Summary

- The FOMC kept the fed funds rate unchanged in June, but the post-meeting statement said that the Committee would take into account “economic and financial developments” when “determining the extent to which additional policy firming may be appropriate.”

- In our view, recent “economic and financial developments” will lead the FOMC to raise its target range for the federal funds rate by 25 bps on July 26.

- For starters, the employment reports for May and June, which were released since the FOMC last raised rates on May 3, showed that while job growth is slowing, the labor market remains tight and is helping to keep inflation above the Committee’s 2% target.

- Inflation slowed in June, including the smallest monthly gain in the core CPI since 2021. However, with price growth running well-above target for about two years now, we believe participants will want to be more confident that inflation is on a sustainable downward path before ending the FOMC’s tightening cycle.

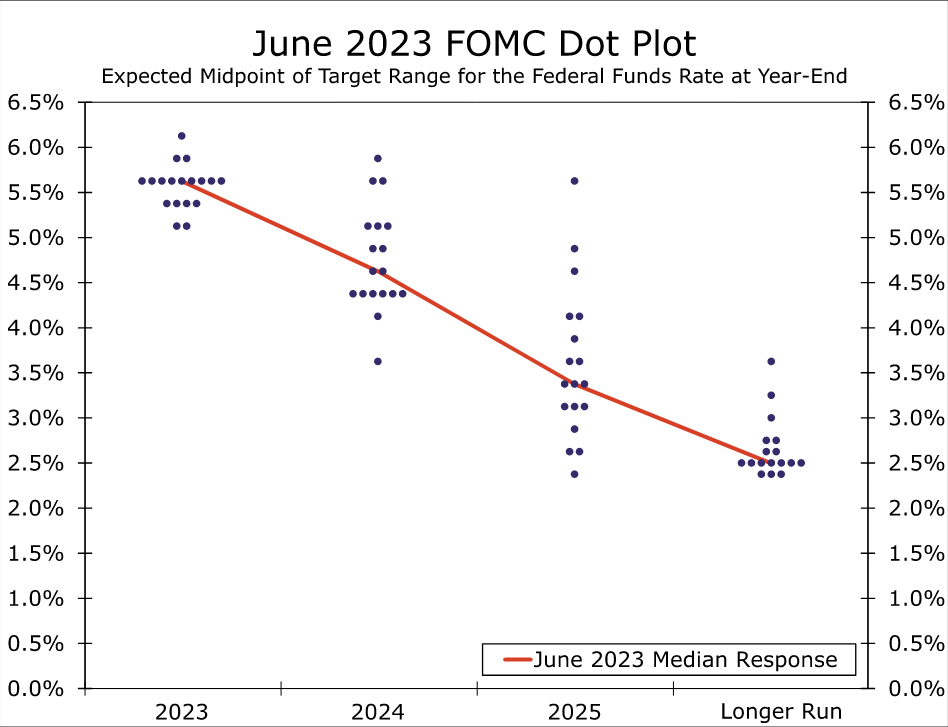

- Furthermore, written and verbal communication by Fed officials since the last FOMC meeting suggest that further tightening likely lies in store. The “dot plot” that was released after the June 14 meeting showed that most members believed that further tightening would be appropriate by the end of this year, and Fed officials have generally sounded hawkish in recent public comments.

- The FOMC could conceivably refrain from hiking its target range by 25 bps on July 26, but we do not believe a consensus currently exists among Committee members for another hold next week. A far more likely way to reach consensus, in our view, would be via a 25 bps rate hike with indications in the post-meeting statement that the FOMC is prepared to hike further, if “economic and financial developments” warrant.

- We do not expect the FOMC to make any technical tweaks to the interest rate it pays on reserve balances that banks hold at the central bank, nor to its repo and reverse repo rates.

Recent Data Support the Case for Another Rate Hike

The Federal Open Market Committee (FOMC) has raised its target range for the federal funds rate by 500 bps since March 2022. The rapid pace of tightening last year, which transpired as inflation was shooting higher, was meant to quickly turn the stance of monetary policy from accommodative to restrictive. The Committee has slowed the pace of tightening this year as economic activity has decelerated and inflation has receded. In the statement that was released following the policy meeting on May 3, at which the FOMC hiked rates by 25 bps, and again on June 14, when it kept rates unchanged, the Committee said it would take into account “economic and financial developments” when “determining the extent to which additional policy firming may be appropriate.”

