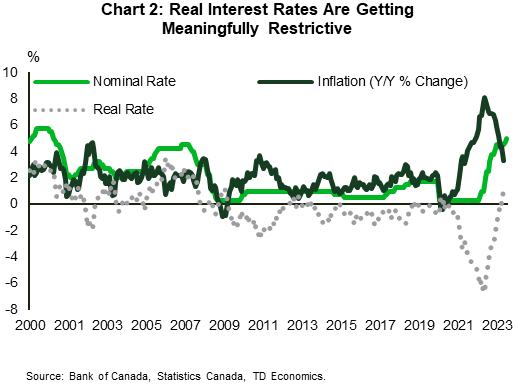

Markets are now pricing in a 50% chance of another rate hike by the end of the year, but we believe the Bank of Canada has reached the peak. Our base case is that key metrics tracked by the BoC will continue to moderate, especially as real rates become increasingly restrictive (Chart 2). Compared to the BoC, our own forecast sees consumption slowing down materially in coming quarters, with this softness more apparent in 2024 as mortgage renewals increasingly strain household budgets.

The BoC will need to digest a deluge of upcoming data before they meet again on September 6th. Front and center is next week’s inflation report for June where we expect further moderation of headline measures. We don’t expect much short-term respite in core measures as progress has effectively stalled over the past several months. Retail trade for May will further inform the state of the consumer.

{kind=link}