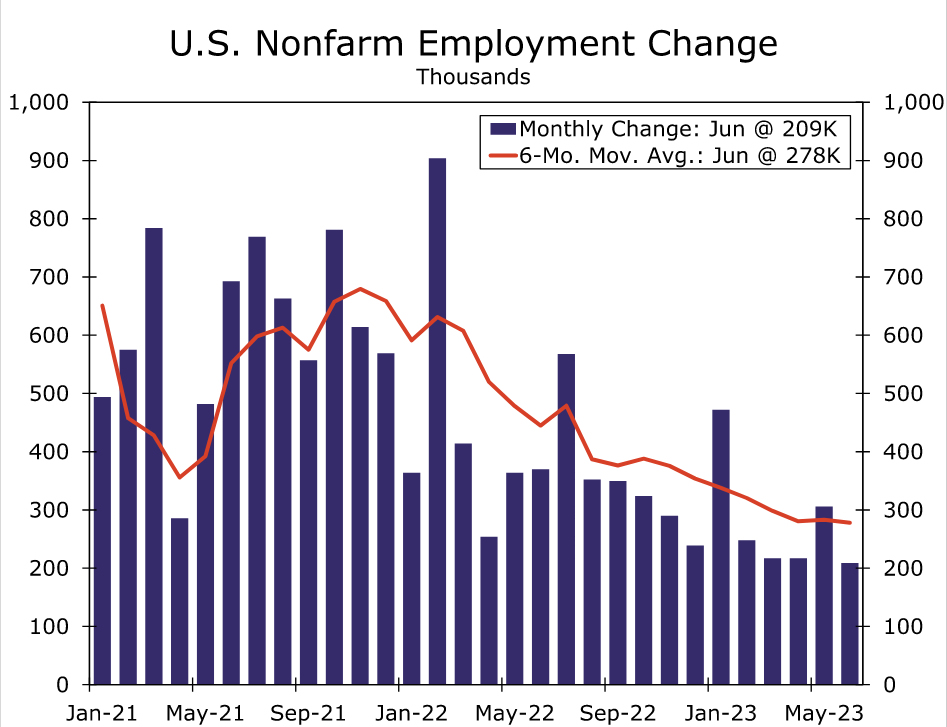

In that regard, recent data suggest that more “policy firming” may indeed “be appropriate.” For starters, the U.S. economy added 209K jobs in June (Figure 1). Although the monthly addition to payrolls in June was the smallest since December 2020, the increase still exceeded the average rise of roughly 185K per month during the 2010-2019 expansion. Only 3.6% of the labor force was unemployed in June, little changed from the cyclical low of 3.4% hit in January and April, and the year-over-year rise in average hourly earnings stayed constant at 4.4% last month. In short, the labor market remains tight, which is helping to keep inflation elevated.

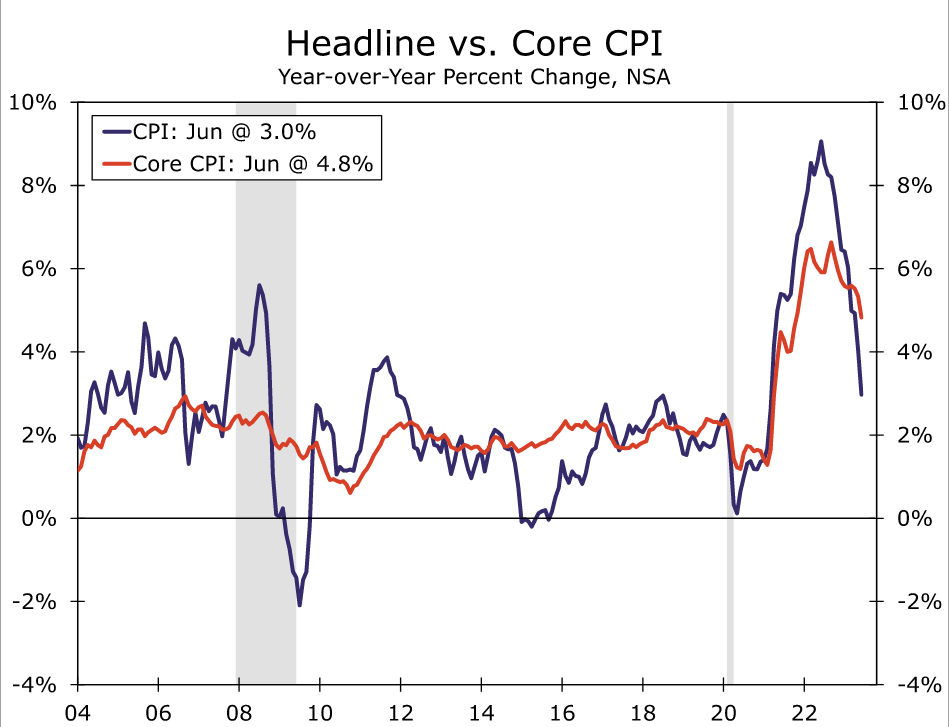

Data released on July 12 showed that consumer prices edged up 0.2% in June relative to the previous month, which caused the year-over-year rate of CPI inflation to drop from 4.0% in May to 3.0% in June (Figure 2). Since peaking at 9.1% in June 2022, the overall rate of CPI inflation has receded by more than six percentage points. While there has been broad-based deceleration in consumer prices over the past year, the 27% drop in the gasoline component of the CPI since June 2022, which has little to do with Fed policy tightening per se, has helped to pull the overall rate of CPI inflation lower over the past year. When looking at the “core” rate of CPI inflation, which excludes prices of food and energy but accounts for 80% of the consumer price index, the FOMC has had less success in bringing inflation lower. The year-over-year rate of core CPI inflation, which rose to a 40-year high of 6.6% last September, has receded to only 4.8%. Moreover, the core CPI in June rose at an annualized rate of 4.1% relative to three months prior (i.e., March). Although down from the comparable three-month rate of change of 5.0% in May, inflation is still running well above the FOMC’s 2% target.

Core inflation was initially pushed higher by rapid acceleration in prices of core goods (i.e., prices of goods excluding food and energy). But a rotation of consumer spending away from goods and toward services in conjunction with the healing of supply chains have led to considerable moderation in core goods inflation since early 2022. In June, prices of core goods were up only 1.4% on a year-ago basis. Although the acceleration in prices of core services, which account for nearly 60% of the overall CPI, lagged the moonshot in core goods prices, service sector inflation has been slower to recede. In June, prices of core services were up 6.2% on a year-ago basis.

Because wages and salaries are the largest cost component for most service-providing businesses, a return to an overall inflation rate of 2% will be difficult for the Federal Reserve to achieve as long as the labor market remains excessively tight. At 3.6% currently, the jobless rate is below what most FOMC members estimate it should be in the “longer run” (i.e., after 2025). This long-run estimate of the unemployment rate can be interpreted as a proxy for the “equilibrium” jobless rate, or the so-called non-accelerating inflation rate of unemployment (NAIRU). In order to generate some “slack” in the labor market, the Fed must slow growth in the economy enough to bring labor demand into better balance with labor supply. Interest rate increases affect the economy with long and variable lags, and individual policymakers can disagree about whether more monetary tightening is currently needed to bring the demand for labor in line with the supply of labor. But written and verbal communication by many Fed officials since the last FOMC meeting suggest that further tightening likely lies in store.

Most FOMC Members Seem to Support Further Tightening

For starters, the “dot” plot that was released at the conclusion of the June 14 FOMC meeting showed that 16 of the 18 Committee members deemed that at least 25 bps of further tightening would be appropriate by the end of this year (Figure 3). More recently, Fed officials have sounded hawkish in public commentary. Last week, a number of FOMC members, including Governors Christopher Waller and Michael Barr, Cleveland Fed President Loretta Mester and San Francisco Fed President Mary Daly all indicated their support for further monetary tightening this year. In sum, we think that a 25 bps rate hike on July 26 is highly likely.

Although the FOMC could conceivably refrain from tightening further on July 26, we think that probability is rather low. As discussed previously, the economy remains resilient and inflation continues to run well above the FOMC’s target of 2%. Financial markets are more or less fully priced for a 25 bps rate hike on July 26, and the FOMC has tried to refrain from surprising markets in recent years. Although Fed speakers did not discuss the specific timing of further rate hikes in recent comments, pausing again at this meeting after the Committee decided to keep rates on hold on June 14 does not seem probable to us. The June dot plot indicated that 12 of the 18 FOMC members thought that at least 50 bps of further tightening would be appropriate by the end of the year. This suggests to us that holding policy rates steady for the second consecutive meeting is not the consensus view on the FOMC. Furthermore, a second consecutive “skip” would likely lead markets to discount the possibility of further tightening, leading to an easing in financial conditions.

Likewise, we think the probability of a 50 bps rate hike next week is even less likely than another pause. Payrolls and core consumer prices have decelerated since the FOMC last met in June. Financial markets are not currently priced for a 50 bps rate hike on July 26 and, as noted above, the FOMC tries to refrain from surprising market participants. Furthermore, the FOMC is a consensus-driven body, and we do not believe a consensus currently exists among Committee members for a 50 bps rate hike next week. A far more likely way to reach consensus, in our view, would be via a 25 bps rate hike with indications in the post-meeting statement, supported by comments by Chair Powell in his press conference, that the FOMC is prepared to hike further, if “economic and financial developments” warrant.

We Do Not Expect Any Change in the Pace of QT

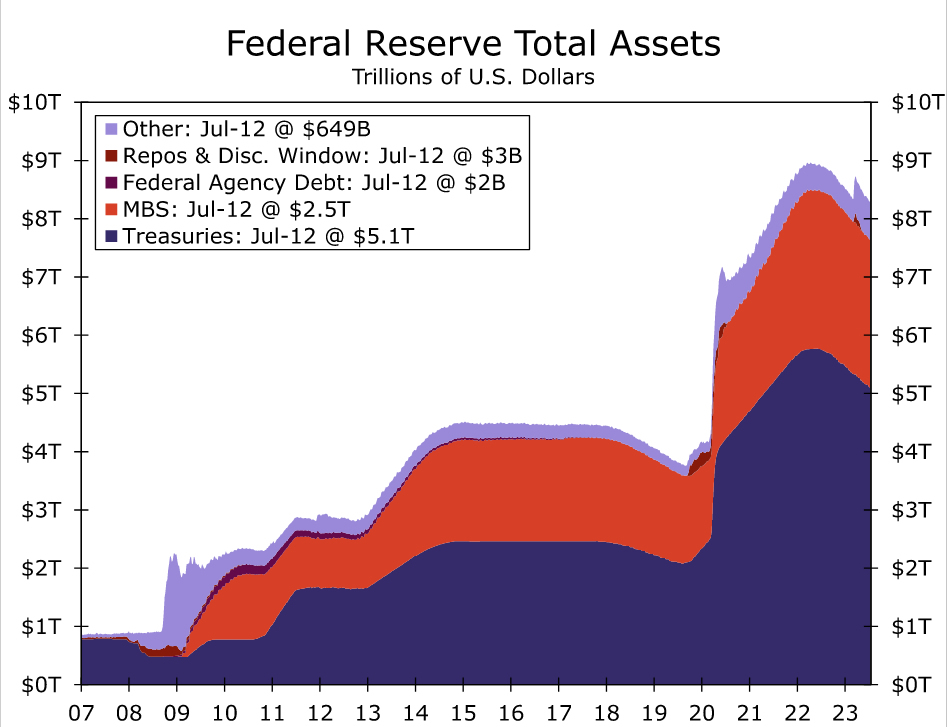

Not only has the FOMC been tightening monetary policy via rate hikes since March 2022, but it has also undertaken “quantitative tightening” (QT) since last June. That is, the FOMC is currently allowing up to $60 billion worth of Treasury securities and up to $35 billion worth of mortgage-backed securities (MBS) to roll off the central bank’s balance sheet every month. As shown in Figure 4, the size of the Fed’s balance sheet peaked at roughly $9 trillion in April 2022 before shrinking to $8.3 trillion in early March of this year. The failures of some regional banks in mid-March caused the balance sheet to spike by approximately $400 billion over the following two weeks as some liquidity-strapped banks tapped the Fed’s emergency lending facilities. But as tensions in financial markets have subsided since March, the outstanding stock of emergency loans has trended lower and the size of the Fed’s balance sheet has declined to $8.3 trillion.

The FOMC held a previously scheduled policy meeting on March 22, less than two weeks after the failures of Silicon Valley Bank and Signature Bank. Despite lingering tensions in financial markets at that time, the FOMC decided on March 22 to maintain the monthly pace of QT at $60 billion of Treasury securities and $35 billion of MBS. With many measures of financial market volatility at low levels and with few signs that banks are experiencing liquidity issues, we look for the FOMC to maintain its current pace of QT at the July 26 meeting. Our expectation regarding the pace of QT was reinforced last week by Minneapolis Fed President Kashkari who said “I think the bar would be quite high in tweaking our path for the balance sheet runoff.” Accordingly, we look for the Fed’s balance sheet to decline further in the month’s ahead and reach roughly $7.7 trillion by year-end.

Additionally, we do not expect the FOMC will make any technical tweaks to the interest rate it pays on reserve balances that banks hold at the central bank, nor to its repo and reverse repo rates. That is, we expect the Committee will lift all three of these rates by 25 bps, in line with the increase in the target range for the federal funds rate.

has raised its target range for the federal funds rate by 500 bps since March 2022. The rapid pace of tightening last year, which transpired as inflation was shooting higher, was meant to quickly turn the stance of monetary policy from accommodative to restrictive. The Committee has slowed the pace of tightening this year as economic activity has decelerated and inflation has receded. In the statement that was released following the policy meeting on May 3, at which the FOMC hiked rates by 25 bps, and again on June 14, when it kept rates unchanged, the Committee said it would take into account "economic and financial developments" when "determining the extent to which additional policy firming may be appropriate."){kind=link}